How much is a mortgage? That depends

The average U.S. homeowner spends about $1,500 per month on their mortgage.

But that’s only one way to answer the question “How much is a mortgage?”

In fact, when you think about mortgage cost, you also need to factor in all the fees for setting up and closing the loan.

Maybe that’s why a third of buyers felt like they spent more than expected on their mortgage in 2019, according to a survey by CoreLogic.

The good news is, it’s easy to keep your mortgage costs down if you know what to look out for when you choose a loan.

Find a low-cost mortgageCalculate your mortgage payment

How to keep mortgage costs low

You can save thousands if you know how to shop around and negotiate mortgage costs.

For instance, CoreLogic’s survey said that almost one-third of home buyers in 2019 put down a higher down payment than anticipated.

This mistake can easily be prevented by researching low- and no-down-payment loans before you buy.

As would-be homeowners are spending more on homes, it’s imperative to not overspend in the areas where you can avoid doing so.

So how do you keep from spending more than you should on your mortgage?

It starts with an understanding of the true costs of a mortgage.

Find a low-cost mortgageUnderstanding your mortgage costs

There are many components that make up mortgage costs. Here’s what you need to know if you want to save.

Down payment: Average 6-12% of purchase price

When you buy a home, your down payment is generally the largest upfront cost.

Many people still think you need 20 percent of the home price in cash when you buy. But that’s not true.

In fact, the average down payment is just 12 percent — and only 6 percent for first-time home buyers.

Here’s what those down payment tiers would look like for a $300,000 home.

| Home price | Down payment (%) | Down payment ($) |

| $300,000 | 6% | $18,000 |

| 12% | $36,000 | |

| 20% | $60,000 |

>> Related: Before making a 20% down payment, read this

You’ll pay your down payment when you close on your loan.

A down payment is only needed when you buy a home. No down payment is necessary when you’re refinancing.

What’s more, there are plenty of loan programs that let you make a lower-than-average down payment. For example:

- Conventional 97 loan — 3% down

- FHA loan — 3.5% down

- VA loan — 0% down

- USDA loan — 0% down

However, some homeowners choose to pay a large lump sum toward your principal when refinancing.

This can help you avoid mortgage insurance and get a better interest rate and lower monthly payment.

Interest: Average rate is below 4% in 2020

Getting the lowest mortgage rate is paramount. The interest rate on a mortgage determines the long-term cost of financing your home.

The lower your mortgage rate, the less you’ll pay for your loan in the long run. It’s that simple.

Take a look at a few examples to see how a half-percent change in mortgage rates can have a big impact on the interest you’ll pay over 30 years.

| Loan amount | Interest rate | Monthly payment | Total interest paid over 30 years | Total cost of mortgage |

| $200,000 | 3.5% | $900 | $123,300 | $323,300 |

| $200,000 | 4% | $955 | $144,000 | $344,000 |

| $250,000 | 3.5% | $1,100 | $154,300 | $404,300 |

| $250,000 | 4% | $1,200 | $179,800 | $429,800 |

| $300,000 | 3.5% | $1,300 | $185,000 | $485,000 |

| $300,000 | 4% | $1,430 | $215,700 | $515,700 |

Using the $250,000 loan amount example: When you drop interest by a half-percent, you save about $70 per month. That might not seem like a lot.

But over the course of a 30-year loan, that 0.5% lower interest rate saves you well over $25,000.

And it’s easy to find a lower interest rate by simply shopping around with a few different mortgage lenders.

Find a low rate todayClosing costs: Average 2-5% of purchase price

Closing costs are fees that are short-term costs associated with the mortgage application process and the mortgage closing.

Home buyers commonly pay fees for applications, inspections, appraisals, and underwriting (that’s the process a mortgage lender uses to determine your eligibility and interest rate).

Home buyers typically pay between 2 to 5 percent of the purchase price in closing costs. Fees can vary by location, as can whom it is that pays for these fees (buyer or seller).

>> Related: Guide to closing costs and how to negotiate them

According to a recent survey by Zillow, buyers pay roughly $3,700 in closing fees nationally. But again, “averages” when it comes to mortgage costs don’t mean a lot. Your own costs will be very different.

The important thing to know is simply that closing costs are usually thousands of dollars — a cost that needs to be accounted for when you’re planning to get a mortgage.

How to compare closing costs: Check your Loan Estimate

When you get a mortgage quote, the lender will give you something called a Loan Estimate or LE. This is a very important tool as it will show you important variables on your loan.

Some of the information you’ll see on a Loan Estimate includes:

- The estimated interest rate

- Monthly payment

- Total closing costs for your loan.

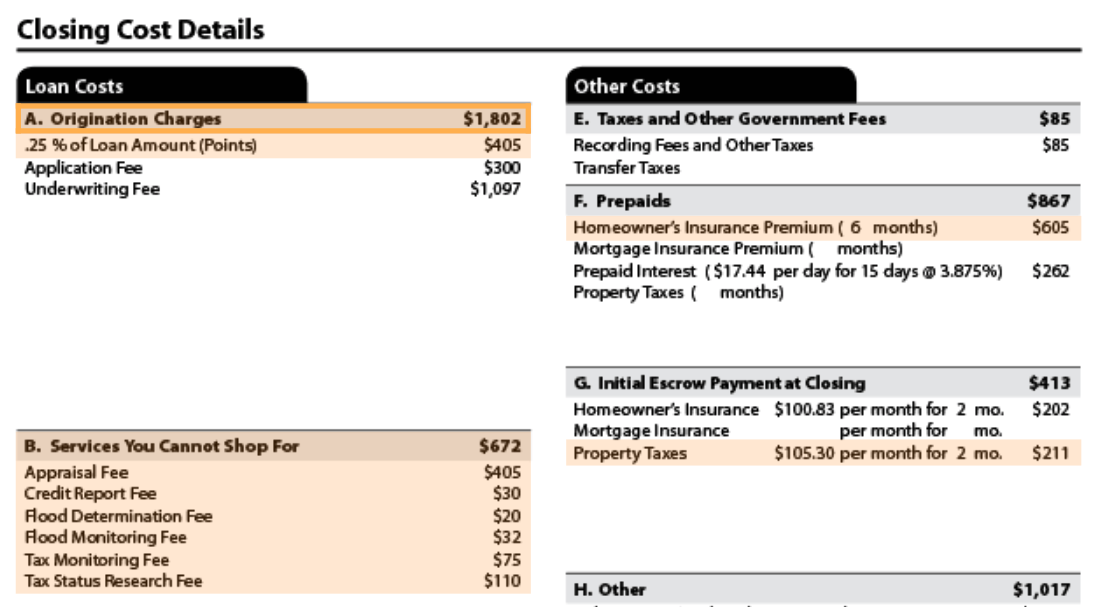

For example, the LE below shows a $1,800 “origination fee” — which is usually the biggest closing cost — along with a variety of smaller fees.

Image: Consumer Financial Protection Bureau

Checking Loan Estimates can help you compare lenders and find the lowest-cost mortgage.

You’ll want to be sure to compare these estimates apples-to-apples — meaning, make sure they have all the same information about your home, and then compare the costs line-by-line to see which is cheaper.

Request custom loan estimates todayLoan-specific fees: Can be 1-2% of loan amount

In addition to closing costs and interest charges, different loan types have their own fees associated with them.

For example, government-backed loans all have an initial fee associated with them:

- FHA Loans — mortgage insurance premium

- VA loans — loan origination fee

- USDA loans — upfront guarantee fee

FHA loans have a closing fee called Upfront Mortgage Insurance Premium (UFMIP), along with a yearly mortgage insurance fee. This mortgage insurance helps ensure the loan if the borrower defaults.

UFMIP costs 1.75% of the loan amount and can be rolled into the loan balance. Yearly mortgage insurance (MIP) is usually 0.85% of the loan amount, broken into monthly payments.

On a $200,000 loan amount, the UFMIP is $3,500. And MIP costs $1,700. While you don’t need to pay both these costs at closing, they still have to be factored into the overall cost of the mortgage.

Similarly, VA loans include a funding fee to help cover the cost of the VA Home Loan program.

The cost varies depending on the size of your down payment and whether it’s your first time using the loan program.

As an example, a second-time-use VA loan with zero down would require a funding fee of 3.60%. On a $200,000 loan amount, that’s $7,200 added to your loan amount.

And a USDA loan includes an upfront guarantee fee to help cover the cost of the USDA Home Loan program. The cost of the fee is 1% of the loan amount and is typically rolled into the loan balance.

Mortgage payment: Average $1,500, but cost varies widely

Your mortgage payment determines how much you pay each month, as well as over the life of the loan.

Commonly known as PITI, your payment is made up of Principle, Interest, Taxes and Insurance.

- Principal — your loan balance

- Interest — what you’re paying to borrow the money

- Taxes — property taxes on the home

- Insurance — homeowners insurance

If any of these components are left out or miscalculated, it could dramatically change your mortgage payment.

>> Related: Calculate your mortgage payment with taxes and insurance

For example, property taxes in 2018 averaged $3,498 per home in the U.S.

Using this amount, forgetting to factor property taxes into your housing budget would mean underestimating your payment by almost $300 per month.

In addition to PITI, some homes have an HOA (homeowner’s association) fee.

Although this amount is typically paid separately from your mortgage payment, it’s still a potential cost that should be calculated when determining housing expenses.

Here’s another example of two different mortgages.

| Purchase price | Interest rate | Down payment | Loan amount | Mortgage insurance | Monthly payment |

| $250,000 | 3.5% | 10% | $225,000 | $125 | $1,130 |

| $400,000 | 3.75% | 20% | $380,000 | $0 | $1,480 |

*Monthly payment includes only principal and interest. Taxes and insurance are not included.

You’ll notice that with two different price points, two different down payments, and two different interest rates, monthly mortgage costs vary widely.

That’s why an “average” mortgage payment doesn’t really mean much. You need to account for your home price, down payment, mortgage insurance, and interest rate to figure out how much your mortgage will really cost.

Get custom mortgage quotesThe bottom line on mortgage costs

Monthly mortgage payments and upfront costs tend to be as unique as those paying them. Rarely are two alike.

The best way to find out how much your mortgage will cost is to get a custom estimate.

Connect with a lender to learn what rate you qualify for, and how your mortgage and closing costs will add up.

Time to make a move? Let us find the right mortgage for you