Mortgage rate forecast for next week (Aug 10 - 14)

Mortgage rates rose for a fifth straight week, marking five consecutive weekly gains.

The average 30-year fixed rate mortgage (FRM) increased to 6.69% on August 6, 2026 from 6.66% the prior week, according to Freddie Mac.

The 30-year fixed-rate mortgage averaged 6.69% this week. While mortgage rates continue to influence affordability, the housing market is showing signs of adjustment, with listing prices modestly below year-ago levels and for-sale inventory improving from the limited supply seen in recent years.

| Average 30-year fixed rate | 1-week ago | 4-weeks ago | 3-months ago | 1-year ago |

| 6.69% | 6.66% | 6.49% | 6.37% | 6.72% |

The latest borrowing activity

Though lagging, the most recent weekly mortgage application report from the Mortgage Bankers Association showed a seasonally adjusted 0.8% decrease for the seven days ending March 27. The refinance index fell 3% week-over-week while standing 4% lower from a year ago. The purchase index rose 1% weekly but came down 7% year-over-year.

“Outside of Fed policy, the U.S.-Iran War will remain in focus. The longer the conflict takes to resolve, the longer the expectation of higher inflation will remain. Higher energy prices resulting from a closed Strait of Hormuz will keep US inflation higher than hoped. Higher inflation generally means higher mortgage rates.” says Charles Goodwin, VP and Head of Bridge and DSCR Lending at Kiavi

Find your lowest mortgage rate. Start here🎧 Listen to this article (18 min)

In this article (Skip to...)

- Will rates go down in June?

- 90-day forecast

- Expert rate predictions

- Mortgage rate trends

- Rates by loan type

- Mortgage strategies for June

- Mortgage rates FAQ

Will mortgage rates go down in July?

Mortgage rates enter July near 6.49%, holding within the mid-6 percent range they have occupied for weeks. The 30-year fixed has barely moved over the past month, signaling a market waiting for a fresh catalyst.

- Dave Meyer, Chief Investment Officer at BiggerPockets

Want to see our expert mortgage insights first?

Add The Mortgage Reports as a preferred source on Google. You’ll automatically see our latest rate analyses, buying guides, and housing forecasts highlighted in your Google Search, AI Mode, and AI Overviews.

The next FOMC meeting is not until July 28-29, 2026, so the first three weeks of the month carry no scheduled Fed decision. Two inflation reports stand between now and then: the CPI release on July 15 from the Bureau of Labor Statistics and the PCE release on July 31 from the Bureau of Economic Analysis. Those readings will shape expectations heading into the meeting.

With the FOMC having held steady at its April 29, 2026 meeting, markets have little reason to price a sharp move before late July. The CPI print mid-month is the most likely source of volatility before then.

The likeliest path for July is rates holding broadly flat near current levels. A clear directional move would require a surprise in the inflation data or a shift in tone from the Fed at the end of the month.

Expert mortgage rate predictions for July

Dave Meyer, Chief Investment Officer at BiggerPockets

Prediction: Rates will hold steady

Mortgage rates are unlikely to change in any meaningful way, despite the outcome of the upcoming Fed meeting. The bond market and mortgage market are already pricing in the inflationary pressure from the conflict in Iran. Until that eases, mortgage rates won’t be coming down.

Charles Goodwin, VP and Head of Bridge and DSCR Lending at Kiavi

Prediction: Rates will hold steady

Mortgage rates have increased back into the 6.60-6.70% range due to inflation expectations and hawkish commentary from the Fed. The Memorandum of Understanding between the US and Iran appears broken, and oil prices have increased again in the past week. Furthermore, commentary from the Fed has been clearly hawkish, with numerous Fed members and Fed Chair Warsh focusing more on the inflation narrative than the labor narrative. Expect rates to stay in this range barring any breakthroughs in the Middle East, easing inflation data, or very weak labor data.

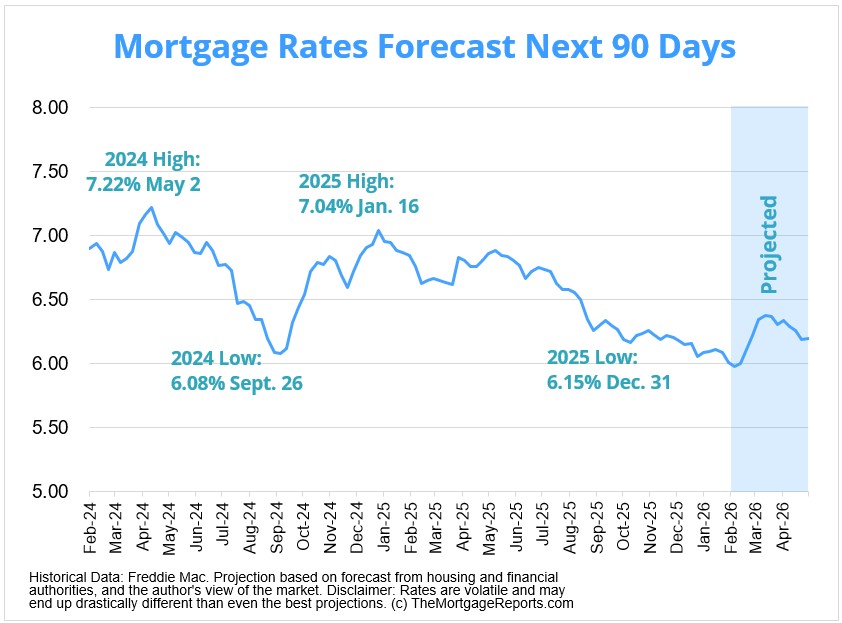

Mortgage interest rates forecast next 90 days

The Fed held steady at its April 29, 2026 meeting and does not meet again until July 28-29, 2026. That late-July decision is the key policy event on the near-term calendar, and markets will weigh incoming data against it through the first three weeks of the month.

Inflation data will guide the read into that meeting. The CPI release on July 15 from the Bureau of Labor Statistics offers the first major signal, followed by the PCE release on July 31 from the Bureau of Economic Analysis. A cooler-than-expected CPI print could ease pressure on bond yields, while a hot reading could push them higher.

Find your lowest mortgage rate. Start hereBorrowers watching the next 90 days should track those two reports along with the July 28-29 FOMC outcome. The 10-year Treasury note, which mortgage rates loosely follow, will react to each release.

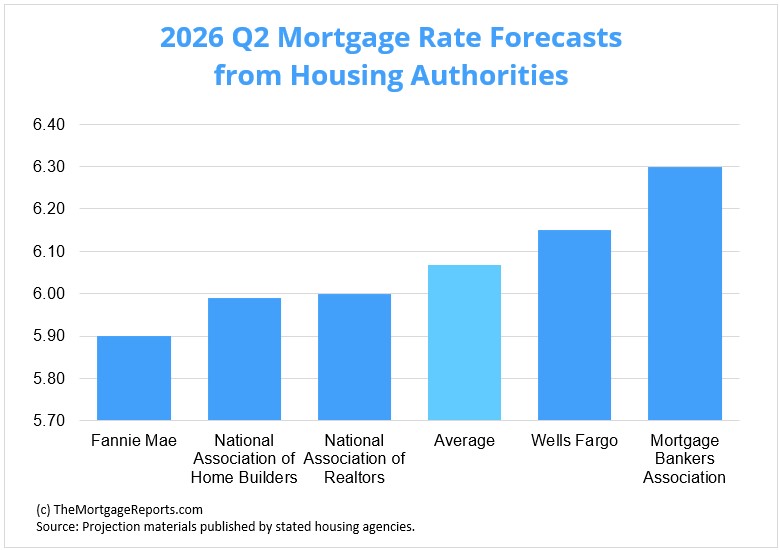

Mortgage rate predictions for July 2026

The major housing authorities publish quarterly-average forecasts. For Q2 2026, both Fannie Mae and the Mortgage Bankers Association place the 30-year fixed at 6.40%, for an average of 6.400%.

That Q2 2026 quarterly-average figure sits just below the current 6.49% reading, consistent with a market holding near current levels rather than moving sharply in either direction.

| Housing Authority | 30-Year Mortgage Rate Forecast (Q2 2026) |

| Fannie Mae | 6.40% |

| Mortgage Bankers Association | 6.40% |

| Average Prediction | 6.400% |

Current mortgage interest rate trends

As of August 6, 2026, Freddie Mac’s weekly survey shows the average 30-year fixed mortgage increased to 6.69%.

The average 30-year fixed rate increased to 6.69% on Aug. 6 from 6.66% on Jul. 30. Meanwhile, the average 15-year fixed mortgage rate dipped to 6.01% from 6.04%.

| August 2026 | 6.69% |

| July 2026 | 6.66% |

| June 2026 | 6.49% |

| May 2026 | 6.53% |

| March 2025 | 6.65% |

| April 2025 | 6.73% |

| May 2025 | 6.82% |

| June 2025 | 6.82% |

| July 2025 | 6.72% |

| August 2025 | 6.59% |

| September 2025 | 6.35% |

| October 2025 | 6.25% |

| November 2025 | 6.24% |

| December 2025 | 6.19% |

Source: Freddie Mac

After hitting record-low territory in 2020 and 2021, mortgage rates climbed to a 23-year high in 2023 before descending over 2024 and 2025. Many experts and industry authorities believe they will follow a downward trajectory in 2026. Whatever happens, interest rates are still below historical averages.

Dating back to April 1971, the fixed 30-year interest rate averaged around 7.8%, according to Freddie Mac. So if you haven’t locked a rate yet, don’t lose too much sleep over it. You can still get a good deal, historically speaking — especially if you’re a borrower with strong credit.

Just make sure you shop around to find the best lender and lowest rate for your unique situation.

Mortgage rate forecast by loan type

Loan-type trends were mixed this week, with 30-year fixed at 6.69% and 15-year fixed at 6.01%.

Find your lowest mortgage rate. Start hereWhich mortgage loan is best?

The best mortgage for you depends on your financial situation and your goals.

For instance, if you want to buy a high-priced home and you have great credit, a jumbo loan is your best bet. Jumbo mortgages allow loan amounts above conforming loan limits, which max out at $832,750 in most parts of the U.S.

On the other hand, if you’re a veteran or service member, a VA loan is almost always the right choice. VA loans are backed by the U.S. Department of Veterans Affairs. They provide ultra-low rates and never charge private mortgage insurance (PMI). But you need an eligible service history to qualify.

Conforming loans and FHA loans (those backed by the Federal Housing Administration) are great low-down-payment options.

Conforming loans allow as little as 3% down with FICO scores starting at 620. FHA loans are even more lenient about credit; home buyers can often qualify with a score of 580 or higher, and a less-than-perfect credit history might not disqualify you.

Finally, consider a USDA loan if you want to buy or refinance real estate in a rural area. USDA loans have below-market rates — similar to VA — and reduced mortgage insurance costs. The catch? You need to live in a ‘rural’ area and have moderate or low income to be USDA-eligible.

Mortgage rate strategies for July 2026

With the 30-year fixed near 6.49% and no FOMC decision until July 28-29, rates look set to hold broadly flat through most of July. That stability gives borrowers room to plan rather than react.

Find your lowest mortgage rate. Start hereThe CPI release on July 15 and the PCE release on July 31 are the data points most likely to move rates before the Fed meets. A surprise in either direction could shift pricing.

The strategies below help borrowers act in a flat-rate environment without overpaying for the wait.

With rates holding near 6.49%, locking now removes the risk that the July 15 CPI report or the late-July FOMC meeting pushes rates higher. A lock protects your quoted rate for a set period.

Rate lock strategy

If you are within your lender’s lock window and comfortable with current pricing, locking is a reasonable choice. Ask about float-down options in case rates improve before closing.

Refinancing makes sense when the new rate and term improve your financial position enough to offset closing costs. Calculate your break-even point before moving forward.

With rates roughly a quarter point below year-ago levels, some borrowers who locked at higher rates may find savings. Run the math against your current loan to confirm.

Buyers facing a flat-rate market can focus on the parts of the deal they control: price negotiation, down payment, and lender selection. Waiting for a sharp rate drop carries no guarantee in current conditions.

Get preapproved so you can move quickly when the right property appears. A solid preapproval also strengthens your offer in competitive markets.

Refinance timing

Your credit score directly affects the rate you are offered. Improving it before you apply can lower your borrowing cost.

Steps that help include the following:

Pay down revolving balances to lower your credit utilization | Avoid opening new accounts before applying | Check your credit reports for errors and dispute them | Make all payments on time in the months before you apply

Even a modest score improvement can move you into a better pricing tier. The effort pays off across the life of the loan.

Home buying strategy

Pair credit work with rate shopping across multiple lenders. Combining both gives you the strongest position in a flat market.

Whatever your timeline, base your decision on your own finances rather than trying to time the market.

- Your credit score and credit history

- Your personal finances

- Your down payment (if buying a home)

- Your home equity (if refinancing)

- Your loan-to-value ratio (LTV)

- Your debt-to-income ratio (DTI)

To figure out what rate a lender can offer you based on those factors, you have to fill out a loan application. Lenders will check your credit and verify your income and debts, then give you a ‘real’ rate quote based on your financial situation.

You should get three to five of these quotes at a minimum, then compare them to find the best offer. Look for the lowest rate, but also pay attention to your annual percentage rate (APR), estimated closing costs, and ‘discount points’ — extra fees charged upfront to lower your rate.

This might sound like a lot of work. But you can shop for mortgage rates in under a day if you put your mind to it. And shaving just a few basis points off your rate can save you thousands.

Compare mortgage and refinance rates. Start here

Mortgage interest rate FAQ

What are today’s mortgage rates?

Mortgage rates are rising, but borrowers can almost always find a better deal by shopping around. Connect with a mortgage lender to find out exactly what rate you qualify for.

Time to make a move? Let us find the right mortgage for you1Today's mortgage rates are based on a daily survey of select lending partners of The Mortgage Reports. Interest rates shown here assume a credit score of 740. See our full loan assumptions here.

Selected sources:

- https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- http://www.freddiemac.com/research/datasets/refinance-stats/index.page