Key Takeaways

- Conventional loans are widely available and can require as little as 3% down with a 620 credit score.

- Your credit score, income, and debt levels play a major role in your rate, costs, and approval.

- Comparing multiple lenders can help you secure a lower interest rate and reduce your overall loan costs.

Due to their competitive rates and wide availability, conventional loans are the most popular mortgage for home purchases and refinances. This is why understanding the conventional loan requirements will help you get the best deal on a mortgage.

Conventional home loans are the closest you can get to a “standard” mortgage. Most lenders offer them, and you can qualify with just 3% down and a 620 credit score. Here’s what to know about conventional loan requirements.

In this article (Skip to...)

- Conventional loan definition

- Loan requirements

- Loan limits

- Conventional rates

- Benefits

- Alternatives

- FAQ

What is a conventional loan?

A conventional loan is any mortgage not backed by the federal government. Most conventional loans also fall into the category of “conforming loans.” These mortgages meet lending standards set by Fannie Mae and Freddie Mac.

Check your conventional loan eligibility. Start hereAlthough Fannie and Freddie regulate them, private lenders offer conventional loans. You can get one from any bank, credit union, mortgage lender, or mortgage broker. In fact, most U.S. mortgages are conventional loans. And if you’re buying a home, there’s a good chance this is the type of loan you’ll use. So here’s what you should know about conventional loan requirements.

Conventional loan requirements 2026

In general, any borrower with solid credit, stable income, and some money for a down payment will satisfy conventional loan qualification requirements. However, because conventional loans aren’t insured or guaranteed by a federal agency, their eligibility requirements for borrowers are usually tougher to meet than for government-backed mortgages.

Verify your home buying eligibility. Start hereConventional loan requirements vary by lender. But most conventional loans must meet the guidelines Fannie Mae and Freddie Mac set. These include:

- Minimum credit score requirement of 620

- Minimum down payment requirement of at least a 3%

- Maximum debt-to-income ratio of 43% (can be up to 49%, depending on qualifying factors)

Also, remember that conventional lenders are free to enforce stricter requirements than the guidelines set by Fannie and Freddie. If you’re applying for a conventional mortgage after foreclosure or bankruptcy, you might have more trouble qualifying.

Credit score

The minimum credit score for most conventional loans is just 620. But some lenders may have a higher credit score requirement than others. A slightly lower credit score may be allowed. But the lender typically charges a higher interest rate to compensate for the greater risk. On the other hand, those with higher credit scores will likely qualify for lower rates.

“We want to know that people pay their bills on time, and are financially disciplined and good at money management,” says Staci Titsworth, regional vice president sales manager with PNC Mortgage in Pittsburgh, PA.

Applicants with lower scores or a blemished credit history may want to choose an FHA loan. This loan option does not charge extra fees or higher rates for borrowers with lower credit scores.

Be sure to check your credit report before applying for a mortgage loan, so you’ll know where you stand.

Check your home buying options. Start hereDown payment

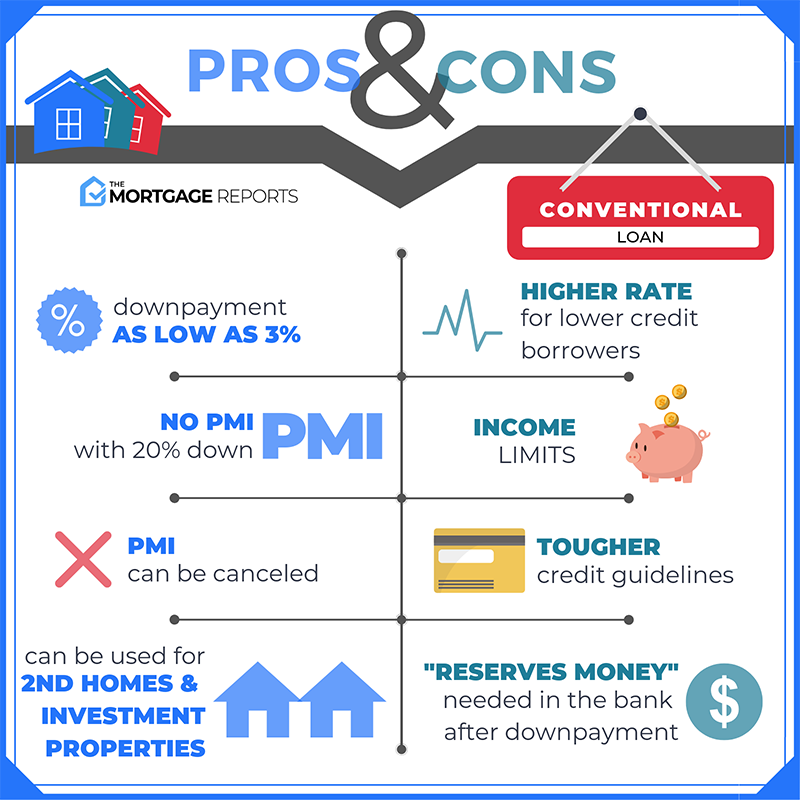

Repeat and first-time home buyers usually get a conventional mortgage loan with a down payment as low as 3%. But this conventional loan requirement is not set in stone. That’s because lenders can have different down payment rules depending on your mortgage needs. Here’s what to expect.

- 5% down payment for repeat home buyers and those who earn less than 80% of the area median income (AMI)

- 5% down if you’re financing with an adjustable-rate mortgage

- 10% down payment if you’re buying a second home

- 15% down payment for those purchasing a multi-unit property, as opposed to a single-family home

Experimenting with a mortgage calculator will help you determine how much your future monthly payments could cost, depending on the size of your down payment and interest rate.

Private mortgage insurance

When you put less than 20% down on a conventional loan, your lender will require private mortgage insurance (PMI). This coverage helps protect the lender if you default on the loan.

PMI does increase monthly mortgage payments. But that’s OK if it allows you to get a conventional loan with a down payment you can afford. Also, note that conventional PMI can be canceled later, once your home reaches at least 20% equity. So you’re not stuck with it forever.

Debt-to-income ratio

The buyer’s debt-to-income ratio (DTI) also influences conventional loan qualifying. DTI compares your total monthly debts (including mortgage costs) to your gross monthly income. Your lender uses DTI to determine how much a mortgage fits within your monthly budget.

Many lenders want this ratio to be less or equal to 36% of the borrower’s income. However, conventional loans may allow a DTI as high as 49%.

To find your debt-to-income ratio, add up your loan payments, including:

- Student loans

- Personal loans

- Car loans

- Credit card minimum payments

- Your projected mortgage payment

Also add in any child support or alimony payments you’re required to make each month. Then divide that sum by your gross monthly income.

Employment and income requirements

During the mortgage preapproval process, home buyers must provide proof of earnings. This may involve some or all of the following documentation:

- 30 day’s pay stubs

- 2 year’s W2s

- 2 year’s tax returns if self-employed

- 2 year’s bank statements

- An offer letter, if you’ve not yet started a new job

- Proof of education for new graduates

“Most lenders require two-year documentation to show a consistent earnings stream,” Titsworth says.

Alimony can also be counted if documented in a divorce decree, along with the recurring payment method, such as an automatic deposit. Seasonal income is also accepted with proof in a tax return.

Check your home buying options. Start hereProperty requirements

A lender won’t approve a mortgage for an amount greater than the home’s value. Before closing on the loan, the lender will appraise the property to determine its fair market value.

As an example, let’s say a buyer has agreed to pay $400,000 for a home, but the appraisal comes in at $380,000

- In this case, the home buyer should use this appraisal as a bargaining chip to get the seller to lower the price to a level the lender will finance

- Or, the buyer could pay the additional $20,000 out of pocket to compensate for the lower borrowing limit. This $20,000 would be added to the down payment you’d already agreed to pay

Property value isn’t the only thing to watch for when getting a conventional loan appraisal. Sometimes during a home inspection, the appraiser may require another professional’s opinion.

“If the appraiser sees water stains or a lot of leaky faucets, he may request a plumbing inspection. The seller may need to make improvements, which could delay a closing,” Titsworth says.

However, conventional loans have less strict appraisal and property requirements than FHA, VA, or USDA loans. This is another advantage to conventional: You can qualify for a home in slightly worse condition, and plan to make the repairs after your loan is approved and you move in.

Closing costs

Closing costs include underwriting fees, such as a lender’s origination fee. Plus, expect vendor fees for an appraisal, title insurance, and credit reporting fees.

Sometimes, a lender or seller will pay all or some of these expenses, depending on the strength of the market and desire to close the transaction. Check whether your chosen lender offers lender credits. Also ensure that any seller contributions are within Fannie Mae and Freddie Mac’s conventional loan requirements.

Typically, sellers and other interested parties can contribute the following amounts, based on the home price and down payment amount.

- Less than 10% down: 3% of the purchase price

- 10 to 25% down: 6% of the purchase price

- More than 25%: 9% of the purchase price

With a rental or investment property, the seller can only contribute 2% of the purchase price toward closing costs.

Conventional loan limits 2026

The amount of money you borrow with a conventional loan must also fall within conforming loan limits. In 2026, that’s $832,750 in most areas, but more in some high-cost areas. The Federal Housing Finance Agency (FHFA) evaluates these limits every year.

Check your conventional loan eligibility. Start hereFor instance, Fannie Mae and Freddie Mac allow a loan amount of up to $1,249,125 in certain high-priced ZIP codes.

Home buyers who need a loan amount above the standard limit should check for the specific limit for their area. Loans exceeding an area’s conventional loan limits are considered non-conforming loans. These require a jumbo loan, not a conventional loan.

You can check conventional loan limits in your area using this search tool.

Conventional loan rates

Today’s average rate for a conventional loan starts at 6.609% (6.68% APR) for a 30-year, fixed-rate mortgage, according to our lender network.

For a 15-year conventional loan, the average rate drops to 5.992% (6.097% APR).

Check your conventional loan rates. Start hereToday’s conventional loan rates (July 20, 2026)

| Loan type | Average Interest Rate* | APR* |

| Conventional 30-Year FRM | 6.609% | 6.68% APR |

| Conventional 15-Year FRM | 5.992% | 6.097% APR |

*Average rates reported daily by TheMortgageReports.com lender network. Your own interest rate will be different. See our full loan assumptions here.

Conventional loan rates are heavily based on the applicant’s credit score — more so than rates for FHA loans. For instance, a home buyer with a 740 score and 20% down will be offered about a 0.50% lower rate than a buyer with a 640 score.

Rates are also based on mortgage-backed securities (MBS), which are traded just like stocks. And like stocks, conventional loan rates change daily, and throughout the day.

Shop around with at least three different lenders

When you’re shopping for a mortgage, it’s important to get personalized rate quotes. Published rate averages often depend on the perfect applicant with great credit and a large down payment. Your rate might be higher or lower.

It pays to get at least three written quotes from different lenders, no matter which loan term or loan type you choose. According to a government study, applicants who shopped around receive rates up to 0.50% lower than those non-shopping.

Get a conventional rate quote based on your information, not on the information of an average buyer.

Benefits of a conventional home loan

Conventional loans are arguably the most popular type of mortgage. However, government-backed mortgages have some unique benefits, including small down payments and flexible credit guidelines. First-time home buyers often need this kind of leeway.

Check your conventional loan eligibility. Start hereBut conventional loans can outshine government-backed loans in several ways.

1. Flexible repayment plans

As with most mortgages, conventional loans offer several repayment options. Conventional loans come in 10, 15, 20, 25, and 30-year terms. Some lenders even let you choose your own loan term, for instance, between 8 and 30 years.

The shorter your loan term, the lower your interest rate should be. But your monthly payment will be higher, because you’re paying off the same loan amount in a shorter time.

Fortunately, a 30-year fixed-rate conventional loan still comes with relatively low fixed-interest payments that are accessible to the majority of home buyers and refinancers.

2. Adjustable rates available

Conventional loans are also a smart choice for those who aren’t staying in their home long and want a short-term adjustable-rate mortgage. This option has a lower interest rate than a fixed-rate loan.

Adjustable rates are fixed, but only for a period of time — usually 3, 5, or 7 years. During that initial fixed-rate period, the homeowner pays lower interest and can save thousands.

Today’s home buyers often choose a 5-year ARM or 7-year ARM. These loans can provide thousands in savings, giving the home buyer enough time to refinance into a fixed-rate loan, sell the home, or pay off the mortgage entirely.

But after this low introductory rate expires, the loan’s interest rate and monthly mortgage payment could decrease or increase each year, depending on market conditions. This makes ARM loans inherently risky for homeowners, and an option that should be considered carefully.

Check your adjustable mortgage rates. Start here3. No upfront mortgage insurance fee

Conventional loans do not require an upfront mortgage insurance fee, even if the buyer puts less than 20% down.

FHA, USDA, and even VA loans require an upfront insurance fee, usually between 1% and 4% of the loan amount. Conventional loans only require a monthly mortgage insurance premium when the homeowner puts down less than 20%.

Plus, conventional mortgage insurance may be lower than government loans if you have good credit and a decent down payment.

Conventional loan alternatives

Conventional loans are the least restrictive of all loan types. There’s a lot of flexibility around the down payment, eligibility guidelines, and types of property you can buy with conventional financing. However, there are government-backed home loans designed to help people achieve their homeownership goals when a conventional loan may not be the best mortgage program available to them.

Check your home buying options. Start hereKeep in mind these government mortgages have specific purposes and come with various limitations:

- FHA loans are guaranteed by the Federal Housing Administration. These loans are a powerful home buying tool, but they come with high mortgage insurance fees that are required for the life of the loan — up to 30 years. The only way to cancel FHA mortgage insurance is to refinance the FHA loan, which would require paying closing costs again

- VA loans are backed by the Department of Veterans Affairs and are only available to current and former military service members. They offer many benefits, like zero down payment and no monthly mortgage insurance. But they are not available to the general population

- USDA loans are guaranteed by the U.S. Department of Agriculture. These loans are only available in designated rural areas. For those who qualify, USDA loans allow zero down payment and have low interest rates on average

Additionally, most loan programs provided by government agencies can’t be used for second homes or investment properties. They’re designed to help Americans buy single-family homes to be used as a primary residence.

First-time and repeat buyers can land a good value when choosing a conventional loan for their home purchase. And, more buyers qualify for this loan than you might expect.

Conventional loan requirements FAQ

Check your home buying eligibility. Start hereFind out if you meet the conventional loan requirements

Conventional home loans have low down payment requirements, which makes them a great option for many first-time home buyers. Check your conventional loan eligibility with a lender. If you don’t qualify, apply with another. It’s best to get preapproval with several lenders and compare their quotes. Get started today with the link below.

Time to make a move? Let us find the right mortgage for you