Key Takeaways

- You can buy a home with a USDA loan and put no money down if the property is located in an eligible rural or suburban area.

- USDA mortgage rates are usually lower than FHA and conventional rates, which makes mortgage payments more affordable.

- You can choose between USDA Guaranteed, Direct, and Home Improvement loans based on your income and housing needs.

USDA loans help people buy a home in rural and suburban areas with no down payment. Backed by the government, they’re often easier to qualify for than other options and offer competitive USDA mortgage rates that can keep monthly payments affordable.

USDA loans mainly serve low- to moderate-income buyers who may not qualify for conventional financing. If homeownership feels out of reach, a USDA loan might change your mind.

In this article (Skip to…)

- Overview

- Types of USDA loans

- Requirements

- USDA eligibility map

- USDA loan rates

- USDA mortgage insurance cost

- How to get a USDA loan

- USDA loan vs other loans

- FAQ

>Related: How to buy a house with $0 down: First-time home buyer

What is a USDA loan?

A USDA loan is a mortgage loan backed by the U.S. Department of Agriculture under its Rural Development program. It’s meant for low- to moderate-income home buyers and lets you buy with no down payment, lower mortgage insurance, and USDA loan interest rates that are below market due to government subsidies. To qualify, your household income must fall under the USDA limits. The home must also be your primary residence in an eligible rural area.

Verify your USDA loan eligibility. Start hereHow do USDA loans work?

You apply for a USDA loan through a bank, credit union, or mortgage lender authorized to offer USDA-guaranteed loans. Once you choose a lender, you’ll submit financial documents, complete underwriting, and close the loan after approval. Borrowers with very low income may qualify for a Single Family Housing Direct Home Loan, which is only available through USDA Rural Development. You can use a USDA home loan to purchase or refinance a home.

Types of USDA loans

The USDA home loan program offers three main options, depending on your income and what type of loan you’re looking for.

Verify your USDA loan eligibility. Start hereUSDA Guaranteed Loans

These are the most common. You apply through a mortgage lender, and the USDA guarantees the loan, which is why USDA mortgage rates can be so competitive. A USDA Guaranteed Loan provides 100% financing and lenient credit score requirements. To qualify, your household income must fall within the local income limits, and the home must be in an eligible rural area.

USDA Direct Loans

Funded directly by the USDA, the 502 Direct Loan Program is for very low-income borrowers who want to buy, build, or fix up a home in a rural area. Direct Loans offer USDA rates as low as 1% with payment assistance, along with longer loan terms of up to 38 years. The home price must fall under the local loan limit, which varies by region: from around $330,000 in most areas to over $700,000 in high-cost states like New York and California.

USDA Home Improvement Loan

Also known as the Single Family Housing Repair Loan and Grant Program, this option helps low-income rural homeowners pay for repairs or upgrades that improve safety or livability. You can get a loan of up to $40,000 at a 1% USDA rate, repayable over 20 years. Grants of up to $10,000 are available for homeowners aged 62 or older who are unable to afford their loan payments; however, the funds must be repaid if the home is sold within three years. You can also combine a loan and grant for up to $50,000 in total assistance.

Qualifying for USDA loans

To qualify for a USDA home loan, you’ll need to meet several eligibility requirements that vary depending on whether you are applying for a USDA Loan Guarantee or a USDA Direct Loan. Some general USDA qualifications, however, apply to all USDA loans, specifically those based on both the buyer’s and property’s eligibility.

Verify your USDA loan eligibility. Start hereUSDA loan property requirements

- Eligible rural area: The USDA defines an eligible area as having a population of 20,000 or fewer. Check the USDA’s eligibility site or the map below.

- Single-family primary residence: USDA loans are only available for primary residences, not investment properties or second homes.

- Meet safety standards: The property must adhere to the USDA’s minimum property requirements for safety, structural integrity, and access to utilities and services.

USDA loan borrower requirements

- Income limits: Household income can’t exceed 115% of the area median income to meet USDA income eligibility requirements.

- Stable income: Applicants must demonstrate stable and dependable income, typically for at least 24 months before applying.

- Creditworthiness: Lenders usually seek a minimum credit score of 640 for guaranteed loans, with USDA Direct Loans potentially having more lenient criteria.

- Debt-to-income ratio: Monthly debt, including future mortgage payments, generally should not exceed 41% of gross monthly income, with exceptions based on credit score and cash reserves.

- Citizenship status: Applicants need to be U.S. citizens, U.S. non-citizen nationals, or qualified aliens with a valid Social Security number.

What qualifies as an eligible rural area?

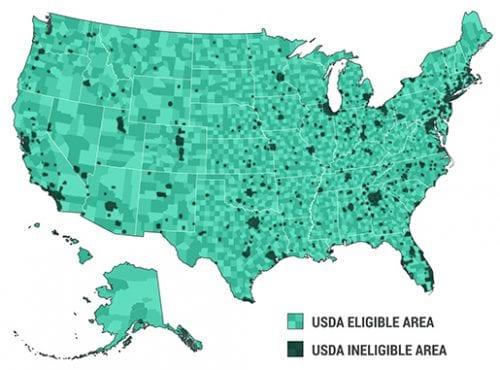

The USDA eligibility map is the best way to check if a home is in an eligible rural area for a USDA home loan. You can enter a specific address or browse the map to see which locations qualify for USDA Guaranteed Loans or Direct Loans. Areas shown in green are eligible; areas marked in black are not. Small black pockets—or larger black zones around a metro area—usually mark places with more than 20,000 people, which fall outside USDA guidelines.

Verify your USDA loan eligibility. Start here

1 Source: USDAloans.com, based on Housing Assistance Council data

USDA loan rates

USDA mortgage rates are among the lowest on the market; typically about 0.5% to 0.75% lower than what you’ll see with FHA loans or conventional loans. To estimate current USDA loan rates, just subtract that range from today’s average mortgage rates.

Find your lowest USDA interest rates. Start hereKeep in mind that these are averages. Your actual USDA loan rate will depend on your credit score, debt-to-income ratio, and the lender you work with.

| Program | Mortgage Rate | APR* | Change |

|---|---|---|---|

| Conventional 30-year fixed | |||

| Conventional 30-year fixed | 6.785% | 6.849% | +0.03 |

| 30-year fixed FHA | |||

| 30-year fixed FHA | 6.374% | 6.436% | -0.22 |

| 30-year fixed VA | |||

| 30-year fixed VA | 6.45% | 6.492% | -0.38 |

| Rates are provided by our partner network, and may not reflect the market. Your rate might be different. Click here for a personalized rate quote. See our rate assumptions See our rate assumptions here. | |||

Additionally, in May 2024, the USDA provided base rates for both Single Family Housing Direct Home Loans and Guaranteed Loans, which serve as a starting point for borrowers.

- Single Family Housing Direct Home Loans: The USDA underwrites these loans directly for low- and very low-income buyers. The interest rate is a fixed 4.625% for qualified borrowers.

- Single Family Housing Guaranteed Loan Program: USDA-approved lenders underwrite these loans. The interest rate depends on the loan type and length. For loans under 5 years or with variable rates, the cap is SOFR + 6.75%. For fixed loans of 5 years or more, the cap is the 5-year Treasury rate + 5.5%.

Your final USDA loan interest rate might be higher or lower than these base rates, depending on your finances and the lender’s policies. That’s why it’s smart to shop around and compare offers from multiple USDA-approved mortgage lenders.

Additionally, while USDA mortgage rates are generally lower than those of other mortgage programs, it’s important to consider all aspects of the loan, including fees and closing costs, when comparing options.

How to get the best USDA mortgage rates

If you’re shopping for the lowest mortgage rates for USDA loans, a stronger financial profile can make a big difference. Here are a few ways to improve your odds.

- Increasing your credit score by disputing inaccurate negative marks and checking that old debts are no longer being reported.

- Making a down payment can strengthen your application, even though it’s not required.

- Paying off existing debts can lower your debt-to-income ratio and help you get a better rate.

- Comparing rates, fees, and loan terms from several USDA-approved lenders to find the best deal.

Understanding USDA loan guarantee fees and other costs

USDA loans don’t come with traditional mortgage insurance, but they do include two guarantee fees that fund the program and protect lenders. There’s a one-time upfront fee, plus a small annual fee that’s spread out over 12 months.

- Upfront guarantee fee: This one-time fee is usually 1% of the loan amount. You can pay it upfront or roll it into your loan balance.

- Annual guarantee fee: This works like mortgage insurance, but it’s specific to USDA loans. It’s 0.35% of the remaining principal, split into monthly payments and included in your monthly mortgage payment.

USDA appraisal requirement

The USDA requires a specialized appraisal to verify the home’s value and ensure it meets Minimum Property Requirements (MPRs) for safety, livability, and structural integrity. Appraisal costs usually range from $500 to $800, depending on the location and lender. You should also budget for closing costs of about 2% to 5% of the purchase price, which cover loan fees, title charges, and the appraisal fee.

How to apply for a USDA loan

Qualifying for a USDA home loan can be an excellent way to finance a home, especially if you’re looking to buy in a rural area. These rural development loans provide appealing benefits like zero down payments and competitive interest rates. However, the USDA loan approval process involves several steps and specific eligibility requirements. Here’s a guide on how to apply for a USDA home loan.

Check your USDA loan eligibility. Start hereStep 1: Check your USDA eligibility

Before diving into the application process, it’s important to determine if you meet the USDA’s eligibility requirements. These typically include:

- A minimum credit score of 640, though this may vary by lender

- A debt-to-income (DTI) ratio of up to 41%, with some flexibility depending on the borrower’s situation

- Income limitations, which vary by location and household size

- The property must be located in a USDA-eligible area and meet certain safety conditions and size requirements

Step 2: Gather necessary documentation

You’ll need to provide various documents to prove your USDA eligibility, including:

- Proof of income eligibility (e.g., pay stubs, tax returns)

- Employment verification

- Credit history report

- Personal identification (e.g., driver’s license, passport)

Step 3: Get pre-qualified

Contact a USDA-approved lender to get pre-qualified or pre-approved for a mortgage. During this prequalification, the participating lender will review your financial situation to provide an estimate of how much you can borrow with a USDA loan. Pre-approval involves a more detailed review of your finances and is a stronger sign of potential loan approval. Both pre-approval and prequalification can help you understand your budget better and show sellers that you are a serious buyer.

Check if you're eligible for a USDA loan. Start hereStep 4: Find a qualifying property

Once pre-qualified or pre-approved, you can begin searching for a property that complies with USDA guidelines. Remember that the home must be your primary residence and located in an eligible rural area. Working with a real estate agent experienced in USDA loans can provide a significant advantage.

Step 5: Complete USDA home loan application

After finding the right property, you’ll need to fill out the USDA loan application. Your lender will guide you through this process, which will include a more thorough review of your financial situation and the submission of additional documents.

Step 6: Obtain property appraisal and inspection

The lender will arrange for an appraisal to ensure the property meets USDA standards. An inspection may also be required to identify any potential issues with the home.

Step 7: Get final loan approval and close

Once the appraisal and inspection are finished and all documentation is verified, you’ll move on to the loan approval stage. If approved, you’ll go to closing, where you’ll sign all required paperwork and officially secure your USDA home loan. With the loan in place and the keys in your hand, you’re now ready to move into your new home!

How do USDA loans compare to other types of loans?

USDA loans aren’t the only type of mortgage out there. If you’re not eligible for a USDA loan, you might be for an FHA or VA loan, or even a conventional loan. Here’s an overview of some key differences between these types of loans:

Verify your USDA loan eligibility. Start here| Loan Type | Credit Requirements | Debt-to-Income Ratio | Down Payment | Mortgage Insurance |

| USDA Loan | None, but 640 is standard | Up to 41% | None | Upfront fee of 1% and annual fee of 0.35% |

| Conventional Loan | 620 | Up to 43% | 3% or 5% | Required if down payment is less than 20% |

| FHA Loan | 580 | Up to 50% | 3.5% | Upfront fee of 1.75% and annual fee of 0.45% to 1.05% |

| VA Loan | None unless lender requires | Up to 41% | None | Upfront funding fee of 1.25% to 3.3%, no annual fee |

USDA loans vs. conventional loans

USDA loans have no down payment requirement, while conventional loans typically require a minimum of 3% down. USDA loans also have more flexible credit score requirements, with most lenders accepting scores as low as 640. Conventional loans usually require a minimum credit score of 620. Additionally, USDA loans do not require private mortgage insurance (PMI), which is often required for conventional loans with a down payment of less than 20%.

USDA loans vs. FHA loans

Both USDA and FHA loans allow for low down payments (0% for USDA, 3.5% for FHA). However, USDA loans are limited to eligible rural areas, while FHA loans can be used for properties in any location. FHA loans also have slightly more lenient credit score requirements, with a minimum of 580.

USDA loans vs. VA loans

USDA and VA loans share many similarities, including no down payment requirement and competitive interest rates. However, VA loans are exclusively for eligible military service members, veterans, and their surviving spouses. USDA loans are available to a broader range of borrowers but are restricted to eligible rural areas.

FAQs about USDA loans

Verify your USDA loan eligibility. Start hereCompare USDA loan rates today

USDA interest rates are among the most competitive in the real estate market, making now an excellent time for first-time home buyers to take action.

With the potential for low or no down payments and favorable terms, USDA loans can help you save on your dream home.

Compare USDA loan rates from multiple lenders at once, without any commitment, by clicking the links below. Take the first step towards homeownership and discover the benefits of USDA loans today.

Time to make a move? Let us find the right mortgage for you1 Source: USDAloans.gov, based on Housing Assistance Council data