Key Takeaways

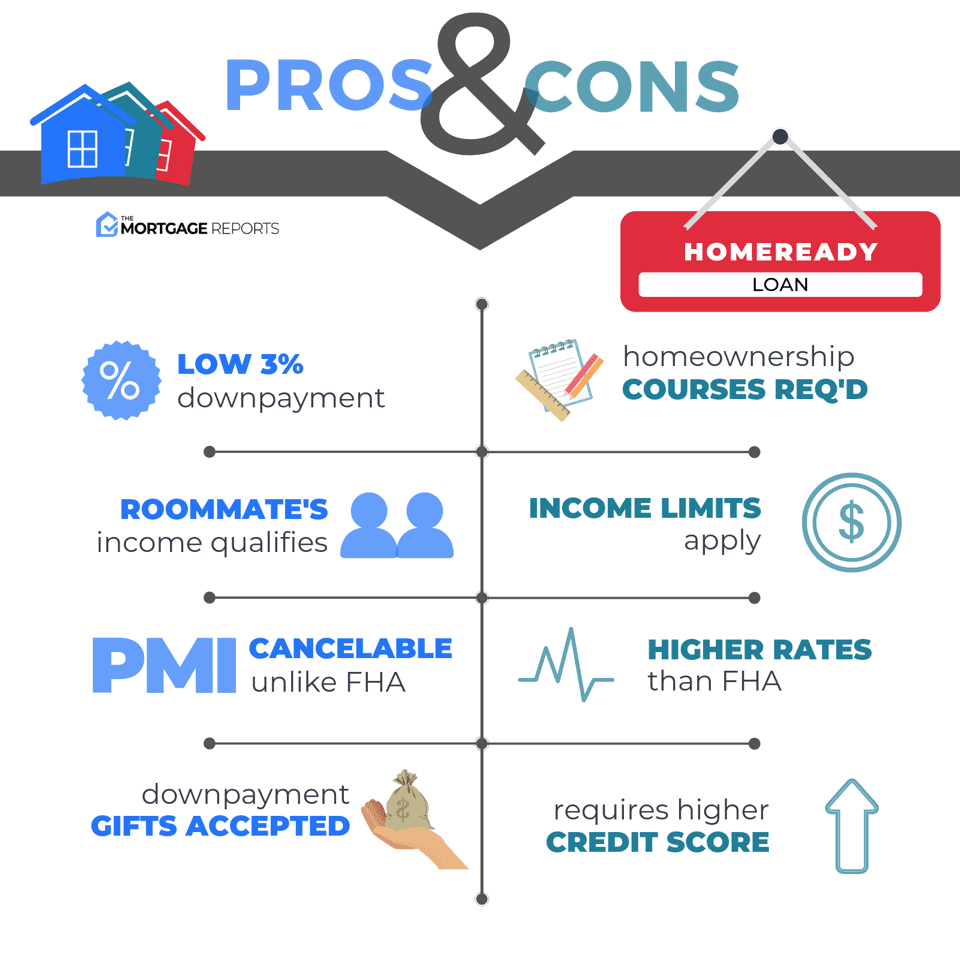

- HomeReady lets eligible buyers purchase a primary home with just 3% down, as long as their income is at or below 80% of the area median income (AMI).

- The program allows flexible income sources, including co-borrowers and boarder or rental income, which can help more buyers qualify.

- As a conventional loan, HomeReady offers competitive rates and the ability to cancel PMI once you reach 20% equity.

If you’re ready to buy a home but don’t have a lot saved for a down payment, the Fannie Mae HomeReady mortgage can be a great option.

You only need a 3% down payment, and you can use alternative funding sources like gifts or grants. Co-borrowers, regardless of residency, can also be included in your application, making it a flexible and accessible option for many buyers.

To qualify, your income must not exceed 80% of the area’s median income. For example, if your area has a median annual income of $50,000, you can make no more than $40,000 to meet the HomeReady income limits.

In this article (Skip to…)

- Income limits

- Overview

- Requirements

- Eligible properties

- Interest rates

- Down payment help

- Alternative loans

- FAQ

Want to see our expert mortgage insights first?

Add The Mortgage Reports as a preferred source on Google. You’ll automatically see our latest rate analyses, buying guides, and housing forecasts highlighted in your Google Search, AI Mode, and AI Overviews.

HomeReady income limits 2026

Fannie Mae sets the HomeReady income limits for borrowers nationwide. To qualify, you can’t make more than 80% of your area’s median income (AMI).

That means if your area has a median yearly income of $100,000, you must make $80,000 or less to qualify for the HomeReady program.

Verify your HomeReady eligibility. Start hereTo qualify for HomeReady income limits, you must not make more than 80% of your area’s median income (AMI).

You can determine whether or not you meet HomeReady income limits for 2026 by using Fannie Mae’s AMI Lookup Tool. Simply input your address, and the tool will detail your county’s area median income.

Additionally, lenders may use the Desktop Underwriter (DU) system to assess your eligibility, considering both your income and your property’s location.

For example, Salt Lake County, Utah, has an AMI of $115,400. To comply with HomeReady income limits, you can make up to $92,320 (80% of your AMI). But Fulton County, Georgia’s area median income, is $106,100. This means HomeReady income limits are $84,880 (80% AMI) for home buyers in the Atlanta area.

Since HomeReady is intended for lower-income borrowers, these AMI limits might not be a problem for most applicants. But what if you’re worried your income is too low to qualify? In that case, HomeReady’s income source flexibility can help immensely.

What is considered income by HomeReady?

Fannie Mae allows applicants to apply with one or more co-borrowers if their combined income falls within local HomeReady income limits.

You can also count income from a renter on your application, as long as they’ve lived with you for at least one year before buying the home.

- Wages and salaries

- Self-employment income

- Bonuses

- Commissions

- Pensions

- Annuities

- Social Security benefits

- Child support

- Alimony

- Rental income from a one-unit property with an accessory dwelling unit (ADU)

- Boarder income

Just note that non-borrower income is not counted directly toward your qualifying income. In addition, these policies can vary by lender, and consideration of non-borrower income may be rare.

Fannie Mae even allows lenders to consider the income of non-borrowing household members as a “compensating factor,” meaning it could help your chances if you have a higher DTI or lower credit score.

What is the HomeReady mortgage?

The HomeReady program aims to make it simpler for people with lower incomes to obtain low-down-payment mortgages at current market rates. Notably, the HomeReady loan allows for a down payment as low as 3%.

Check your HomeReady eligibility. Start hereHomeReady loan program benefits

The HomeReady program stands out for its flexibility in considering various income sources, making it an attractive option for homebuyers and homeowners looking to refinance. Whether you’re applying with a co-borrower or looking to include additional income, HomeReady offers unique features that can help you qualify for a mortgage or improve your current loan terms.

Check your HomeReady eligibility. Start hereKey benefits of the HomeReady program:

- Flexible co-borrower options: Allows non-occupant co-borrowers who can live either with you or elsewhere.

- Additional income consideration: Documented income from a renter or boarder can be included if it meets HomeReady loan limits.

- Increased qualification chances: These features can assist families who might otherwise face loan approval challenges.

- Refinancing opportunities: Available for both home purchases and mortgage refinancing.

- High loan-to-value (LTV) ratio: Offers refinancing with up to a 97% LTV, helping borrowers with lower equity.

- No need for 20% equity: Homeowners can secure lower interest rates and reduced monthly payments without waiting to build significant equity.

HomeReady loan requirements

To qualify for this loan program, you’ll have to fall within the HomeReady income limits, take a short online class about homeownership, and have decent credit. The exact requirements might vary by lender, but Fannie Mae sets the minimum requirements for all HomeReady loan applications.

Check your HomeReady eligibility. Start hereThe basic requirements for HomeReady include:

- You cannot earn more than 80% of your Census tract’s median income

- You need a FICO score of at least 620 in most cases

- The home must be your primary residence

- You should have a debt-to-income ratio (DTI) that’s no higher than 50%. This is more lenient than most other mortgage programs

- You must agree to complete a 4- to 6-hour online homeownership education course

Eligible homeownership education courses must be taken with a HUD-approved housing counseling agency prior to mortgage underwriting. Contact the Hope Hotline at 1-888-995-HOPE or visit its website for a list of approved classes.

“But if you put more than 10% down, this requirement can be waived,” says loan officer Jon Meyer.

If you meet these criteria, the HomeReady loan program may be just what you need to move from renting to homeownership.

What properties are eligible for HomeReady financing?

Borrowers have many options for buying real estate with a HomeReady loan.

Check your income eligibility. Start hereYou can purchase a traditional single-family home if you wish. But if you want something a little different, Fannie Mae also allows the purchase of:

- Condominium units

- Homes in a planned unit development (PUD)

- Co-ops

- Manufactured homes

- Multi-family homes with 2, 3, or 4 units

Borrowers who want a multi-unit home will need a higher credit score, possibly as high as 680.

No matter what type of home you buy with HomeReady, it needs to be your primary residence. That means if the building has 2-4 units, you must live in one of the units yourself full-time.

In other words, you can’t use this loan program to purchase investment properties or vacation homes. It serves low- and moderate-income buyers looking for a home to live in.

HomeReady mortgage interest rates

Interest rates for a HomeReady mortgage loan are the same as rates for a “traditional” conventional loan. There is no premium applied for using the HomeReady program.

Check your home buying options. Start hereIn fact, mortgage rates for the HomeReady loan might be even lower than for other low-down-payment mortgages, like the 3% down conventional 97 loan.

Because mortgage rates can vary by as much as 50 basis points (0.50%) between lenders, it pays to shop around. Don’t stop shopping after you get your first quote.

Fixed-rate mortgage options

Borrowers using the HomeReady mortgage program have access to a complete mix of fixed-rate mortgage products, including:

- 10-year fixed-rate mortgage

- 15-year fixed-rate mortgage

- 20-year fixed-rate mortgage

- 30-year fixed-rate mortgage

This range of options is a significant advantage over USDA loans, which offer only a 30-year mortgage.

Shorter-term loans often have lower interest rates than 30-year loans. Thanks to the low rate and short term, borrowers can save tens of thousands in mortgage interest over the life of the loan.

However, 10-, 15-, and 20-year loans generally have much higher monthly payments than 30-year mortgages. That’s because you have to pay off the same loan amount in less time. For this reason, most home buyers choose a 30-year fixed-rate mortgage.

Adjustable-rate mortgage options

Borrowers using the HomeReady mortgage program also have access to a range of adjustable-rate mortgage (ARM) products. These include the following:

- 5/1 ARM

- 7/1 ARM

- 10/1 ARM

Adjustable-rate loans have a fixed rate for the first 5, 7, or 10 years. After that, your interest rate and monthly payment could rise each year. This makes ARMs much riskier than fixed-rate loans.

Some leading lenders have opted out of HomeReady ARMs. So if you want an adjustable-rate loan, you may have to shop around for a lender offering one.

How can I get help with my HomeReady down payment?

HomeReady’s 3% down payment is about half the average down payment size. It’s a fraction of the 20% many renters think they’d need to save up.

Check your income eligibility. Start hereStill, coming up with 3% — which is $6,000 for a $200,000 home — can be challenging for first-time home buyers with limited income and/or savings.

HomeReady helps by allowing flexible sources for your down payment. You could use the following:

- Gift funds: Family members could help you come up with your down payment by gifting the money. Note that this must be a true gift and not a loan in disguise. Learn more about down payment gift requirements here

- Home buyer grants: Ask your loan officer or real estate agent about down payment assistance programs in your area. Many local governments and nonprofits offer DPAs in every state

- Down payment loans: Fannie Mae’s Community Seconds program can help you secure a second loan specifically to cover your down payment and closing costs. Down payment assistance might offer a low- or no-interest loan as well

Using a second mortgage, such as Community Seconds, will put a second lien on your home, which means you’d have to pay off both loans (your primary mortgage and your second mortgage) if you sell or refinance.

How to apply for a HomeReady loan

If you’re considering a HomeReady mortgage, knowing how to navigate the application process can help you make more informed decisions.

Beyond meeting the HomeReady income limits, it’s important for potential home buyers to understand that lenders will evaluate their eligibility based on several other main criteria of the loan program. These include factors such as credit score, debt-to-income ratio, employment history, and savings for down payment and closing costs.

Check your income eligibility. Start hereHere’s a step-by-step guide to applying for a HomeReady loan.

1. Compare loan features

Before diving in, take time to understand what sets a HomeReady loan apart from other mortgage options. Although it allows for low down payments, keep in mind that the interest rates may be higher compared to conventional loans. Compare this with other loan types to see if a smaller down payment outweighs the cost of potentially higher interest rates.

2. Check eligibility requirements

Next, familiarize yourself with the requirements that you must fulfill, such as falling under the HomeReady income limits and credit score minimums. HomeReady also requires applicants to meet its mandatory homeownership education requirements. If you’re confident you meet these criteria, move forward to the next step. If you’re uncertain, consider seeking advice from a mortgage advisor.

3. Compare mortgage lenders

While Fannie Mae originated the HomeReady program, it doesn’t underwrite the loans directly. You’ll need to look for a participating mortgage lender. These could be local banks, national financial institutions, or online lenders. It’s worth noting that some lenders may choose not to offer this type of loan.

4. Submit your loan application

Once you’ve chosen a lender, you’ll begin the actual application process. This usually entails filling out an application form and providing various documents, such as proof of income and tax returns. The timeframe for this stage can vary depending on whether you’re using physical copies or digital uploads. Some platforms offer real-time verification of financial data, which can speed up the process.

5. Await loan approval

After submitting your application, there will be a period of evaluation where the lender assesses your financial stability and creditworthiness. You’ll eventually receive information on whether you’ve been approved, along with the terms of your mortgage, like the interest rate and the loan amount. This will allow you to either start house hunting or make an offer if you’ve already found a property.

If you find that your application is unsuccessful, don’t be discouraged. There are numerous other mortgage options tailored to different financial situations. Consult with your mortgage advisor to discover other paths to homeownership.

Are there any alternatives to the HomeReady loan?

As you navigate the path to homeownership, it’s essential to explore all your mortgage options. This section will delve into two popular alternatives to the HomeReady mortgage: FHA loans and the Home Possible program, highlighting the main differences and advantages of each.

Check your income eligibility. Start hereHomeReady loans vs. FHA loans

Like HomeReady loans, FHA loans help people overcome the financial challenges of homeownership. If you qualify for HomeReady, you might also be eligible for FHA. But which mortgage program is better?

Renters with limited cash for a down payment have used FHA loans since 1934. FHA’s minimum down payment amount is 3.5%, slightly higher than HomeReady’s 3%. The down payments are similar, but these two loan programs have some big differences.

When is an FHA loan better than a HomeReady loan?

The FHA loan works best for borrowers with lower credit scores. With a FICO as low as 580, you could borrow with only 3.5% down. Borrowers with scores between 500 and 579 might still qualify, but they’d need at least a 10% down payment.

Backing from the Federal Housing Administration helps lenders extend favorable loan terms to borrowers with lower credit scores.

By contrast, HomeReady depends more on the borrower’s credit, and you’d typically need a score of at least 620 to qualify.

FHA loans work best for higher earners, too, since the FHA program, unlike HomeReady, doesn’t have income limits.

When is HomeReady better than an FHA loan?

HomeReady loans offer more flexibility when it’s time for income verification. For example, lower-income borrowers could apply with one or more co-borrowers.

You could even count supplemental income from a boarder’s rent if you plan to have a roommate or rent out a room in the house. You do not need to include the renter on your loan application. However, you must document that they’ve lived with you for at least one year prior to applying.

Plus, since HomeReady is a conventional loan, you can cancel private mortgage insurance (PMI) once you’ve paid the loan down to 80% of the home’s price. This would lower your monthly mortgage payments considerably.

By comparison, FHA’s mortgage insurance coverage lasts the life of the loan unless you put 10% or more down.

Remember, though, that you have to earn 80% or less than your area’s median income to qualify for HomeReady.

HomeReady vs. Home Possible

Freddie Mac’s Home Possible program works a lot like Fannie Mae’s HomeReady.

Like the HomeReady program, the Home Possible loan:

- Allows 3% down payment

- Has an income limit of 80% of the area median income

- Is co-borrower friendly

One of the main differences between these two programs is the minimum credit score. Many lenders require a credit score of at least 660 to qualify for a Home Possible loan. HomeReady, on the other hand, is typically available with a FICO score of 620 or higher.

Compare your low-down-payment mortgage options. Start here

HomeReady income limits FAQ

Verify your HomeReady eligibility. Start hereBottom line on HomeReady income limits

The final word on HomeReady income limits is that they ensure the program’s benefits are specifically directed towards low-income borrowers, making homeownership more attainable for those who need it most.

The HomeReady mortgage program helps more U.S. households get approved for low-down-payment loans. Qualified borrowers can buy with just 3% down.

The mortgage interest rate you receive depends on several factors, including your credit score, down payment, and adherence to HomeReady income limits, to name a few. Get quotes and compare pricing with at least three different lenders before deciding.

Ready to get started? Check your eligibility with a lender today.

Time to make a move? Let us find the right mortgage for you