Key Takeaways

- Comparing rates and fees from at least three to five lenders can save you thousands over the life of your mortgage.

- The best mortgage offer depends on loan type terms closing costs and service not just the lowest advertised rate.

- Using standardized Loan Estimates makes it easier to compare lenders side by side and negotiate a better deal.

So, you’ve finally decided to take the leap into homeownership, and now the next big step is finding the right mortgage lender to turn your dream into a reality.

With an array of options available in the market, it’s essential to shop around for the best fit. We’ll break down how to shop for a mortgage lender and navigate the process to find the perfect match for you.

In this article (Skip to…)

- How to shop for a mortgage

- Types of mortgages

- Loan term options

- Comparing quotes

- How to negotiate

- Mortgage shopping FAQ

How to shop for a mortgage lender

Choosing the right mortgage lender is crucial, as it can have a lasting impact on your financial well-being. By shopping for a mortgage lender wisely, you not only secure your dream home but also unlock the potential for substantial savings in the long term.

Let’s delve into key steps that can help you navigate the intricate landscape of mortgage lending and find the perfect lender that suits your needs.

Check your home buying eligibility. Start here1. Research, research, research

Embracing the range of mortgage lender options – including banks, credit unions, online lenders, and mortgage brokers – provides a platform for diversity and inclusion in your home buying process. Each type of lender brings distinct advantages and approaches to the table, catering to a wide array of borrower profiles.

By learning how to shop for a mortgage lender and delving into their unique offerings, you gain insights into how they can address your specific financial situation and goals. This diversity not only enhances your mortgage shopping experience but also opens doors to personalized solutions that can save you money and set you on the path to homeownership success.

2. Consider customer reviews and recommendations

One effective way to gather insights while shopping for a mortgage lender is to consult individuals within your social circle who have recently undergone the home-buying process.

Take the time to explore customer reviews and testimonials available online to gain a comprehensive understanding of the customer experience. Prioritize lenders who are known for their exceptional customer service and transparent communication in order to make an informed decision that aligns with your needs and preferences.

3. Understand different mortgage types

Understanding different loan types is essential when shopping for the best mortgage lender. Each loan type, such as conventional, FHA, VA, or USDA loans, has unique features that can impact your financial situation. By being aware of these distinctions, you can confidently select a lender who not only offers competitive rates but also provides the loan type that best suits your needs and helps you achieve your homeownership goals.

Check your home buying options. Start hereBefore selecting a mortgage lender, familiarize yourself with the range of loan options accessible to borrowers, such as:

Conventional loans

Conventional loans are a popular type of loan, accessible with a minimum FICO score of 620 and a down payment as low as 3%. Additionally, lenders evaluate your debt-to-income ratio, credit history, and employment stability, usually preferring a debt-to-income ratio under 43%.

If you’re able to make a down payment of 20% or more, you’ll be exempt from the mandatory private mortgage insurance (PMI) payments. Additionally, once your loan-to-value ratio reaches 78%, lenders usually remove the PMI. Furthermore, refinancing options are available to eliminate PMI from your loan once you’ve built up at least 20% equity in your home.

You can choose from various loan lengths, typically between 10 to 30 years, and opt for either a fixed or adjustable interest rate. Fixed rates provide consistent monthly payments, while adjustable rates might start lower but can fluctuate over time.

Check your conventional loan options. Start hereFHA loans

FHA loans are backed by the Federal Housing Administration (FHA). This type of loan is a favorite among first-time home buyers due to their lenient qualification criteria. You can secure an FHA loan with just 3.5% down if your FICO score is 580 or above, or with a 10% down payment for scores as low as 500.

However, it’s important to note that FHA loans mandate mortgage insurance premiums (MIP) for the entirety of the loan’s term. Nonetheless, there’s an option to eliminate this MIP in the future by refinancing into a conventional loan.

FHA loans also have specific guidelines for the debt-to-income ratio and property standards. The property being purchased must meet certain safety and security standards and undergo an FHA appraisal. This is to ensure the home’s value justifies the loan amount and it meets minimum property standards.

Check your FHA loan options. Start hereVA loans

VA loans, backed by the Department of Veterans Affairs, provide a significant benefit of 0% down payment but are exclusively available to eligible veterans or service members. Although the VA itself doesn’t specify a minimum credit score, individual lenders often impose their own requirements, usually ranging between 580 to 620.

In addition to the no down payment feature, VA loans do not require mortgage insurance, resulting in lower monthly payments. However, there is a VA funding fee, which is typically between 1.3% to 3.6% of the loan amount. It’s important to note that while the VA provides guidelines, individual lenders may have additional criteria for income stability and debt-to-income ratios.

Check your VA loan options. Start hereUSDA loans

The U.S. Department of Agriculture (USDA) loan is specifically designed for low-income buyers in certain suburban and rural areas. This loan stands out because it requires no down payment. While the USDA does not establish a minimum credit score requirement, most lenders prefer to see a FICO score of around 640.

USDA loans aim to support homebuyers who might not qualify for conventional mortgages due to financial constraints. They offer several advantages, such as lower interest rates and reduced mortgage insurance costs compared to conventional loans. However, applicants must meet certain income eligibility criteria, which vary based on the region and household size.

Additionally, the property must be located in an eligible rural or suburban area as defined by the USDA. These loans also typically require the property to be the buyer’s primary residence and to meet specific safety and quality standards.

Check your USDA loan options. Start hereJumbo loans

Jumbo loans are a type of mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). This makes them ideal for financing high-priced or luxury properties that go beyond the scope of conventional mortgages.

Unlike conventional loans, jumbo loans cannot be secured by government-sponsored entities like Fannie Mae or Freddie Mac. As a result, they often have more stringent credit requirements. Typically, lenders look for higher credit scores, usually around 700 or above, for jumbo loan applicants. Additionally, these loans often require larger down payments, commonly 20% or more of the home’s purchase price, to offset the lender’s increased risk.

4. Understand loan repayment terms

Understanding loan repayment terms is crucial when shopping for a mortgage lender. It allows you to assess your financial obligations accurately over the loan term, ensuring you choose a lender whose terms align with your budget and long-term financial goals.

Check your home buying options. Start hereHere are the two most common rate repayment structures when shopping mortgage lenders:

Fixed-rate mortgages (FMR)

Fixed-rate loans have a set interest rate that doesn’t change during the loan’s term. Common loan terms are 15-year and 30-year mortgages, which means you’ll make monthly mortgage payments for 180 months and 360 months, respectively.

Adjustable-rate mortgages (AMR)

Adjustable-rate loans have variable interest rates that change over the life of the loan. Your initial rate is often fixed for a period of time, but will reset periodically over your 15- or 30-year loan term

5. Get quotes from multiple lenders

Most experts recommend getting at least three rate quotes when you shop for a mortgage. But there’s no limit to the number of mortgage companies you can apply with. And research suggests that the more quotes you get, the more money you’ll save.

For example, Freddie Mac found that “borrowers who received as many as five rate quotes during the second half of 2022 could have potentially saved more than $6,000 over the life of the loan, assuming the loan remains active for at least five years.”

You should get at least three to five mortgage quotes when shopping for a mortgage. The more quotes you get, the more you’re likely to save.

Each of these quotes can provide different benefits, from lower rates to more flexible terms, especially if you’re considering a refinance. It’s important to compare their offers carefully to find the one that best fits your financial situation.

“Keep in mind that a quote is just that, and nothing is guaranteed until you are locked in,” reminds Jon Meyer, mortgage loan expert. “But quotes should help you gauge the market, lender to lender.”

6. Compare quotes and negotiate rates

At face value, comparing mortgage rates is fairly straightforward. But at this point you may be wondering ‘How many quotes should I get?’

Compare rates from multiple lenders. Start hereYou can apply for preapproval with three or more lenders and simply compare the rates you’re offered. But remember — your interest rate isn’t the only thing that matters when shopping for a mortgage. You also need to look at factors like closing costs, origination fees, annual percentage rate (APR), and discount points.

Luckily, it’s easy to compare mortgage quotes and find the best mortgage lender.

All mortgage offers come in the same format, called a Loan Estimate, so you can quickly skim for rates, fees, and other important information to find the best offer.

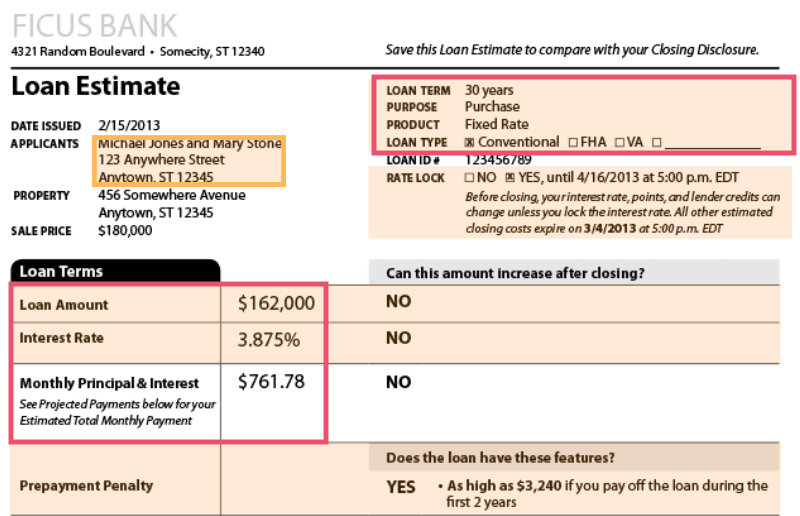

How to read your Loan Estimates

You will find your loan terms, quoted interest rate, and monthly payment on the first page of your Loan Estimate.

Along with comparing interest rates, you can use this page to:

- Make sure all your loan offers are for the same loan type (conventional loan, FHA loan, USDA loan, etc.)

- Make sure they’re all quoting the same type of rate (fixed-rate mortgage or adjustable-rate mortgage)

- Compare monthly mortgage payments to see which loan is cheaper month to month

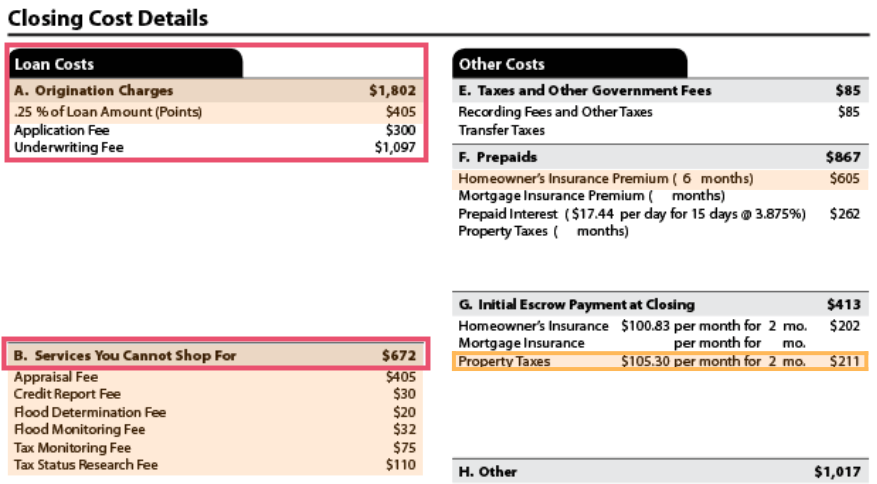

On the second page, you will see your closing costs and other upfront expenses, like prepaid taxes and homeowners insurance.

Note that loan costs are separated into two categories: (A) Origination Charges, and (B) Services You Cannot Shop For.

Origination charges represent the lender’s own fees. You’ll want to pay close attention to this section when shopping for a mortgage because these fees can vary a lot from one lender to the next. Shopping for a lower fee could save you serious cash at the closing table.

In addition, this section includes information on “Points.” Points — or discount points — are an additional fee paid upfront to get a lower interest rate.

You’ll want to pay attention to discount points when shopping for mortgage rates. If one mortgage lender has exceptionally low rates, but charges points, you know you have to pay extra upfront to actually get that rate.

Images: CFPB

Because these documents are uniform, it’s easy to compare Loan Estimates from different lenders side by side and find the very best deal on your rate and closing costs.

Use your mortgage quotes to negotiate

Keep in mind that the mortgage quotes you get are not set in stone. Mortgage lenders have the flexibility to adjust their fees and even their interest rates. That means you can often use competing offers as leverage to negotiate your costs.

Compare rates from multiple lenders. Start hereDon’t hesitate to play one lender off against another:

“I like your company, but I’ve got a quote here with a lower rate or less expensive closing costs. Can you match it? Better yet, can you beat it?”

Chances are, these negotiations won’t lower your rate by much. But, when you’re borrowing huge amounts over decades, even a tiny drop in your rate can add up to hundreds or even thousands. And what do you have to lose?

What happens after you find the best mortgage lender?

Once you’ve put in your applications, compared interest rates and fees, and chosen your preferred lender, there are a few final steps to take in order to finalize your mortgage loan.

Submit a final loan application

Once you’ve found your dream home and successfully negotiated the purchase price with the seller, it’s time to begin the formal mortgage application process.

Although you may have already been preapproved for a mortgage, you’ll need to go through a similar, but more rigorous, underwriting process in order to receive final approval.

The underwriter will verify all your financial information and documentation. It may request additional verifications or a letter of explanation, so stay on top of the process and respond to any queries as soon as possible. This will help keep your loan process and closing date on track.

Don’t make any big life changes

Try to avoid changing jobs or becoming unemployed, if at all possible. And don’t open or close any credit accounts. Any of the last three could reduce your credit score. “Also, don’t make any large purchases on open credit lines,” adds Meyer.

Keep in mind that lenders routinely recheck your credit history just before closing. So you don’t want to do anything that will jeopardize your savings, mortgage rate, or — worst case — your entire mortgage approval.

FAQ: How to shop for a mortgage

Compare rates from multiple lenders. Start hereFinal thoughts on how to shop for a mortgage lender

Curious about securing the best mortgage lender in today’s market?

The key is in knowing how to shop for a mortgage lender effectively. Start by gathering multiple quotes and then diligently compare them.

Ensure that each loan offer has similar terms and identical rate lock periods. This comparison process is straightforward and can conveniently be done online.

Want to explore your current home buying options further? Click through to find out more about how to shop for a mortgage and unlock the best deals available now.

Time to make a move? Let us find the right mortgage for you