Your lender asked for a letter of explanation. What now?

When you apply for a home loan, your lender will do a deep dive into your financial history. Depending on what it finds in your bank statements or credit report, additional documentation may be necessary.

Start your mortgage application todayYou may be asked for a “letter of explanation” during the application process. Fear not. Letters of explanation are fairly standard and nothing to worry about.

However, you want to make sure you write this letter correctly, as it could be crucial to your mortgage approval.

Here’s everything you need to know so you can hit a home run with your letter of explanation.

In this article (Skip to...)

What is a mortgage letter of explanation?

Commonly referred to as an ‘LOE’ or ‘LOX,’ letters of explanation are often requested by lenders to gain more specific information on a mortgage borrower and their situation.

An LOX can necessary when there is inconsistent, incomplete, or unclear information on a loan application.

Letters of explanation may be required if any red flags turn up during the underwriting process, such as:

- Declining income

- Gaps in your employment history

- Differing names on your credit report

- Large deposits or withdrawals in your bank account

- Recent credit inquiries

- An address discrepancy on your credit report

- Derogatory items in your credit history

- Late payments on credit cards or other debts

- Overdraft fees on an account

There are many other situations where an LOX may be requested, too.

If you need to write one, be sure to ask your loan officer what exactly the underwriter wants to see, and whether you need to provide any supporting documentation along with the letter.

How to write a letter of explanation for your mortgage lender

When it comes to mortgage letters of explanation, less is typically more.

Start your mortgage application todayToo much unnecessary information may lead to confusion, or at minimum, additional questions about your file — questions that may have been avoided if it weren’t for some of the details in your letter.

The most important elements of your letter of explanation should include the following:

- Facts — Be honest. Never be tempted to write a letter based on solely on what you may think your lender wants to hear. You shouldn’t fabricate any aspect of your letter. Include correct dates, dollar amounts, and any other pertinent details for your situation

- Resolution — Your lender wants to know how and when the situation that led up to certain events was resolved. For instance, if you were temporarily furloughed during COVID, but you’ve since returned to full employment, you should be able to document your recent paystubs and have your employer verify that you’ll continue working full time for the foreseeable future

- Acknowledgement — This one is important and shouldn’t be left out of your letter. Mortgage underwriters want to know why it is that something happened, and how or why it won’t happen again in the future

Remember that a letter of explanation is a professional document that will go into your loan file.

Be mindful of things like spelling, grammar, and punctuation. Create a letter that’s visually appealing, properly formatted, and communicates the relevant information.

Providing additional documentation with your letter can be helpful. For example, if hospitalization was the culprit behind some missed payments on your credit report, it may be helpful to include hospital bills.

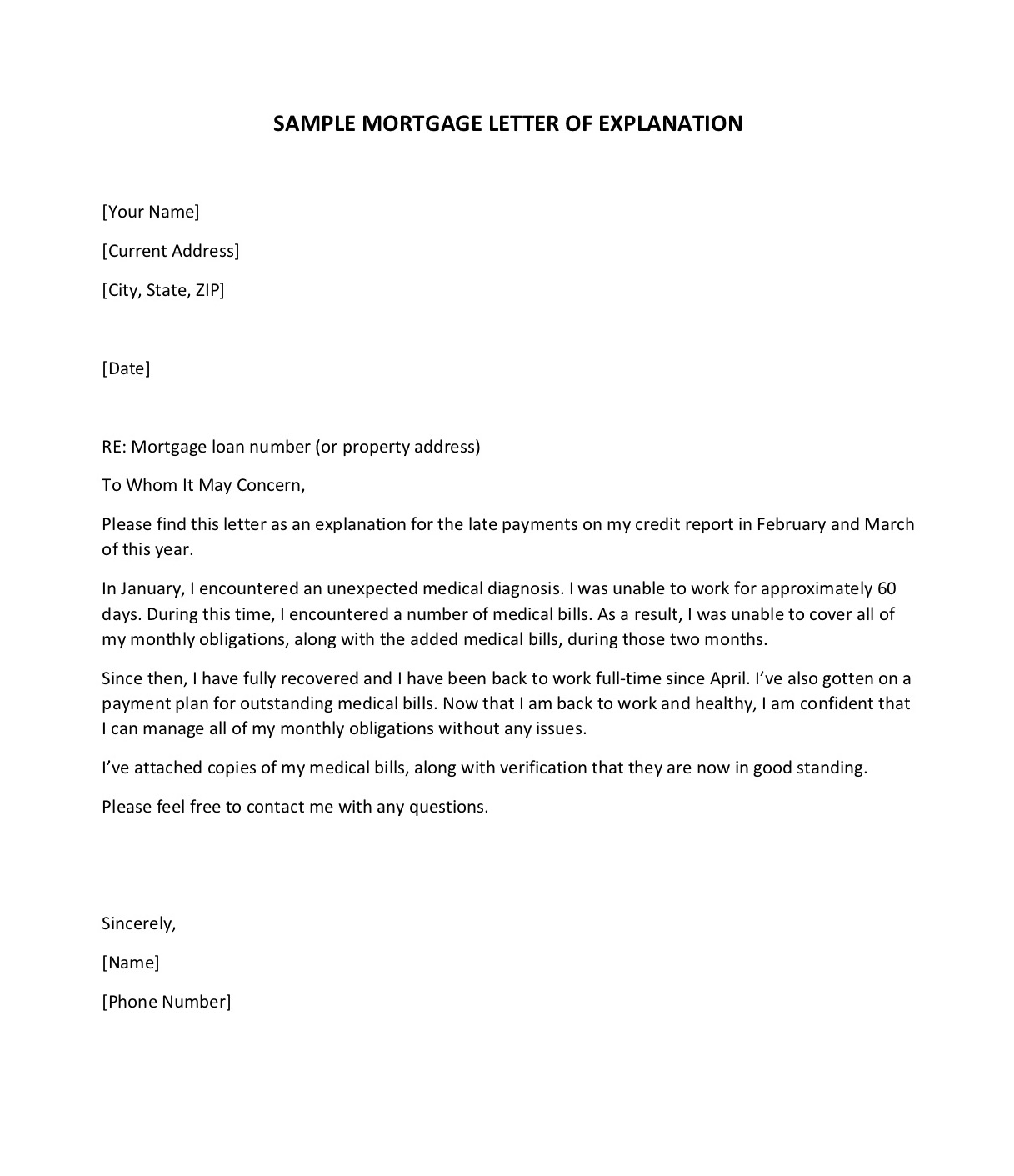

Sample letter of explanation and template

Remember to be honest, formal, and concise when writing a letter of explanation for your mortgage lender.

Start your mortgage application todayThe exact content will vary based on your situation, but here’s a general letter template you can use as a guide. (Click the image to open a PDF version.)

Remember to include your mailing address, phone number, and the number of your mortgage loan application (or the property address for which you’re applying).

Final advice on writing a letter of explanation

You’ll be asked to submit a pile of documentation during the mortgage loan process, including bank statements, tax returns, pay stubs, and more.

Start your mortgage application todayDepending on your financial situation, your lender may also request a letter of explanation. Many first-time home buyers think being asked to provide a letter of explanation means their mortgage application may be doomed.

Remember, this type of request is usually a good thing. The underwriter may be looking for this last item before signing off on your final approval.

When your lender requests a mortgage letter of explanation, remember this first: don’t panic.

Next, double-check with your lender on exactly what is being requested.

Then write a clear, concise letter that’s free of emotional language, negativity, or excessive detail. There’s a good chance that the next time you hear from your lender, it will be to let you know you’re fully approved.

Time to make a move? Let us find the right mortgage for you