Loan Estimates let you easily shop for mortgage rates

A Loan Estimate — formerly called a “Good Faith Estimate” — is the most important document you’ll look at when you shop for a mortgage.

The Loan Estimate lists everything you need to know about a mortgage. It includes things like the interest rate, upfront loan costs, and monthly payments, as well as a breakdown of your closing costs.

LEs always come in the same format, making it easy to compare rates and fees from different lenders side-by-side.

This lets you shop for a loan with complete visibility about how much it will cost from any given mortgage company.

Verify your mortgage eligibilityIn this article (Skip to…)

- What is a Loan Estimate or “Good Faith Estimate”?

- What’s included in a Loan Estimate?

- How to read a Loan Estimate: Page 1

- How to read a Loan Estimate: Page 2

- How to read a Loan Estimate: Page 3

- How many days is a Loan Estimate good for?

- Does a Loan Estimate mean you’re approved?

- How accurate is a loan estimate?

- Full list of mortgage Loan Estimate definitions

- How to get a loan estimate

What is a Loan Estimate or “Good Faith Estimate”?

A Loan Estimate (LE) is a standard document you’ll receive when you apply for a mortgage with any lender.

This document used to be called a “Good Faith Estimate,” but was updated in 2015. The new version, called a “Loan Estimate,” is easier to read and a more useful tool for loan shoppers.

LEs always follow the same format — making it simple to compare loan offers side-by-side and find out which company offers the best rates and fees.

Lenders are required to send you a loan estimate within 3 days of you applying for a mortgage.

Get a Loan Estimate. Start here

What is included in a Loan Estimate?

The LE is 3 pages long, split into sections which outline the terms, closing costs, and fees associated with your loan.

Some of the items you’ll find listed on your mortgage Loan Estimate include:

- A summary of your loan details, which include your loan amount, the term of your loan, and your initial monthly payment

- Your escrow account information, which includes your pro-rated annual property tax and homeowners insurance costs

- Your estimated loan closing costs, including your lender fees, your title fees, and whatever third-party costs apply

While it’s important to understand all the terms on your Loan Estimate, there are a few key sections you’ll want to pay special attention to. We walk through those below.

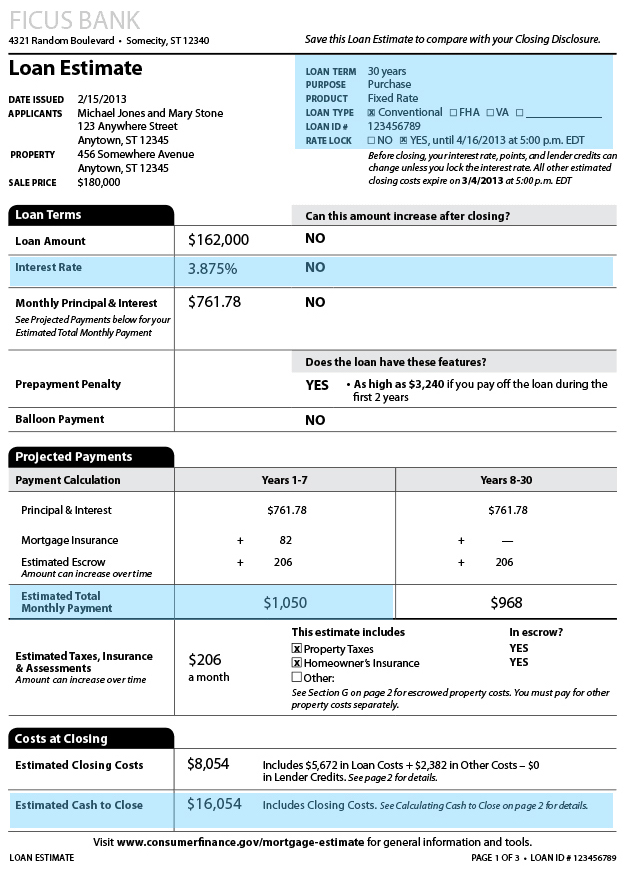

How to read a Loan Estimate: Page 1

Page one of the Loan Estimate is an overview of your loan terms and costs. When you’re comparing lenders, you’ll want to pay special attention to:

- Date issued — The LE is only binding to the lender for 10 days after this date. You should also try to get all LEs on the same day, as rates change daily

- Loan term and type — Make sure these are the terms you wanted, and that all LEs you compare show the same information. Accidentally comparing a 15-year loan to a 30-year loan, for example, would give you a skewed rate comparison

- Interest rate — Look for the lowest rate. But also pay attention to page two, which shows you how much you have to pay (in the form of “points”) to get that rate

- Estimated total monthly payment — This shows you how much you’d pay each month with principal, interest, taxes, and insurance included

- Estimated cash to close — This number shows how much money you actually need upfront, including your down payment as well as lender fees and third-party charges

See where you can find these items below.

Source: The Consumer Financial Protection Bureau

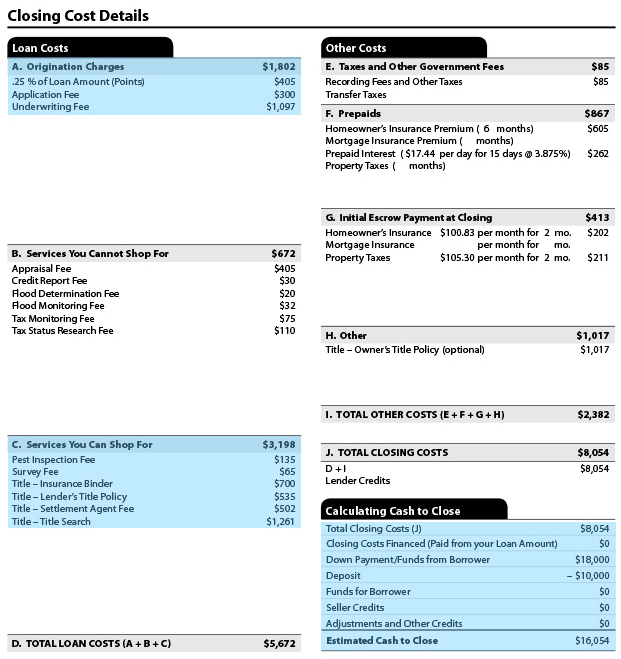

How to read a Loan Estimate: Page 2

The second page of your loan estimate breaks down the costs shown on the first page. To better understand your interest rate and fees, you should look at:

- Points — This shows the dollar amount you have to pay to “buy down” your interest rate, and actually receive the rate shown on page 1

- Application and underwriting fee — Lenders all charge different fees to process your loan. Consider what you’re paying the lender upfront as well as your interest rate

- Services you can shop for — These are third-party services. They’re not set by your lender, but you’re free to shop for cheaper third-party providers

- Calculating cash to close — This box shows you a breakdown of the “cash to close” shown on page 1

See where you can find these items below.

Source: The Consumer Financial Protection Bureau

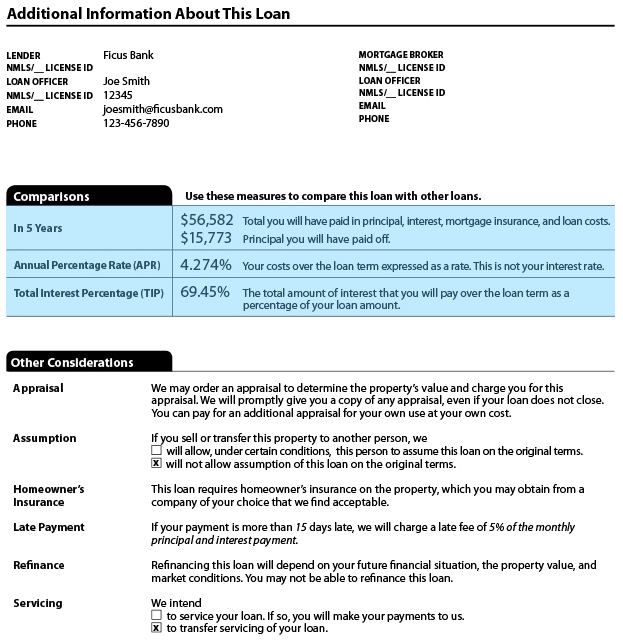

How to read a Loan Estimate: Page 3

Page three of the Loan Estimate has a few more key numbers to help you compare offers from different mortgage lenders.

- In 5 years — Shows how much you will have paid altogether, and how much you will have paid off toward the loan balance alone, in 5 years. This number is especially helpful if you don’t plan to stay in the house a long time, as it helps you understand the weight of upfront costs vs. interest rate in the short-term

- APR — Another way to compare two lenders’ rates and fees combined. The APR represents your total loan costs over the life of the loan, including interest and upfront costs, expressed as an annual percentage

See where you can find these items below.

Source: The Consumer Financial Protection Bureau

How many days is a loan estimate good for?

These terms on a Loan Estimate are valid and binding for a period of 10 days from issuance. That means a lender must follow through with the rate and terms offered on your LE if you move forward with the loan within 10 days — provided that there are no major changes to the loan or application.

Does a good faith estimate mean you’re approved?

Receiving a Loan Estimate or “Good Faith Estimate” does not mean you’re approved for a mortgage. As the CFPB puts it, “Loan Estimate shows you what loan terms the lender expects to offer if you decide to move forward.”

If you do move forward, you’ll have to provide additional documents proving your ability to repay the loan.

Remember, the Loan Estimate is issued based on an initial look at your application. You can get an LE after providing just:

- Your name

- Your income

- The property address of the home you want to purchase/refinance

- The property’s value estimate or purchase price

- Your loan amount

- Your Social Security number

Source: Quicken Loans

At the time a lender sends the Loan Estimate, it hasn’t yet seen all the documentation supporting those numbers on your application. In other words, your loan hasn’t gone through full “underwriting.”

If anything on your application can’t be fully documented (like your income, savings, debt, etc.), your loan terms are subject to change.

The terms on your LE are also subject to change if there’s a major change to your loan. For instance, if you change the term for 30 to 15 years or decide you want an adjustable-rate mortgage instead of a fixed-rate mortgage.

Only after the lender has fully reviewed all your documents will you be officially “approved” for the loan.

Verify your mortgage eligibility

How accurate is a loan estimate?

Although it’s just an estimate, the Loan Estimate is very often a reasonable approximation of what your loan will cost. This is because, by law, final loan costs must be within 10 percent of the costs shown on the original LE.

Importantly, you should try to get all your Loan Estimates on the same day. That’s because mortgage rates change on a daily basis. So if you look at different LEs from different lenders on different days, you’re not really comparing apples to apples quotes.

Full list of mortgage Loan Estimate definitions

Key terms on Loan Estimate page 1:

- Loan amount — The home price, minus your down payment

- Interest rate — Your annual interest rate expressed as a percentage of the loan amount

- Principal and interest — Your monthly payment to the mortgage company. Includes the amount paid toward your loan balance and interest paid to the lender

- Prepayment penalty — May be charged if you sell, pay off a big chunk of the loan balance, or refinance within the stated time frame. Not all lenders have a prepayment penalty

- Balloon payment — Most loans do not have a balloon payment. This is a special type of loan with lower initial payments, and a large lump-sum payment due at the end

- Mortgage insurance — Mortgage insurance is an additional monthly charge, usually required if you put less than 20% down

- Escrow — Typically, you pay taxes and insurance in monthly installments along with your mortgage. This money goes into an “escrow” account

- Taxes and insurance — What you owe for property taxes and homeowners insurance, divided by 12 to show a monthly charge

- Closing costs — Closing costs include all upfront fees charged by your lender and third-party companies to approve, set up, and fund the loan

- Cash to close — Cash to close includes closing costs, plus your down payment; this represents the total amount you have to pay out-of-pocket at the closing table

Key terms on Loan Estimate page 2:

- Application fee — Fee to apply for the mortgage. Many lenders do not charge an application fee

- Underwriting fee — Fee for the mortgage company to review all your documentation and officially approve you for the loan

- Services you cannot shop for — According to the CFPB, “The services and service providers in this section are required and chosen by the lender. Because you can’t shop separately for lower prices from other providers, compare the overall cost of the items in this section to the Loan Estimates from other lenders”

- Services you can shop for — According to the CFPB, “The services in this section are required by the lender, but you can save money by shopping for these services separately. Along with the Loan Estimate, the lender should provide you with a list of approved providers for each of these services”

- Taxes and government fees — The cost to legally transfer the title of the house/property to you

- Prepaids — Prepaid homeowners insurance (typically 12 months) due at closing, plus any prepaid mortgage interest

- Initial escrow payment at closing — Your first few months’ of homeowners insurance premiums and property taxes to be deposited into escrow, due at closing

- Closing costs financed — If any of your closing costs are rolled into the loan balance, that amount will be subtracted from your cash to close

- Deposit — Your earnest money deposit will be subtracted from your final cash to close

- Lender credits — A rebate offered by the lender to reduce your closing costs. Usually, if there are lender credits, you’re paying a higher interest rate. Make sure you discuss this decision with your lender

- Seller credits — If you negotiated with the seller to pay part or all of your closing costs, that amount will be subtracted from your cash to close

Key terms on Loan Estimate page 3:

- In 5 years — The total amount you’d pay toward the loan in five years, including principal, interest, mortgage insurance, and upfront costs

- Annual percentage rate (APR) — Your combined interest and loan costs, represented as a percentage of the loan amount. APR is the effective annual rate you’d be paying if all costs were spread out over the life of the loan

- Total interest percentage (TIP) — Your total interest cost if you were to pay off the loan in full, represented as a percentage of the loan amount

- Late payment — Indicates whether or not there is a fee for being late on your mortgage payment, and if so, what the grace period is

- Servicing — Indicates whether the lender will keep your mortgage or transfer servicing to another company. If it transfers servicing, the new company will handle payments and any modifications to the loan in the future. Transferring servicing is the norm

How to get a Loan Estimate

If you don’t have a home picked out yet, a mortgage lender is likely to give you a “quote” — a non-binding estimate of what your loan might look like.

If you do have a home picked out, you can complete a mortgage application and get an official Loan Estimate within 3 days.

An LE is free (aside from a potential credit check fee), and gives you all the information you need to find the best mortgage deal.

Time to make a move? Let us find the right mortgage for you