Key Takeaways

- FHA loans make homeownership more accessible by allowing low credit scores, small down payments, and flexible income and debt requirements.

- FHA programs go beyond home buying, offering refinance, renovation, and specialty loan options for a wide range of borrower needs.

- The main downside is required mortgage insurance, but many borrowers accept the added cost in exchange for easier qualification and lower upfront barriers.

FHA loans have been making homeownership more accessible for decades. Tailored to borrowers with lower credit, the FHA makes it possible to buy a house with a credit score of just 580 and only 3.5% down.

But home buyers aren’t the only ones who can benefit. For current homeowners, an FHA refinance may let you access low rates and home equity, even without great credit.

Not sure whether you’ll qualify for a mortgage? Check out the FHA mortgage program. You might be surprised.

In this article (Skip to...)

- What is an FHA loan?

- How does an FHA loan work?

- FHA loan benefits

- Types of FHA loans

- FHA loan qualifications

- FHA vs conventional

- FAQ

>Related: How to buy a house with $0 down: First-time home buyer

What is an FHA loan?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA). Thanks to their flexibility and low rates, FHA loans are especially popular with first-time home buyers, borrowers with low or moderate incomes, and lower-credit home buyers.

But FHA financing isn’t limited to a certain type of buyer—anyone can apply.

That’s because FHA insurance protects mortgage lenders, allowing them to offer loans with low interest rates, easier credit requirements, and low down payments (starting at just 3.5%).

Verify your FHA loan eligibility. Start here

How does an FHA loan work?

The first thing to know about FHA mortgages is that the Federal Housing Administration doesn’t actually lend you the money. You get an FHA mortgage loan from an FHA-approved bank or lender, just like you would any other type of home mortgage loan.

Verify your FHA loan eligibility. Start hereThe FHA’s role is to insure these mortgages, offering lenders protection in case borrowers can’t pay their loans back. In turn, this lets mortgage lenders offer FHA loans with lower interest rates and looser standards for qualifying.

The one catch is that you pay for the FHA insurance that protects your mortgage lender. This is called the “mortgage insurance premium,” or MIP for the life of the loan or until the FHA home loan is refinanced into another type of mortgage. We go over this in detail below.

Why are FHA loans beneficial?

Many, particularly first-time home buyers, choose this loan type due to the flexible FHA loan qualifications and borrower-friendly features. You can opt for a fixed-rate loan with consistent payments or an adjustable-rate mortgage that adjusts to changing rates.

With an efficient underwriting process and guidance from a trusted loan officer, the FHA mortgage program makes owning a home more attainable, regardless of where you’re starting.

Check your FHA loan eligibility. Start hereHere are some key FHA loan benefits:

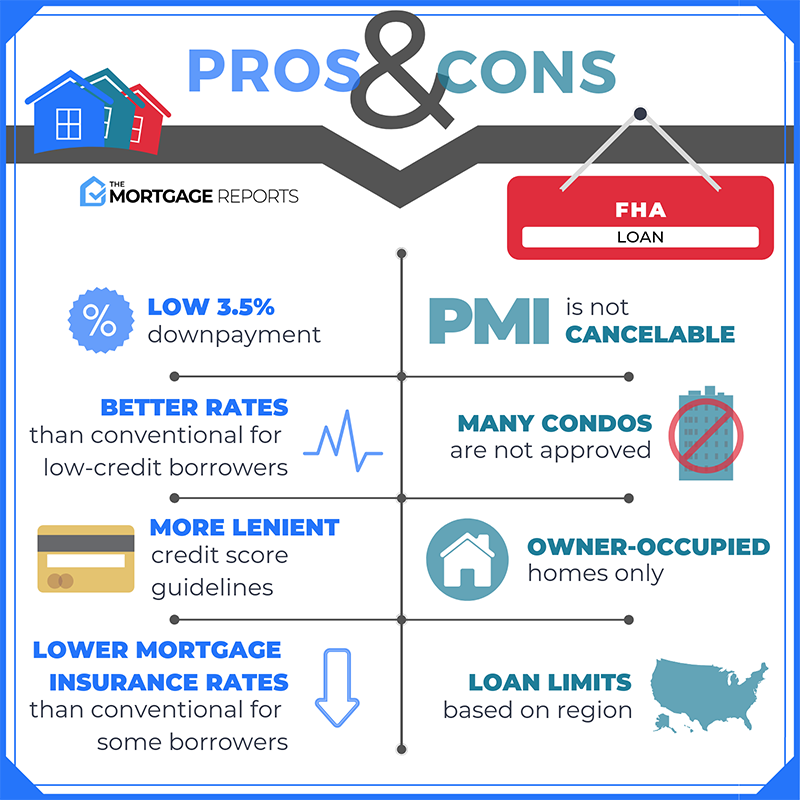

- Down payments as low as 3.5% of the home purchase price.

- 100% of the down payment and closing costs can come from gift funds.

- Higher debt-to-income (DTI) limits between 43% and 50% with compensating factors.

- Credit scores as low as 580 qualify for a 3.5% down payment and 500-579 with 10% down.

- Borrowers with no credit scores can still qualify, as the Department of Housing and Urban Development (HUD) prohibits FHA lenders from denying applications based solely on a lack of credit history.

- Non-traditional credit histories, such as rent or utility payments, are accepted.

- FHA loan limits for single-family homes range from $541,287 to $1,249,125 in higher-cost areas of the country.

- Streamline refinancing makes it simple to lower your rate with minimal documentation.

Borrowers with smaller savings or financial hurdles can achieve homeownership thanks to these FHA benefits.

Types of FHA loans

Whether you’re buying your first home, fixing up a property, or looking to refinance, FHA loans aim to make homeownership accessible. These programs open doors to your next home by offering flexible FHA loan qualifications that accommodate lower credit scores and smaller savings for a down payment.

Compare FHA loan quotes from multiple lenders. Start herePlus, many buyers may qualify for down payment assistance programs, which can provide even more support along the way.

Home purchase loans

The most common type of FHA loan, the Basic Home Mortgage 203(b), allows you to purchase a single-family home as your primary residence. With a down payment requirement as low as 3.5% and a minimum credit score of 580, it’s a popular choice for first-time home buyers.

Keep in mind that vacation homes, real estate investment properties, and second homes do not qualify for this loan.

Refinance loans

For current homeowners, FHA offers multiple loan types to refinance your mortgage for better terms or access home equity:

- FHA rate-and-term refinance: If you want to lower your interest rate or switch your loan term, this FHA refinance program could be the right fit—especially if your credit score has improved since you first got your loan.

- FHA Streamline Refinance: Already have an FHA loan? The Streamline Refinance makes refinancing quick and easy. With minimal documentation and no need for a new appraisal, it’s a hassle-free way to reduce your monthly payments or lower your mortgage insurance premiums.

- FHA cash-out refinance: Need cash? The cash-out refinance lets you tap into your home equity and turn it into funds for big expenses. It often requires a minimum credit score of 620 and leaves at least 15% equity in your home after the refinance.

- FHA 203(k) Refinance: If your home needs significant repairs or renovations, this program lets you refinance your mortgage and include the cost of improvements in one loan. It’s a smart way to both update your property and simplify your mortgage.

Renovation loans

For buyers or owners looking to improve their property, FHA renovation loans combine the costs of the home and upgrades into a single loan:

- FHA 203(k) loan: If you’re purchasing a home that needs a little (or a lot of) work, this program lets you roll the purchase price and renovation costs into one loan. From major repairs to simple updates, the 203(k) is a practical solution for turning a fixer-upper into your dream home.

- FHA Energy Efficient Mortgage (EEM): Looking to make eco-friendly improvements? This loan allows you to finance energy-efficient upgrades, like solar panels or insulation, as part of your FHA loan. This approach not only reduces your utility costs but also increases the value of your home.

- FHA Title 1 Loan: Perfect for smaller-scale improvements or repairs, this FHA loan helps homeowners finance property upgrades without refinancing their mortgage. It’s a flexible option for making your home more functional or energy-efficient.

Specialty loans

These FHA programs are tailored for specific needs:

- FHA Home Equity Conversion Mortgage (HECM): A reverse mortgage for seniors 62 and older, HECM lets you access your home’s equity as cash without selling the property. It’s a way to enjoy more financial freedom while staying in your home.

- Section 245(a) Loan: Expecting your income to grow? This option starts with lower monthly payments that increase over time, making it a perfect fit for young professionals or those with anticipated career advancements.

- FHA Manufactured Home Loans (Title II): Specifically for purchasing or refinancing manufactured homes, this loan program ensures affordability for non-traditional properties that meet FHA standards.

- FHA Construction-to-Permanent Loan: Perfect for building your dream home, this loan simplifies construction financing by automatically converting into a permanent mortgage once the home is complete.

FHA loan qualifications

Homeownership can be a liberating experience, especially for first-time home buyers. With flexible FHA loan qualifications and government backing, FHA loans offer an accessible path to owning a home.

Verify your FHA loan eligibility. Start hereHere’s what you need to know about FHA qualifications:

- Property standards: An FHA-approved appraiser must appraise the property, it must serve as the borrower’s primary residence, and it must meet basic FHA standards. Occupancy is required within 60 days of closing.

- Down payment: Borrowers with credit scores of 580 or higher need a 3.5% down payment, while those with scores between 500-579 must provide 10%.

- Mortgage insurance premiums (MIP): FHA loans require both an upfront mortgage insurance premium of 1.75% of the loan amount and an annual premium (typically 0.55%). The annual MIP can last for the loan’s life or reduce to 11 years with a larger down payment. Refinancing into a conventional loan can also eliminate FHA mortgage insurance.

- Credit score requirement: FHA loans accommodate FICO credit scores as low as 500, though a higher score (580+) opens up lower down payment options.

- Debt-to-income ratio (DTI): FHA prefers a DTI ratio of 43% or less but allows higher ratios, up to 50% in some cases, with compensating factors like strong credit or savings.

- Income and employment: Borrowers must demonstrate a stable employment history and income through documentation such as pay stubs, W-2s, tax returns, and bank statements.

FHA loan requirements offer affordability, and they give you the tools to keep your monthly mortgage payments manageable and take the next step toward owning your home.

Check your FHA loan rates. Start here

FHA loans vs. conventional loans

Choosing the right mortgage is an important step in your homeownership journey, and understanding the differences between an FHA loan and a conventional loan can help you make the best decision for your needs. Each loan type has its strengths, but they cater to different financial situations.

Verify your FHA loan eligibility. Start hereHere’s how an FHA loan stacks up against a conventional loan:

- Credit score qualifications: Got a few dings on your credit? An FHA loan is more forgiving, allowing lower credit scores—even for borrowers with past financial setbacks like credit card debt. Conventional loans, on the other hand, generally require higher credit scores to qualify.

- Mortgage insurance: An FHA loan comes with mortgage insurance premiums (MIP) for all borrowers, regardless of the down payment amount. This is part of what makes an FHA loan accessible to more buyers. Conventional loans only require private mortgage insurance (PMI) if your down payment is less than 20%, and PMI can eventually be removed once you build 20% equity in your home.

- Down payment flexibility: An FHA loan makes it easier to get help with your down payment. Whether it’s a gift from family, an employer, or even a charitable organization, FHA rules allow more flexibility. Conventional loans tend to have stricter guidelines for gifted funds.

- Property standards: When you’re buying a home with an FHA loan, the property must pass an FHA appraisal to ensure it meets government standards for health and safety. These appraisals are more detailed than the ones required for conventional loans, which don’t have the same inspection requirements.

- Debt-to-income ratios (DTI): If you’re carrying a lot of debt, an FHA loan might still work for you. It allows higher DTI ratios compared to conventional loans, making it a great option for borrowers balancing other financial obligations.

- Closing costs: An FHA loan may come with additional closing costs, such as the upfront mortgage insurance premium (UFMIP), which isn’t typically required for conventional loans.

An FHA loan is a great choice if you’re looking for flexibility and accessibility, while a conventional loan may save you money in the long run if you meet their stricter qualifications.

FAQ: FHA loans

Find out if you qualify for an FHA loan. Start hereSee if you qualify for an FHA loan

Now is an opportune time to consider an FHA loan, with current mortgage rates being historically competitive.

FHA loan interest rates are typically among the most competitive. To capitalize on these favorable rates, start by comparing offers from FHA-approved lenders.

You could find the most affordable loan with just a few clicks. Begin your journey towards homeownership today by exploring your options and discovering the best rates available for your financial situation.

Time to make a move? Let us find the right mortgage for you