Key Takeaways

- An FHA 203(k) loan finances a home purchase and renovation with a single mortgage.

- Borrowers use a 203(k) loan to repair, upgrade, or modernize a property.

- The 203(k) program offers Standard and Limited options for different amounts of renovation.

- This loan helps buyers afford fixer-uppers that may not qualify for traditional financing.

If you’re looking to build equity quickly and don’t mind remodeling a fixer-upper, an FHA 203(k) loan lets you finance the purchase and renovations with a single mortgage. Fixer-uppers often have less buyer competition, giving you a faster path to building equity. Here’s how to get started with the FHA 203(k).

In this article (Skip to...)

- How it works

- Types of 203(k) loans

- Eligible renovations

- Requirements

- Refinancing

- Lenders

- Alternatives

- How to apply

- FAQ

Want to see our expert mortgage insights first?

Add The Mortgage Reports as a preferred source on Google. You’ll automatically see our latest rate analyses, buying guides, and housing forecasts highlighted in your Google Search, AI Mode, and AI Overviews.

What is an FHA 203(k) loan?

An FHA 203(k) loan is a government-backed mortgage that lets you buy or refinance a fixer-upper and finance the repairs with a single loan and a single monthly payment. Often called a “rehab loan,” it solves a major problem for buyers because most lenders refuse to finance homes that need significant repairs. With a 203(k) loan, the lender tracks and verifies the renovation work, which makes it willing to approve financing on a property it would normally reject.

That said, the fixer-upper must still meet basic FHA safety and livability standards, and severely damaged properties may not qualify. This program appeals to buyers who want an affordable way into homeownership and prefer improving a lower-cost home rather than paying more for a move-in-ready property.

Check your 203(k) loan eligibility. Start here

How does the FHA 203(k) loan work?

The FHA 203(k) loan works by combining the cost of the home and its renovations into one loan. Borrowers submit renovation plans, including contractor bids and timelines, which are reviewed by the lender. The home is then appraised to determine its current value and its projected value after renovations. Based on this, the loan amount is calculated, ensuring it falls within FHA loan limits.

Once approved, the funds for the home purchase are disbursed at closing, while renovation funds are held in escrow and released in stages as the work is completed. The renovation must be finished within six months, with inspections along the way to ensure the work is on track.

Fast Fact

Although the FHA 203(k) loan involves more paperwork and oversight than a standard FHA loan, it offers the advantage of financing both the home and repairs with one loan, typically requiring a lower down payment and having more flexible qualification criteria.

Types of FHA 203(k) loans

There are two types of 203(k) loan options: Standard 203(k) loans, also known as Full 203(k) loans, and Limited 203(k) loans, also called Streamline 203(k) loans. Both are federally insured mortgages for buying and remodeling a home. However, each one is customized for a specific project type, based on the scope and cost of the planned renovations.

| Loan variant | Loan limit | Minimum loan | Eligible upgrades |

| Standard 203(k) | FHA loan limits for the county where property is located | No minimum | Major renovations: roof, plumbing, accessibility changes |

| Limited 203(k) | Up to $35,000 | At least $5,000 | Minor non-structural upgrades: paint, new appliances |

Standard FHA 203(k) Loans

Limited FHA 203(k) Loans

What can an FHA 203(k) loan be used for?

As we’ve already mentioned, there are two types of 203(k) loans: Standard and Limited. While both allow you to finance renovations, the type of work you can do depends on which loan you choose.

Check your 203(k) loan eligibility. Start hereThe Standard 203(k) loan is ideal for major renovations and can be used for a wide range of repairs and upgrades. Here are some of the renovations you can finance with this loan:

- Major structural alterations

- Converting a single-family home into a 2-, 3-, or 4-unit -home, or vice versa

- Connecting to public sewer or water

- Larger landscaping projects

- Improving accessibility for disabled persons

- Moving the house to a different site

- Plus everything that the Limited loan can do

The Limited 203(k) loan is designed for smaller-scale repairs and renovations. It’s perfect for cosmetic updates or repairs that don’t require major structural work. Some eligible renovations include:

- Small kitchen and bathroom remodels

- Appliance replacement

- HVAC upgrades or replacements

- Carpet and flooring

- Roofing replacement, including gutters and downspouts

- Painting

- Repairing health and safety hazards

- Energy-efficient home improvements

- Septic system improvements

While the FHA 203(k) loan can cover a wide range of renovations, certain luxury items and non-essential improvements are not eligible. Here’s what you can’t use the loan for:

- Luxury items such as swimming pools, hot tubs, outdoor kitchens, or saunas.

- Non-permanent items such as satellite dishes, garden fountains, and barbeque pits.

- Anything that doesn’t directly improve the functionality or structure of the home.

In these cases, other options might be a better fit, such as getting a home equity loan after purchase or other alternative rehabilitation loans.

Check your 203(k) loan eligibility. Start here

FHA 203(k) loan requirements for 2026

A 203(k) loan is a subtype of the popular FHA loan, which is meant to help those who might not otherwise qualify for a home loan. The FHA 203(k) loan requirements are flexible, which makes qualifying easier than a typical renovation loan.

Verify your FHA 203(k) loan eligibility. Start hereHere’s a breakdown of the main eligibility requirements for an FHA 203(k) loan:

- Credit score requirements

- Minimum credit score of 580, though some lenders may require 620–640.

- Lower threshold than the typical 720+ for conventional construction loans.

- Minimum down payment

- Down payment is 3.5% of the combined purchase price and project cost.

- Down payment assistance or gifts from family/non-profits are allowed.

- Example: For a $200,000 home plus $25,000 in renovations, the down payment is $7,875.

- Income and debt requirements

- Debt-to-income (DTI) ratio typically capped at 43%.

- For example, a $5,000 monthly income would mean a max of $2,150 for total monthly debts.

- Maximum loan amount

- Borrow up to 110% of the home’s estimated post-renovation value, or purchase price plus renovations, whichever is less.

- Must stay within FHA loan limits for the area (e.g., $2,211,600 in many regions).

- Mortgage insurance premiums

- Upfront Mortgage Insurance Premium (UMIP): 1.75% of the loan amount, paid at closing.

- Annual Mortgage Insurance Premium (MIP): 0.15%-0.75% of the loan amount, divided monthly.

- Occupancy and citizenship requirements

- Must use the property as a primary residence; not eligible for investment properties.

- Available to U.S. citizens and lawful permanent residents only.

Verify your 203(k) loan program eligibility. Start here

Refinancing with a 203(k) loan

People usually use the FHA 203(k) loan for buying homes, but it’s also suitable for refinancing. You can choose this refinancing option if your improvements cost at least $5,000. Lenders will require an appraisal to determine both the current property value and the improved value after renovations. The lowest of these three calculations sets the maximum refinance loan amount, within FHA loan limits:

- Add the existing debt before rehab to the estimated cost of improvements and allowable closing costs

- Add the as-is value to the rehab costs

- Multiple 110% of the after-improved value by 97.75%

If the property has been owned for less than a year, the lender must consider the purchase price plus documented rehabilitation costs to determine the maximum loan amount. You do not need to have an existing FHA loan to qualify for an FHA 203(k) loan for refinancing.

Where can I get an FHA 203(k) loan?

You can obtain an FHA 203(k) loan through an FHA-approved lender, but not all lenders offer this program or have loan officers who understand how it works. Before applying, verify that the lender regularly underwrites 203(k) loans and has experience with the renovation process. The U.S. Department of Housing and Urban Development (HUD) offers an online search tool that allows you to check if a lender has completed at least one 203(k) loan in the past year. Enter the lender’s name in the search bar, scroll to the program list, and select the 203(k) rehabilitation mortgage insurance option to confirm their participation.

Check your home buying options. Start hereFHA 203(k) loan: Pros and cons

You can find inexpensive fixer-uppers that require updating or repairs, and the repairs themselves might not cost much. For example, a house that could be worth $250,000 might sell for only $200,000 when it requires just $20,000 in repairs. That leaves $30,000 in potential equity for a buyer with the initiative to manage the fixes.

Verify your 203(k) loan program eligibility. Start hereStill, this strategy isn’t right for everyone.

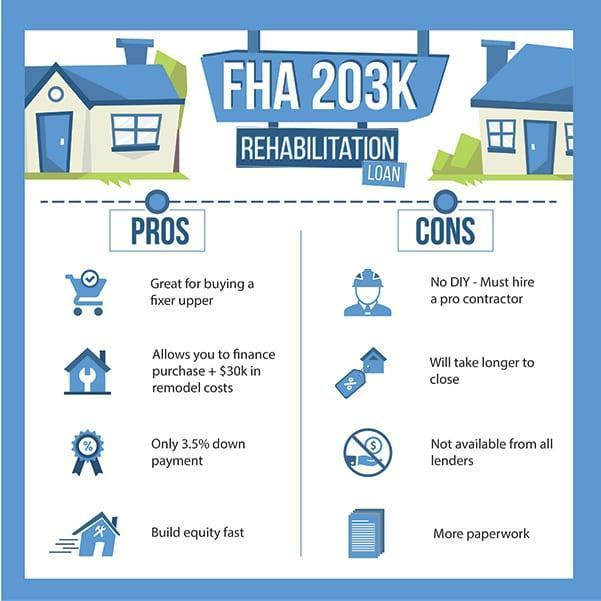

FHA 203(k) pros

- Instant equity potential: Purchase a property below market value and gain equity after repairs are complete.

- Less competition: Fewer buyers are interested in homes needing repairs, which can make purchasing easier.

- Remodeling experience: Gain hands-on experience with home remodeling, adding to your homeowner skills.

- Discounted purchase prices: Distressed properties may be discounted by as much as 42% compared to standard listings, according to Realtytrac.

FHA 203(k) cons

- Mortgage insurance costs: Mortgage insurance premiums are required until the loan is paid off or refinanced.

- Licensed contractor requirement: Must work with licensed contractors and ensure proper documentation for all repairs.

- Bid revisions: Lenders may require multiple bid revisions with the contractor for approval.

- Upfront repair decisions: Must decide on repairs and stay within budget before finalizing the loan.

- Extended loan process: Requires more paperwork than a traditional loan, so expect longer processing times—typically much longer than a 15-day close. Set realistic timelines with the seller.

Alternatives to an FHA 203(k) loan

There are several reasons why FHA 203(k) might not be your best option. You may need only a few thousand dollars for minor work, for example. Or your home renovation could exceed FHA guidelines due to its luxury or high cost. You might even prefer to handle the work on your own. Or you’d prefer a renovation loan that doesn’t require mortgage insurance for life.

Verify your FHA 203(k) loan eligibility. Start hereThankfully, there are other home improvement loans. One might be a better fit.

FHA 203(k) loans versus conventional home rehab loans

Conventional home rehabilitation loans and FHA 203(k) loans are both designed to help borrowers purchase and renovate homes. But they have distinct characteristics, requirements, and benefits.

| Conventional rehab loans | FHA 203(k) loans | |

| Origination | Private lenders, no specific government backing. | Backed by the Federal Housing Administration. |

| Eligibility | Higher credit score, lower debt-to-income ratio. | More lenient on credit score, smaller down payment. |

| Property restrictions | Flexible property types. | One-to-four units, at least a year old. |

| Loan limits | Typically higher. | Set by county, based on local home prices. |

| Renovation restrictions | Upgrades that add value. | Essential repairs/improvements for home safety. |

| Mortgage insurance | PMI required < 20% down; can be removed once equity is built. | Upfront & annual premium; stays for life of loan unless refinanced. |

Remember, when choosing between these loans, it’s all about what fits your situation best. Talk to a trusted mortgage professional and weigh the pros and cons. Because while buying a fixer upper can be a wild ride, being informed makes it all a bit smoother.

How to get an FHA 203(k) loan

Applying for a 203(k) loan is a multi-step process that involves a bit more paperwork and time than a standard loan application due to the additional requirements related to the renovation plans.

Verify your FHA 203(k) loan eligibility. Start hereHere’s a detailed look at the steps involved:

1. Choose your home improvement projects

The first step of an FHA 203(k) loan is deciding which home improvements or modernizations you want to do (see a list of qualifying repairs below). The lender will require any safety or health hazards to be addressed first, including repairs like mold, broken windows, derelict roofing, lead-based paint, and missing handrails.

From there, you choose which cosmetic improvements you want to take care of, such as updating appliances, adding granite countertops in the kitchen, or installing a new bathroom. These types of updates are all eligible uses for this remodel loan.

2. Determine your eligibility

Make sure you meet the eligibility criteria for a 203(k) loan. This typically includes having a credit score of at least 620 and a debt-to-income ratio of less than 43%. The property must also meet eligibility criteria: it must be a one- to four-unit dwelling that is at least one year old.

3. Find a suitable property and plan your renovations

Search for a property that you’d like to buy and renovate. Make a detailed plan of the improvements you wish to make, including cost estimates. For a Full 203(k) loan, your plan must involve at least $5,000 worth of renovations, while a Streamline 203(k) loan must not exceed $35,000 in renovation costs.

4. Choose your contractors

The next step is to find licensed contractors. Qualifying contractors must be licensed and insured, and they typically have to be in full-time business. You can’t use buddies who do construction on the side, and you typically can’t do the work yourself unless you’re a licensed contractor by profession.

The best results will come from experienced and professional remodeling firms that have done at least one 203(k) renovation in the past. Be aware that one contractor’s refusal to complete the required forms could delay your entire project. So you might even go so far as to write the 203(k) paperwork requirements into the contractor agreement.

5. Get your bids

Once your contractor is on board with helping you complete your loan application, get official bids. Make sure the bids aren’t guesses. They must be completely accurate because the lender will submit final bids to the appraiser, who builds the value of the work into the future value of the property, upon which your loan is based.

Changing bid dollar amounts later could incur additional appraisal costs and trigger a re-approval with the lender. Again, make sure your contractor knows all this!

6. Choose a 203(k)-approved lender and provide documentation

Not every lender offers 203(k) loans, so it’s important to find a lender who is familiar with the specifics of the 203(k) loan process. You can find a list of approved lenders on the Department of Housing and Urban Development (HUD) website.

You will need to provide a range of documentation to support your application. This may include pay stubs, W-2s, tax returns, details about your debts, and a written proposal for your planned renovations.

7. Property appraisal and feasibility study

For a Full 203(k) loan, the lender will arrange for a HUD-approved consultant to visit the property. The consultant will perform a feasibility study and review your proposed improvements to ensure they increase the property’s value and meet HUD’s Minimum Property Standards and local code requirements. For a Streamline 203(k), a consultant isn’t needed, but the property will still need to be appraised.

8. Closing the loan

Once the loan is approved, you’ll proceed to closing, where you’ll sign all of the loan documents. The renovation funds from your loan will be put into an escrow account to be released as work is completed.

9. Overseeing renovation work

Renovation work must start within 30 days of closing your loan. For a Full 203(k) loan, you’ll work with your consultant to oversee progress.

Depending on the extent of the repairs, you may be able to move in at the same time. But for bigger projects, arrange to live somewhere else until work is complete. You can finance up to six months of mortgage payments into your loan amount to allow room in your budget to do so.

10. Move into your renovated home

The work is complete, and you’re the owner of a beautiful new home. You’ve built home equity early on, and you didn’t have to engage in a bidding war to buy your ideal home.Plus, you may be able to refinance out of the FHA loan and the mortgage insurance premium (MIP) that comes with it.

FAQs about FHA 203k loans

Check your FHA 203(k) loan options. Start hereFinal thoughts about the FHA 203(k) rehab loan

It’s always wise to shop around for best mortgage lender. But with a 203(k) loan, you may not always want the lender with the lowest interest rate.

It’s often better to accept a higher interest rate if it’s coming from a lender with more 203(k) loan experience than the lender who’s offering a lower rate. This is a rare exception in mortgage shopping, in which the lowest rate may not be in your best interest.

In the world of 203(k) loans, contractor and lender experience is typically more of a consideration than cost. Click the link below to begin your search for the best FHA 203(k) loan lender for your financial needs.

Time to make a move? Let us find the right mortgage for you