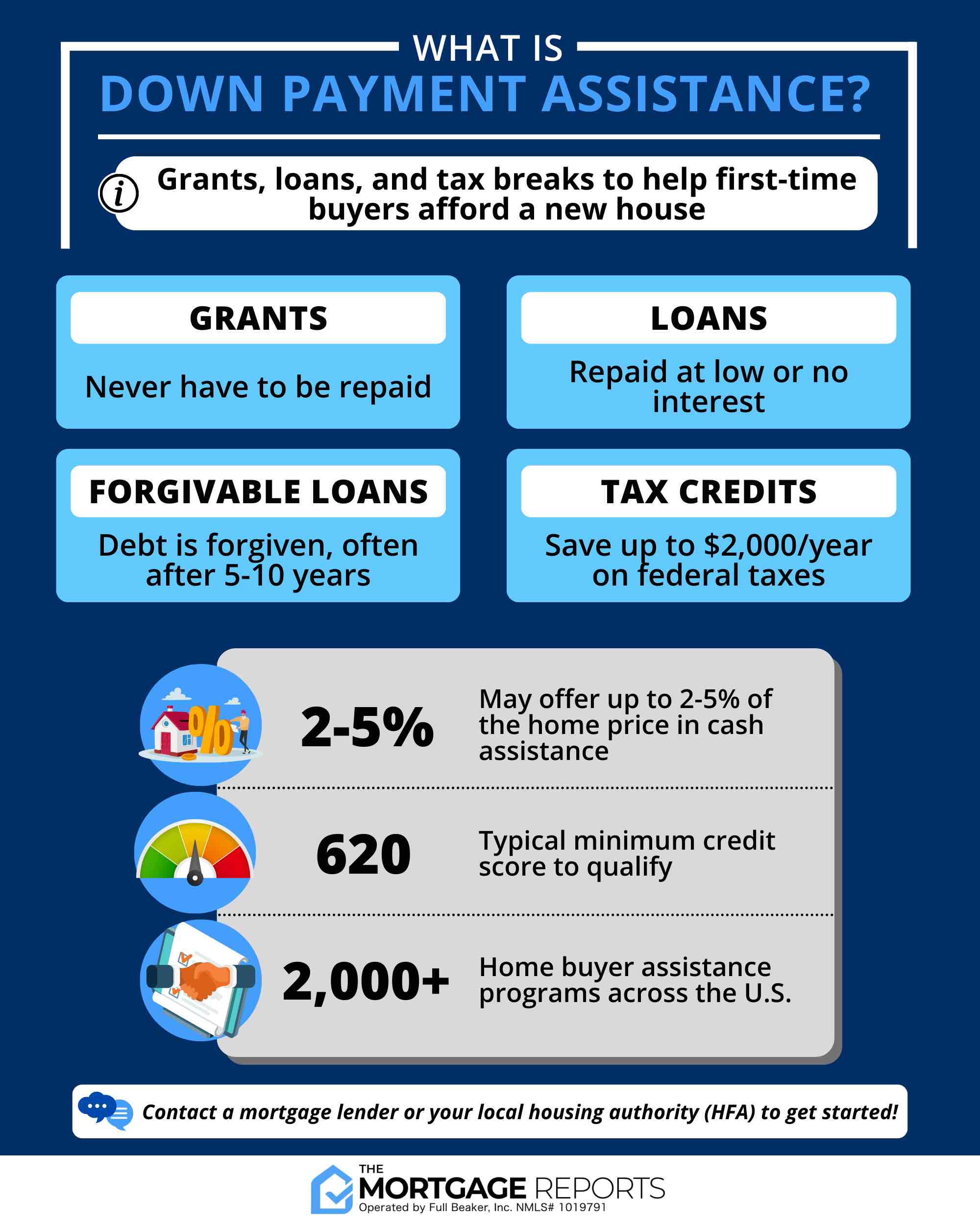

Key Takeaways

- DPA can cover part (or all) of your down payment and sometimes closing costs.

- Assistance comes as grants or loans—some are deferred or forgivable if you stay in the home long enough.

- Most programs require first-time (or 3-years-since-owning) status, income/price limits, and an approved lender/loan type.

Down payment assistance (DPA) programs offer financial help to cover part or all of a home buyer’s down payment and often closing costs.

These programs provide grants or low-interest loans, reducing the upfront cash needed to buy a home. Some DPAs offer forgivable loans or cash gifts that don’t need to be repaid, while others may require low or no-interest repayment.

With over 2,000 programs nationwide, many run by state, county, and city governments, DPAs can provide thousands of dollars to eligible buyers. Typical requirements include being a first-time home buyer, a decent credit score, and low to moderate income, though specific rules vary.

In this article (Skip to...)

>Related: How to buy a house with $0 down: First-time home buyer

Want to see our expert mortgage insights first?

Add The Mortgage Reports as a preferred source on Google. You’ll automatically see our latest rate analyses, buying guides, and housing forecasts highlighted in your Google Search, AI Mode, and AI Overviews.

Who qualifies for down payment assistance (DPA)?

Down payment assistance programs are typically designed for first-time home buyers. However, a repeat home buyer may still qualify as a “first-time buyer” if they haven’t owned a home in the past three years.

Verify your first-time home buyer eligibility. Start hereTypical requirements to qualify for down payment assistance:

- First-time home buyer

- Low- to moderate-income

- Buying a primary residence

- Buying within local purchase price limits

- Using an approved mortgage program

- Working with an approved mortgage lender

Keep in mind that every down payment assistance program has its own requirements. The exact criteria vary based where you live and which programs are available.

In addition, you could get more money and qualify easier if you’re buying in a so-called “target area.” Your lender can help determine if your property is eligible.

Types of down payment assistance (DPA) programs

There are four main types of down payment assistance:

- Grants: Gifted money that never has to be repaid

- Loans: Second mortgages that are paid monthly along with your primary mortgage

- Deferred loans: Second mortgages with deferred payments that only have to be paid when you move, sell, or refinance

- Forgivable loans: Second mortgages that are forgiven over a set number of years (often five, but sometimes up to 15 or 20). These only need to be repaid if you move, sell, or refinance too early

Some DPA loans are interest-free, some have lower rates than your first mortgage, and others may require the same or a higher rate. A quick count of the programs listed below suggests that all four types of DPA are widespread. While grants are the most common, the other types aren’t far behind.

If you want to do some research on your own, you can also Google “down payment assistance grants in [state, county, or city].” This will help you find current programs specific to your area that you might be able to apply for.

Down payment assistance (DPA) programs & grants by state

Depending on which source you reference, there are between 2,000 and 2,500 DPA programs in the U.S. These programs are typically managed by state and local governments, as well as nonprofit organizations. Below, we’ve listed some of the biggest programs in each state.

Verify your home buying eligibility. Start hereThe U.S. Department of Housing and Urban Development (HUD) also lists many homeownership assistance programs, including DPA, on its state pages.1

While we have made reasonable efforts to make sure the information below is correct at the time of posting, it is subject to change without notice. Please check the relevant websites for more information.

Alabama down payment assistance

The Alabama Housing Finance Authority (AHFA) provides various programs and initiatives to make homeownership more accessible and affordable for Alabama residents. They provide financial assistance in the form of a DPA and closing cost grant, which can help alleviate the upfront costs associated with purchasing a home.

AHFA Step Up DPA

The AHFA will lend you up to 4% of the purchase price, with a $10,000 maximum, for a down payment on a new or existing home in Alabama. This assistance comes in the form of a 10-year second mortgage, provided that you meet the following conditions:

- Your household income can’t exceed $159,200

- You need a credit score of 640 or higher (680 or higher if you make more than 80% of your area’s median income)

- Debt-to-income ratio of 45% or lower.

- Your new first mortgage must be a HFA Advantage conventional loan, FHA loan, or VA loan from a participating lender.

- You must complete a homeownership education course

AHFA Affordable Income Subsidy Grant

In addition to the Step Up program’s down payment assistance, borrowers who opt for financing through the HFA Advantage loan are eligible for a grant to help with closing costs.

- If a borrower’s income does not exceed 50% of the AMI limits, they can qualify for a grant equal to 1% of their loan amount.

- If a borrower’s income is at or below 80% of the AMI limits, they are entitled to receive a grant worth 0.5% of their loan amount.

To qualify for this closing cost grant program, you’ll need to meet household income limits as well as AHFA’s standard guidelines for credit score, debt-to-income ratio, and more.

AHFA Mortgage Credit Certificate

Mortgage Credit Certificates (MCCs) offer a way to reduce federal tax liability by applying a tax credit based on a portion of the mortgage interest paid each year. This credit directly lowers the amount of federal tax due. You can still deduct any interest not covered by the MCC as mortgage interest on your federal tax return.

You can combine this MCC with the AHFA’s Step Up program or any 30-year fixed-rate mortgage that is fully amortized and is offered through a participating lender.

The rate of the mortgage credit varies depending on the size of the loan:

- For loans exceeding $150,000, a 20% MCC is provided without a maximum annual credit limit.

- For loans between $100,001 and $150,000, a 30% MCC is available, with the annual credit capped at $2,000.

- For loans of $100,000 or under, a 50% MCC is offered, also with an annual credit limit of $2,000.

Get more details on the AHFA website. And take a look at HUD’s list1 of alternative programs for Alabama.

Check your home buying eligibility in Alabama. Start hereAlaska down payment assistance

The Alaska Housing Finance Corporation (AHFC) can provide both down payment assistance and closing cost assistance to eligible Alaskan home buyers.

Affordable Housing Enhanced Loan program (AHELP)

AHELP provides qualified borrowers with down payment assistance that may come in the form of a grant, a second mortgage with deferred payments, a forgivable loan, or a combination of these options. The funds come through Alaska Housing’s network of local and federal government agencies, nonprofit agencies, or regional housing authorities

To be eligible, borrowers must meet the participating provider’s requirements.

- Borrowers may not own other residential real estate in the same general area

- Eligible properties are limited to owner-occupied single-family homes, condominiums, and manufactured homes

- An authorized home inspector must examine any homes that are 10 years old or older

- You must complete an approved home buyer education class

However, the website doesn’t provide much information about how much help is available. So your best bet is to speak with one of the many participating providers. You’ll find a list on the program’s website.

Closing Cost Assistance program

Alaska Housing can also offer a grant toward your closing costs and down payment. This grant is equal to either 3% or 4% of the loan amount, depending on your credit qualifications.

- You must have a score of 640 or above to be eligible

- You can get up to 4% of the purchase price of the home you’re buying. However, you may get only 3% if your credit score is particularly low

- You must be buying (not refinancing) a single-family home that you’ll occupy as your primary residence

- You must finance your home purchase with a 30-year fixed-rate mortgage. Eligible mortgage types include FHA loans, VA loans, and USDA loans.

As of now, the program’s status is a bit of a puzzle. Some information on the website suggests it’s not running at the moment, but other details seem to say otherwise.

To add to the confusion, there’s no word on whether any hiatus is temporary or here to stay. If you’re scratching your head like we are, the surefire way to get clarity is to give Alaska Housing a call. They’re just a toll-free dial away at 888-854-3884.

Regardless, you can learn more by visiting the AHFC webpage. And take a look at HUD’s list1 of alternative programs for Alaska.

Check your home buying eligibility in Alaska. Start hereArizona down payment assistance

Home buyers in Arizona have the option of choosing between two down payment assistance programs, depending on the location of the property they wish to purchase.

Home Plus Arizona

The Arizona Industrial Development Authority (Arizona IDA) offers the Home Plus program, which provides up to 4% of the initial balance on your new mortgage. The amount you might get will depend on the type of mortgage you choose.

- Funds can be applied to both down payment and closing costs

- You’ll need a minimum credit score of 640 to qualify for the program

- To be eligible, your annual income must not exceed $136,609

- You’ll also need to complete a homebuyer education course prior to the loan closing

Home Plus is a 3-year deferred second mortgage. That means there is no interest and no monthly payments, provided you do not sell or refinance the property within the first 36 months of homeownership. Find out more at the Home Plus homepage.

Pathway To Purchase DPA

The Pathway To Purchase program by the Arizona Department of Housing provides a grant of up to 10% of your loan amount, with a maximum of $20,000, to be used for your down payment or closing costs. Buyers must reside in one of the 17 designated cities in Arizona to be eligible for this opportunity.

While you don’t need to be a first-time homebuyer, there are several requirements to meet:

- Maximum purchase price for a home is set at $371,936

- The first mortgage loan must be 95% or less of the home’s value

- A minimum FICO score of 640 is required.

- Applicants must have a debt-to-income ratio of 45% or less

- The mortgage must be a 30-year fixed-rate for the purchase of existing homes, condos, or townhouses; new constructions or spec homes are excluded

- Completion of a homebuyer education course and a home inspection are mandatory

- Participants cannot own another property at the time of purchase

Learn more on the program’s website. And take a look at HUD’s list1 of alternative programs for Arizona.

Check your home buying eligibility in Arizona. Start hereArkansas down payment assistance

The Arkansas Development Finance Authority (ADFA) has a couple of helpful DPA programs associated with its Move-UP home loan.

Those taking advantage of the Move-Up first mortgage might also qualify for additional down payment assistance through any one of these ADFA programs:

- Arkansas Dream Down Payment Initiative (ADDI): Low-income borrowers may be eligible to receive up to 10% of the home purchase price, with a maximum limit of $10,000, for down payment and closing cost assistance. This is a forgivable second mortgage with no monthly payment that’s forgiven over five years.

- ADFA Down Payment Assistance Program (DPA): Qualifying moderate-income borrowers can receive up to $15,000 to use for their down payment and closing costs. This 10-year loan works as a second mortgage, which you pay alongside your mortgage payment.

- ADFA mortgage credit certificate (MCC): A dollar-for-dollar tax credit worth up to $2,000 per year.

Visit the ADFA homepage to discover more, including income limits for your county. And take a look at HUD’s list1 of alternative programs for Arkansas.

Check your home buying eligibility in Arkansas. Start hereCalifornia down payment assistance

The California Housing Finance Agency’s (CalHFA) MyHome Assistance Program provides eligible Californias with up to 3.5% of their home purchase price to go towards a down payment. Assistance comes in the form of what the agency calls a “silent second.” This is essentially a deferred loan that requires no repayment until the home is sold, or the loan is refinanced or paid in full.

- Homes financed with CalHFA loans receive a 3%.

- Homes financed with FHA loans receive a 3.5%.

This is a first-time home buyer’s down payment assistance program. So it won’t help if you already own an existing home.

However, CalHFA defines a first-time home buyer as “someone who has not owned and occupied their own home in the last three years.” So many who’ve previously owned homes may qualify.

Check out the MyHome Assistance Program webpage for more information. You’ll find some income limits there. If you’re a teacher or fire department employee, certain program limits may not apply.

Also, take a look at HUD’s list1 of alternative programs for California.

Check your home buying eligibility in California. Start hereColorado down payment assistance

For qualified Coloradans, the Colorado Housing and Finance Authority (CHFA) and the Colorado Housing Assistance Corporation (CHAC) both offer down payment assistance grants and second mortgages.

CHAC Down Payment Assistance

Colorado Housing Assistance Corporation is a nonprofit organization that offers down payment assistance and affordable loan programs to low- to moderate-income home buyers in Colorado.

CHAC’s assistance is intended for first-time buyers. To qualify, you’ll need to have a low or moderate income compared to others in the area in which you live.

- All borrowers must contribute a minimum of 1% of the home’s sale price to the transaction, and those funds cannot be a gift. If you’re part of the state’s disability program, that requirement is reduced to $750.

- This down payment assistance comes in the form of a second mortgage loan that must be repaid via monthly payments.

- Borrowers must also take a homebuyer education course

For more, visit CHAC’s website. And consult HUD’s list1 of alternative programs for Colorado.

CHFA Down Payment Assistance

The Colorado Housing and Finance Authority provides valuable assistance to first-time home buyers in the form of down payment assistance grants and second mortgage loans. These programs make it easier for Colorado households with moderate and low incomes to buy a home.

Home buyers who use CHFA first mortgage loan programs to finance their home purchase may qualify for additional assistance with their down payment and closing costs. You are still allowed to use one of the following options, even if you contribute to your down payment:

- CHFA Down Payment Assistance Grant: Qualified borrowers can receive up to 3% of their first mortgage (loan amount capped at $25,000). You receive help in the form of a grant, so you do not have to repay those funds.

- CHFA Second Mortgage Loan: This program offers a forgivable loan of up to 4% ($25,000 maximum) of your first mortgage rather than an outright grant. You only need to repay the loan balance if specific events occur, such as when your first mortgage is paid off, when you sell or refinance your house, or when you stop using the home as your primary residence.

To qualify for either program, you must meet the standard requirements, such as meeting the minimum credit score and household income limits and completing a homebuyer education course. Visit the CHFA website for next steps or more information.

Check your home buying eligibility in Colorado. Start hereConnecticut down payment assistance

The Connecticut Housing Finance Authority is usually the first stop for first-time home buyers looking for down payment assistance. The organization provides a number of programs and services to help low- and moderate-income families purchase their first home.

These programs include down payment assistance, closing cost assistance, and affordable mortgage options. Furthermore, the Connecticut Housing Finance Authority provides education and counseling to help homebuyers navigate the complex process of purchasing a home.

CHFA Down Payment Assistance Program (DAP)

The Connecticut Housing Finance Authority (CHFA) offers up to $15,000 in down payment assistance (DPA) in the form of a second mortgage.

- The minimum DPA loan amount is $3,000.

- You can normally borrow between 3% and 3.5% of the purchase price of the home—no more than the minimum required down payment.

- Borrowers are required to attend a free home buyer education course.

To apply for this program, you need to first obtain mortgage approval from a participating lender. You’ll find a list of approved lenders on the CHFA homepage. And check out HUD’s list1 for other programs in Connecticut.

Check your home buying eligibility in Connecticut. Start hereDelaware down payment assistance

The Delaware State Housing Authority (DSHA) offers a number of resources to make home buying easier, including down payment assistance that’s linked to its “Welcome Home” first-time homeowner program.

The amount of assistance you are eligible for will depend on the type of Welcome Home program you finance your home purchase with. Here’s what you can expect:

- Home Sweet Home: Borrowers can receive up to $12,000 to help cover their down payment and closing costs through a forgivable loan with a term of 10 years. For each year the borrower lives in the home as their primary residence, 10% of the loan’s balance will be forgiven.

- Delaware Diamonds: Essential workers, including educators, healthcare professionals, first responders, state employees, active military members, and veterans, may qualify for up to $10,000 in assistance for their down payment and closing costs. This assistance is provided as a forgivable loan over a 10-year period.

- First State Home Loan. Borrowers can access a second mortgage of up to 3% of the final loan amount to cover down payment and closing costs. You must repay the money when selling the home, refinancing it, or no longer using it as your primary residence.

- Delaware First-Time Homebuyer Tax Credit. First-time home buyers qualify for a federal tax credit that can cover up to 35% of their annual mortgage interest, with a maximum benefit of $2,000 per year. To be eligible, you must use one of DSHA’s homeownership programs.

Find details on the DSHA’s website. And find other DPA programs for Delaware on HUD’s website.1

Check your home buying eligibility in Delaware. Start hereWashington, D.C. down payment assistance

If you’re looking to buy a home in Washington, D.C., you’ll find substantial down payment assistance through two key sources: the DC Housing Finance Agency (DCHFA) and the Department of Housing and Community Development (DHCD).

These organizations provide down payment and closing cost assistance, competitive mortgage financing options, and resources through programs like DC Open Doors and the Home Purchase Assistance Program (HPAP) to make homeownership more feasible for individuals and families in the District of Columbia.

DC Open Doors Down Payment Assistance Loan (DPAL)

You can get a no-interest loan for as much as you need for your down payment through the DCHFA’s DC Open Doors program.

The DAPL is structured so that borrowers are not required to make monthly payments. The repayment of the loan, which is interest-free, is due in full under specific conditions: when 30 years have passed since the loan’s closing date, if the property is sold or transferred, if the property is no longer the borrower’s primary residence, or if the borrower refinances their first mortgage.

DCHFA Mortgage Credit Certificate

Additionally, if you meet the requirements, you may be eligible for a DCHFA Mortgage Credit Certificate (MCC), which entitles you to a federal tax credit equal to 20% of the mortgage interest you pay each year.

Visit the DCHFA website for more details on both of these programs.

DHCD Home Purchase Assistance Program (HPAP)

The DHCD offers first-time home buyers with low to moderate incomes assistance with their down payment and closing costs through its Home Purchase Assistance Program, also known as HPAP.

HPAP offers zero-interest, deferred-payment loans that are repaid when the property is sold or refinanced.

- Low-income applicants earning less than 80% of the area median income can receive up to $4,000 as an interest-free loan with no monthly payments, due upon resale or refinancing of the home.

- Moderate-income applicants earning 80% to 110% of the area median income are eligible for a $4,000 interest-free loan, repayable after five years.

Read more at the HPAP homepage.

DHCD Employer-Assisted Housing Program (EAHP)

The Employer-Assisted Housing Program (EAHP) supports eligible District government employees with purchasing their first single-family home, condo, or co-op in the District. It provides a deferred, 0% interest loan alongside a matching funds grant, which can be used for down payment and closing costs.

For all District government employees:

- The maximum loan amount has been raised to $20,000.

- The matching funds grant has been increased to up to $5,000.

For first responders and educators:

- A recoverable grant of up to $10,000 is available for down payment assistance, contingent upon a five-year service obligation.

- The property must remain the participant’s principal residence for five years, fulfilling a five-year service agreement signed upon purchase.

- Failure to meet these conditions turns the $10,000 grant into a deferred, zero-interest loan.

- Eligible for a matching funds grant of up to $15,000.

Since the loan is a deferred second mortgage, no repayment is required until you sell, refinance, or no longer occupy the property as your primary residence. You can find more details on the EAHP website. And see other possible DPA programs on HUD’s website.1

Check your home buying eligibility in Washington, D.C. Start hereFlorida down payment assistance

The Florida Housing Finance Corporation (FHFC) is a key resource and a buyer’s first stop in Florida. With programs such as down payment assistance, low-interest loans, and homebuyer education, FHFC plays an important role in assisting Florida first-time home buyers.

Florida Assist

The Florida Assist is a deferred second mortgage with a 0% interest rate of up to $10,000 that can be used for a down payment, closing costs, or both. The loan has no monthly payments and is repaid only when you sell, refinance, or pay off your first mortgage.

Florida Homeownership Loan Program (FL HLP)

The Florida Homeownership Loan Program (FL HLP) is designed to provide eligible first-time home buyers with up to $10,000 to use towards their down payment and closing costs. This is a second mortgage with a 15-year amortizing loan at 3%.

3%, 4%, and 5% HFA Preferred Program

The HFA Preferred Program provides assistance in the form of a forgivable second mortgage that’s either 3%, 4%, or 5% of the first mortgage. Your income and the location of the home will determine how much of a loan you are eligible for. Additionally, there is a 20% annual forgiveness of the loan for the entire five-year term.

HFA Advantage PLUS Second Mortgage

The HFA Advantage PLUS Second Mortgage is nearly identical to its sister program, with the main difference being that it offers a 0% deferred second mortgage of up to $8,000 that is forgiven at a rate of 20% per year for five years. This is a great option for first-time home buyers who are using one of Florida Housing’s conventional loans.

Florida Hometown Heroes Housing Program

The Florida Hometown Heroes Housing Program aims to assist individuals who offer valuable services to their communities, including teachers, healthcare workers, law enforcement officers, firefighters, and veterans. Qualifying borrowers can receive up to 5% of the first mortgage loan amount, or a maximum of $35,000. This helps with the down payment and closing costs.

That’s a 30-year, no-interest loan that the buyer repays when they sell, refinance, or pay off their first mortgage.

Discover more at the FHFC’s website. And check HUD’s list of alternative programs1 for Florida.

Check your home buying eligibility in Florida. Start hereGeorgia down payment assistance

The Georgia Dream Homeownership Program (GDHP) offers various down payment loan options to assist Georgia first-time home buyers or those who haven’t owned a home in the past three years.

To be eligible for any of these DPAs, borrowers must meet local household income limits and have liquid assets of no more than $20,000 or 20% of the home purchase price (whichever is greater).

Standard loan option

All eligible homebuyers can receive up to $10,000 through the Standard Loan option to use towards their down payment or closing costs. This creates opportunities for individuals and families who would otherwise struggle with these upfront costs.

Protectors, Educators, and Nurses (PEN) program

The PEN program goes a step further by offering up to 6% of the home purchase price, or a maximum of $12,500, to individuals who work in public service roles such as public protectors, educators, healthcare providers, and active military personnel.

Choice

Similarly, offering $12,500, the CHOICE program is specifically created for families that have a family member with a disability. Recognizing the financial strain that disability care can put on families, it offers generous assistance to help them purchase a home.

You can get all the details from the GDHP website. And check out HUD’s list1 of other DPA programs in Georgia.

Check your home buying eligibility in Georgia. Start hereHawaii down payment assistance

There isn’t an official statewide down payment assistance program for Hawaii. But help is still available for Hawaii’s first-time home buyers.

The Hawaii Home Ownership Center is a non-profit mortgage brokerage offering both down payment assistance and a 15-year deferred closing cost loan.

DPAL Program

The DPAL program offers a second mortgage specifically designed for first-time buyers. It requires a minimal down payment of 3% for individuals with incomes up to 120% of the area median income (AMI).

- You need to make a down payment of at least 3%.

- You will be charged a mortgage interest rate of 4.5% or the rate of the first mortgage, whichever is lower, and you are not required to have mortgage insurance.

- Excludes pre-payment fees

- The loan limit is $125,000

- You must secure the initial mortgage through HHOC Mortgage.

- You must enroll in first-time homebuyer education classes and attend a coaching session through the Hawaii HomeOwnership Center.

Deferred Closing Cost Assistance Loan

This plan offers a deferred loan for 15 years with no interest and no monthly repayments to help with closing costs; it also provides options for interest rate reduction.

- First-time homebuyers with low to moderate income (120% AMI or below) qualify.

- You must participate in first-time homebuyer education and attend a coaching session through the Hawaii HomeOwnership Center.

- You can receive a loan of up to $15,000 with a matching ratio of 6:1.

- HHOC Mortgage needs to originate the primary mortgage.

- The borrower must use the home as their primary residence and submit an occupancy affidavit to verify this annually.

- Applicants across the state can access this assistance.

Take a look at HUD’s list1 of other homeownership assistance programs in Hawaii.

Check your home buying eligibility in Hawaii. Start hereIdaho down payment assistance

The Idaho Housing and Finance Association (IHFA) operates two programs that help with down payments and closing costs through forgivable second mortgages. Both programs require borrowers to take a homebuyer education course to qualify.

Idaho Housing Second Mortgage

The first option is a second mortgage with a fixed interest rate of up to 7% of the home’s purchase price, which will cover the majority of your down payment and closing costs. You will pay back this loan over 15 years with a fixed monthly payment and a 2% interest rate.

To receive this assistance, you need to be a first-time home buyer. You must contribute at least 0.5% of the sale price from your own funds, and your income cannot exceed $150,000.

Idaho Housing Forgivable Loan

The alternative option is a forgivable loan. This loan offers a 0% interest rate and requires no monthly repayments, but it caps the loan amount at 3% of the property’s purchase price.

Each year, 10% of the loan is waived, meaning that by the end of the tenth year, no debt remains. If you decide to relocate, sell, or refinance within the ten-year period, you must immediately repay any remaining loan balance.

There are costs associated with the forgivable loan. The website states that using each 0.5% of forgivable loan will increase the interest rate of the first mortgage by 0.125%.

Visit the IHFA website for complete details, which include income limits in some cases. And check HUD’s list1 of alternative programs for Idaho.

Check your home buying eligibility in Idaho. Start hereIllinois down payment assistance

The Illinois Housing Development Authority (IHDA) has multiple down payment assistance loan options. To get any of these loans, you’ll have to put up $1,000 or 1% of the purchase price (whichever is greater) yourself. And you must be buying an existing home; new builds are excluded.

IHD Access Forgivable

The IHD Access Forgivable program offers a forgivable loan to assist with the down payment and closing costs. This program offers a forgivable loan equivalent to 4% of the purchase price, with a maximum cap of $6,000. Parts of this loan are forgiven over time, which means that if you stay in the home for a set period of time (usually 10 years), you will not have to repay the loan.

IHD Access Deferred

The IHD Access Deferred program offers an interest-free loan for down payment and closing cost assistance, up to 5% of the purchase price (with a cap at $7,500). This loan is deferred, and no payments are required until you sell, refinance, or pay off your first mortgage. This program offers the advantage of enabling you to become a homeowner with minimal upfront costs. You can repay the loan at a later stage when your financial situation might be more comfortable.

IHD Access Repayable

The IHD Access Repayable program provides a loan for up to 10% of the purchase price (with a maximum cap of $10,000) to help with your down payment and closing costs. Unlike the Access Forgivable and Access Deferred programs, this loan requires repayment, but it does offer a higher assistance limit. Home buyers with the financial capacity to handle regular payments but needing help with the upfront costs of purchasing a home will find this program particularly beneficial.

Learn more at the Illinois Housing Development Authority’s website. And consult HUD’s list1 of alternative programs in Illinois.

Check your home buying eligibility in Illinois. Start hereIndiana down payment assistance

The Indiana Housing and Community Development Authority (IHCDA) has two programs that offer down payment assistance.

- First Place (FP) Program: Offers up to 6% of the purchase price for first-time home buyers. This DPA must be used with either an FHA or conventional loan and requires a credit score of 640 or higher, depending on debt-to-income ratio (DTI)

- Next Home (NH) Program: First-time home buyers can get up to 3.5% of the home’s purchase price. It must be used with either an FHA or conventional loan and requires a credit score of 640 or higher, depending on debt-to-income ratio (DTI). This program can also be combined with IHCDA’s Mortgage Credit Certificate

The IHCDA also offers a mortgage credit certificate that can help first-time home buyers and veterans qualify for a better mortgage loan.

For more information on these, visit the IHCDA’s website. And check HUD’s list1 of other programs in Indiana.

Check your home buying eligibility in Indiana. Start hereIowa down payment assistance

You can find grants and loans for down payment or closing cost assistance through the Iowa Finance Authority. Assistance is available for both first-time home buyers and veterans. If someone is purchasing a home in a low-income census tract, they may also be eligible. The Iowa Finance Authority operates a similar program for repeat home buyers.

All programs have income limits and price caps on eligible homes. To qualify, you need a credit score of 640.

First Home DPA Loan

The First Home Down Payment Assistance (DPA) Loan program is designed to assist eligible first-time home buyers with their down payment and closing costs. The program offers a no-interest loan of up to $5,000. This deferred loan requires no monthly payments, but it will have to be repaid if the home is sold, refinanced, or the first mortgage is paid in full.

First Home DPA Grant

Eligible first-time home buyers can receive a grant of up to $2,500 through the First Home DPA Grant to cover the down payment and closing costs. Since it’s a grant and not a loan, you don’t have to repay it.

Homes for Iowans DPA Loan

The Homes for Iowans program provides a no-interest loan of up to 5% of the home purchase price to be used for a down payment and closing costs. Like the First Home DPA Loan, no repayments are required until the home is sold, refinanced, or the first mortgage is paid in full.

IFA Military Homeownership Assistance

The IFA has designed the Military Homeownership Assistance program as a special initiative to honor and support military personnel and veterans. Eligible service members and veterans purchasing a home in Iowa can receive a $5,000 grant for the down payment and closing costs through this program.

Learn more at the IFA’s website. And take a look at HUD’s list1 of alternative programs in Iowa.

Check your home buying eligibility in Iowa. Start hereKansas down payment assistance

Kansas first-time homebuyers are fortunate to have access to not one, but three statewide down payment assistance programs, making sure a variety of options to suit different needs.

Kansas Housing First-Time Homebuyer Program

The Kansas Housing Resources Corporation (KHRC) offers special mortgage loans as well as several down payment assistance options for buyers in the Sunflower State. Buyers can borrow 15% or 20% of the cost of the home as a silent second mortgage, without needing to make any monthly payments.

- The loan is forgiven after 10 years, provided the borrower remains in residence and hasn’t sold, transferred, or refinanced their mortgage by the end of that period

- If you move, sell, transfer ownership, or refinance within those 10 years, you still owe the portion of the loan that has not been forgiven.

- Eligibility requirements include meeting income limits (annual income can’t exceed 80% of the area median income) and contributing at least 1% of the home’s purchase price from your own pocket.

Due to preexisting DPA programs, this one isn’t available in Topeka, Lawrence, Wichita, Kansas City, or Johnson County. Get more details at the KHRC website.

Kansas DPA

Although the Kansas DPA is not affiliated with KHRC, this statewide assistance program can help with closing costs or a down payment. Furthermore, it may also offer you a 30-year mortgage loan with a fixed interest rate.

- Eligibility requirements include meeting income limits and having a credit score of at least 640

- Buyers also need to use an approved lender

The website doesn’t provide much detail about the amount of assistance you can receive. So it’s best to reach out to one of the many participating lenders or speak directly to the Kansas DPA. You’ll find contact details on the program website.

FHLBank Topeka Homeownership Set-Aside Program (HSP)

For homes that need work, this program can help with home improvements and repairs in addition to down payment and closing costs.

- Qualified applicants can receive a grant of up to $7,500, which is entirely forgiven after five years.

- If the buyer sells their home or refinances before that, they must repay the grant.

- To apply, your household income cannot exceed 80% of the area median income, and you must be an FHLBank member.

There’s not much more information online. So if you’re interested in learning more, register for the HSP program through its website for more details. And find alternative programs for Kansas on HUD’s website.1

Check your home buying eligibility in Kansas. Start hereKentucky down payment assistance

The Kentucky Housing Corporation (KHC) offers a special loan program to help future home buyers with down payments, closing costs, and prepaid expenses.

KHC Regular DAP

You can get the Regular DAP for homes priced up to $510,939. The program provides a loan of up to $10,000, which must be repaid over a 10-year term at an interest rate of 3.75%.

Additionally, there is no liquid asset review, and there’s no limit on borrower reserves.

This program is open to all KHC first-mortgage loan recipients, but you must use a KHC-approved lender. Check the KHC’s website for more details.

Check your home buying eligibility in Kentucky. Start hereMeanwhile, consult HUD’s list1 of alternative homeownership assistance programs in Kentucky.

Louisiana down payment assistance

Louisiana’s Resilience Soft Second Loan is among the most generous down payment assistance programs in the U.S. Eligible Louisiana residents may qualify for:

- A “soft loan” of 20% of the home purchase price, up to $55,000

- Up to $5,000 in closing cost assistance for a total of up to $60,000

Better yet, the loan is forgiven after ten years. So as long as you remain in your home for at least that long, you won’t have to repay anything.

To qualify for this program, you must meet the income requirements set by the Louisiana Housing Corporation. You can’t earn more than 80% of your area’s median income.

And only first-time homebuyers can participate. First-time buyers in Louisiana include single parents who owned a home while married.

Only homes in the following parishes qualify: Acadia, Allen, Ascension, Avoyelles, Beauregard, Bienville, Bossier, Caddo, Calcasieu, Caldwell, Catahoula, Claiborne, De Soto, East Carroll, East Baton Rouge, East Feliciana, Evangeline, Franklin, Grant, Iberia, Iberville, Jackson, Jefferson Davis, Lafayette, LaSalle, Lincoln, Livingston, Madison, Morehouse, Natchitoches, Ouachita, Pointe Coupee, Rapides, Red River, Richland, Sabine, St. Helena, St. James, St. Landry, St. Martin, St. Tammany, Tangipahoa, Union, Vermilion, Vernon, Washington, Webster, West Baton Rouge, West Carroll, West Feliciana, and Winn Parish.

For more information on this program, visit LHC’s website. And look at HUD’s list1 of alternative homeownership assistance programs in Louisiana.

Check your home buying eligibility in Louisiana. Start hereMaine down payment assistance

MaineHousing’s First Home Loan Program makes buying a home easier and more affordable by offering low fixed-interest mortgages. And if you require assistance with the cash for closing costs, MainHousing offers two programs that may suit your needs.

MaineHousing Advantage Down Payment Program:

Extra help is available for people who get a mortgage through one of the MaineHousing loan programs.

- Borrowers may be eligible for up to $5,000 in cash to use towards their down payment, closing costs, and any prepaid escrow expenses

- The assistance comes as a grant, not a second mortgage. However, borrowers might need to repay the funds if the home is sold or refinanced

- Borrowers must contribute at least 1% of the loan amount to the home purchase, but this contribution can come from gift funds

- Homebuyers are required to complete a home buyer education class to qualify

MaineHousing Multi-Unit Advantage Program

This program helps with closing costs and down payments for properties with one to four units. The help ranges from $8,000 to $14,000.

- The eligibility requirements, income restrictions, and purchase price caps are the same as for the First Home program.

- Homebuyers must complete both a landlord education course and a home buyer education course.

- Buyers are required to contribute at least 1% of the loan amount towards the purchase.

In both plans, help comes in the form of a grant, and the borrower can use gift money to help pay for a portion of the home. But the details of each program are different, so people who want to buy should look carefully at both to see which one meets their needs best.

Discover more at MSNA’s website. And check HUD’s list1 of other homeownership assistance programs in Maine.

Check your home buying eligibility in Maine. Start hereMaryland down payment assistance

The Maryland Department of Housing and Community Development (MDHCD) can offer home buyer assistance through its Maryland Mortgage Program. Borrowers using the 1st Time Advantage home loan may have access to one of the following DPA options:

- Flex 5000: Receive a $5,000 interest-free loan for down payment and closing costs, with no monthly payments required. You must repay the initial $5,000 when you sell, refinance, transfer, or finish paying off the mortgage

- Flex 3% Loan: You can borrow 3% of your first mortgage under the same terms as the Flex 5000 loan.

- Partner Match: You will receive the money as a no-interest, deferred loan that you can use for the down payment and closing costs. Exclusive to specific MDHCD mortgages.

- 1st Time Advantage 6000: Receive a $6,000 interest-free loan with no recurring payments. However, if you sell or refinance before fully paying off your mortgage loan, you will need to repay the loan.

- 1st Time Advantage DPA: You can borrow up to 3%, 4%, or 5% of your first mortgage loan to pay for your down payment and closing costs.

- HomeStart: If your income is equal to or greater than 50% of the area median income (AMI), you may qualify for a DPA of up to 6% of your loan amount.

Visit MDHCD’s website for more information, as each of these plans has different qualifications. And look for other homeownership assistance programs in Maryland on HUD’s website.1

Check your home buying eligibility in Maryland. Start hereMassachusettsdown payment assistance

MassHousing offers down payment assistance (DPA) through a second mortgage loan, with two options available:

- Option 1: A deferred payment loan of up to $30,000 with 0% interest, requiring no payments until the home is sold, refinanced, or the first mortgage is paid off.

- Option 2: A 15-year loan of up to $25,000 with a 2% fixed interest rate, requiring monthly payments in addition to the first mortgage.

Eligibility is based on income and first mortgage program requirements. Assistance is available statewide in Massachusetts. To find out if you qualify, speak with a loan officer in your area. MassHousing doesn’t publish program details on its website. For a list of other local programs in Massachusetts, visit HUD’s website.1

Check your home buying eligibility in Massachusetts. Start hereMichigan down payment assistance

The Michigan State Housing Development Authority (MSHDA) offers a DPA program to assist potential buyers with closing costs and a down payment.

MI 10K DPA Loan

The M1 10K DPA Loan provides up to $10,000 in down payment assistance in specified ZIP codes if you finance your home purchase with MSHDA’s M1 Loan.

Both first-time Michigan homebuyers—those who have not bought a property in the last three years—and repeat buyers in specific areas are eligible for the program. Household income limits apply, and they vary depending on family size and property location. The maximum sales price for all properties in the state is $224,500.

A minimum credit score of 640 is needed to be eligible, or 660 if you want to buy a manufactured home with numerous sections. Completing a housing education course is also required.

MSHDA offers a homeownership education program and a mortgage credit certificate, which lowers your federal tax bill.

You can find a list of eligible zip codes on the MSHDA website. And find a list of other homeownership assistance programs in Michigan on HUD’s website.1

Check your home buying eligibility in Michigan. Start hereMinnesota down payment assistance

The Minnesota Housing Finance Agency (MHFA) provides three types of down payment assistance loans to eligible borrowers:

- Monthly Payment Loan: You can borrow up to $18,000 at the same rate you pay on your first mortgage. Over a 10-year period, pay that off in monthly installments.

- Deferred Payment Loan: First-time buyers can borrow up to $16,500 free of interest. No payments are required, but the balance becomes due when you complete paying off the mortgage, refinance, or sell the home.

- Deferred Payment Loan Plus: Receive a 0% APR loan for up to $18,000. You do not need to make monthly payments on the loan, but you must repay it in full when you relocate, sell your home, refinance, or pay off your primary mortgage.

Discover more at the MHFA’s website. And check HUD’s list1 of other homeownership assistance programs in Minnesota.

Check your home buying eligibility in Minnesota. Start hereMississippi down payment assistance

The Mississippi Home Corporation (MHC) offers a variety of mortgage products and down payment assistance programs to help homebuyers achieve homeownership.

Standard Loan Products

- Smart6: 30-year fixed mortgage with a $6,000 second mortgage at 0% interest, due upon sale, repayment, or maturity.

- Easy8: 30-year fixed mortgage with an $8,000 second mortgage at 0% interest.

- Trusty10: 30-year fixed mortgage with a $10,000 second mortgage.

- JustRate: 30-year fixed mortgage with a competitive interest rate.

Homebuyer Tax Deduction

- Mortgage Credit Certificate (MCC): Offers a tax credit equal to 40% of the annual mortgage interest paid, reducing federal tax liability. Can be combined with any MHC loan except MRB7.

Specialized Loan Programs

- Housing Assistance for Teachers (HAT): Provides up to $6,000 in grant funds for Mississippi-certified public school teachers in eligible areas.

- Home4All: Offers up to $25,000 in homebuyer assistance. Buyers must complete homebuyer education through a housing counseling agency before reserving a loan.

- DPA 14: A mortgage program in partnership with Tunica and Washington counties, offering competitive rates through Mortgage Revenue Bond proceeds.

These programs aim to make homeownership more accessible and affordable for a wide range of buyers.

Find out more at the MHC’s website. And consult HUD’s list1 of other homeownership assistance programs operating in Mississippi.

Check your home buying eligibility in Mississippi. Start hereMissouri down payment assistance

The Missouri Housing Development Commission (MHDC) offers two down payment assistance (DPA) programs for both first-time and repeat homebuyers.

MHDC First Place Program

Eligible homebuyers receive up to 4% of the purchase price of the home to assist with down payments and closing costs. Key details include:

- The assistance comes in the form of a forgivable loan, which means it may need to be repaid if the home is moved from, sold, or refinanced within the first 10 years.

- Starting at the end of the fifth year, the loan forgiveness begins, occurring monthly at one-sixtieth of its original value. By the end of the tenth year, there will be no outstanding balance.

- Other requirements include using an MHDC mortgage loan and staying within household income limits and purchase price limits.

MHDC Next Step Program

This program offers a 4% cash assistance loan for down payment or closing costs to qualified applicants, with complete forgiveness after 10 years of residing in the home as a primary residence.

Get more information from the MHDC’s website. And check out HUD’s list1 of other homeownership assistance programs in Missouri, including one operated by the Delta Area Economic Opportunity Corporation.

Check your home buying eligibility in Missouri. Start hereMontana down payment assistance

Montana Housing provides two types of down payment assistance to help with down payments and closing costs. Note that these are not grants but rather loans that need to be paid back.

Bond Advantage Down Payment Assistance Program

You can repay this program’s second mortgage alongside your primary mortgage over a 15-year period. Here are the main points:

- Borrow up to $15,000 or 5% of the purchase price, whichever is lower.

- The loan offers relatively low monthly payments. Your lender will make sure you can comfortably afford these payments.

- To qualify, applicants need a credit score of 620 and must contribute $1,000 of their own money towards the purchase.

MBOH Plus 0% Deferred Down Payment Assistance Program

Because it is a “silent mortgage,” this plan does not have any interest or monthly payments.

- Repayment is required when the property is sold or transferred to another party or when the outstanding loan secured by the first mortgage is refinanced.

- The income limits are higher than those in the Bond Advantage program. When this information was written, the limit was $80,000 for a one- or two-person household and $90,000 for a household of three or more

- You need a credit score of 620 or higher.

Remember, you need to use one of Montana Housing’s mortgage products to qualify for either of these assistance programs.

The program has lots of options and rules, so read up on the details on the website. And check HUD’s list1 of other homeownership assistance programs in the state.

Check your home buying eligibility in Montana. Start hereNebraska down payment assistance

The Nebraska Investment Finance Authority (NIFA) makes becoming a homeowner easier by providing assistance with down payments and closing costs.

NIFA Homebuyer Assistance Program (HBA)

Nebraskans who meet NIFA’s first-time buyer criteria can buy a home with a minimal $1,000 investment with the help of HBA.

- Includes both a first and second mortgage loan.

- The first mortgage has a higher interest rate to include assistance for down payments and closing costs.

- The second mortgage loan limit is 5% of the home’s purchase price, with a 10-year term and a 1% interest rate.

Please note that the minimum investment might exceed $1,000 based on the loan type and the seller’s contribution to closing costs.

Check the NIFA’s webpage for more information. And take a look at HUD’s list1 of other homeownership assistance programs in the state.

Check your home buying eligibility in Nebraska. Start hereNevada down payment assistance

If you are a prospective homebuyer in Nevada, you have several notable DPAs to choose from.

The Nevada Housing Division’s (NHD) Home Is Possible and Home First DPAs are two of these programs. However, the NHD is not the only source of assistance available. Nevada Rural Housing (NRH) administers two additional DPA programs with slightly different approaches.

NHD Home Is Possible (HIP)

The State of Nevada Housing Division’s HIP can provide up to 4% of your loan amount toward the down payment and closing costs. This takes the form of an interest-free loan.

To be eligible for Nevada’s DPA program:

- You must be a first-time home buyer, meaning you haven’t owned a home in at least three years

- You must have a minimum credit score of 640

- The home must be your primary residence

In addition, you’ll need to meet your lender’s financial requirements to qualify for the mortgage.

NHD Home First

Home First is a Nevada first-time homebuyer program that offers $15,000 in down payment assistance, forgivable after three years if the buyer stays in the home. The program also has liberal home price limits and offers a 30-year fixed rate mortgage.

To qualify for the Home First program, you must be:

- A first-time homebuyer (you have not owned a home in the past three years)

- A Nevada resident for at least six months

- Have a credit score of at least 640

- Complete a homebuyer education course

- Have an income that falls within the program’s household income limits

For more details, visit the Nevada Housing Division website.

NRH Home At Last DPA

Nevada Rural Housing’s Home At Last DPA helps low- to moderate-income borrowers purchase a home in Nevada. It provides a second mortgage with no interest and no payments for 30 years. The second mortgage is forgiven at the end of the 30-year term, or if the borrower sells, refinances, or prepays the first mortgage prior to the end of the 30-year term.

This assistance can be used to cover your down payment as well as your closing costs. Furthermore, the Home At Last program provides eligible homeowners with refinancing options.

NRH Home Means Nevada Rural DPA

This program is designed specifically for people looking to buy in rural areas of Nevada. If you qualify, you could receive up to $25,000 in forgivable down payment assistance. This assistance, like Home At Last, is a second mortgage that is completely forgiven unless you sell or refinance within the first three years.

You’ll find more detail about NRH’s offerings on its website. And check out HUD’s list1 of other homeownership assistance programs in Nevada.

Check your home buying eligibility in Nevada. Start hereNew Hampshire down payment assistance

New Hampshire Housing provides mortgage programs that offer cash assistance to prospective homeowners, helping them cover down payment and closing expenses. Up to $15,000 is awarded, which can be used for the down payment as well as related closing costs.

This loan comes in the form of a second mortgage, which is forgiven in full after five years. However, exceptions apply if the homeowner decides to sell, refinance, or declare bankruptcy within this five-year timeframe.

The program income limits determine your eligibility for aid:

- Home First: Income limits vary by county

- Home Flex Plus: Allows for incomes reaching up to $167,800

- Home Preferred Plus: Intended for those making up to 80% of the Area Median Income (AMI), according to Fannie Mae

- Home Preferred Plus Over 80% AMI: This is conventional financing tailored for those with incomes that surpass 80% of the AMI but remain below $167,800

Completing New Hampshire Housing’s homebuyer education course is a mandatory requirement to be eligible for this program.

Get more information from the authority’s website. And take a look at HUD’s list1 of other homeownership assistance programs in New Hampshire.

Check your home buying eligibility in New Hampshire. Start hereNew Jersey down payment assistance

First-time buyers in New Jersey can get up to $15,000 in down payment assistance through a five-year, forgivable loan with no interest or monthly payments required. Also, first-generation buyers may qualify for an additional $7,000 in assistance.

The loan must be paired with a first mortgage from the New Jersey Housing and Mortgage Finance Agency (NJHMFA), which can be a 30-year HFA, FHA, USDA, or VA loan.

For more information, visit the agency’s website. And consult HUD’s list1 of other homeownership assistance programs operating in the state.

Check your home buying eligibility in New Jersey. Start hereNew Mexico down payment assistance

The New Mexico Mortgage Finance Authority (MFA) assists first-time and repeat buyers with closing costs and down payments. Here’s what to expect.

MFA FIRSTDown DPA

If you’re a first-time home buyer in New Mexico or if you haven’t owned a home in the last three years, MFA may offer you $1,000 or up to 4% of the home purchase price to assist with closing costs and down payments.

- This program must be used in conjunction with New Mexico’s FIRSTHome mortgage financing program.

- There are caps on household incomes and home purchase prices. But those may be higher if you’re buying in a target area.

MFA FirstDown Plus

FirstDown Plus provides a $15,000 third mortgage loan for first-time homebuyers or those who haven’t owned a home in the past three years. Here’s what you can expect with this DPA loan:

- Must be used with MFA’s FirstHome and FirstDown programs.

- Eligibility requirements are consistent across all related programs.

- Offers a $15,000, 10-year, non-amortizing loan at 0% interest, specifically for down payment.

- The loan is forgivable after 10 years of continuous occupancy without selling, refinancing, renting, or vacating.

- Combined DPA from FirstDown and FirstDown Plus cannot exceed $35,000.

MFA HomeNow DPA

HomeNow, an alternative program, provides up to $7,000 in down payment assistance. The difference is that this loan can be forgiven after 10 years and is only available to borrowers with an income below 80% of the area median income (AMI).

MFA Home Forward DPA

This initiative offers down payment assistance of up to 3% of the home’s sale price to repeat buyers who do not qualify for MFA’s first-time buyer programs. While Home Forward does provide mortgage loans, it can also be used as a stand-alone DPA for those who do not have an MFA mortgage. Because the website doesn’t provide much information about the terms of this second mortgage, speaking with an approved lender should be high on your priority list.

You can find full details on the MFA authority’s website. And read HUD’s list1 of other homeowner assistance programs in New Mexico.

Check your home buying eligibility in New Mexico. Start hereNew York down payment assistance

New York offers first-time homebuyers access to down payment assistance programs through two key agencies: SONYMA provides statewide support, while HomeFirst caters specifically to residents of New York City.

State of New York Mortgage Association (SONYMA)

Among its many programs first-time home buyer programs, SONYMA offers down payment assistance programs to qualified borrowers.

- Down Payment Assistance Loan (DPAL): Offers up to 3% of the purchase price or up to $15,000 as a second mortgage with 0% interest. This is forgiven after 10 years, as long as you don’t sell or refinance within that time

- DPAL Plus ATD: Can offer up to $30,000 for lower-income home buyers who make less than 60% of their area median income (AMI)

HomeFirst Down Payment Assistance Program

In addition, New York City has its own HomeFirst DPA that could offer up to $100,000 to eligible buyers. To qualify, borrowers must have a household income below 80% of their area median income (AMI) and pay at least 3% of the purchase price out of pocket.

Check your home buying eligibility in New York. Start hereFor links to other statewide and local programs in New York, check HUD’s list1.

North Carolina down payment assistance

The North Carolina Housing Finance Agency offers generous loans for down payments to all kinds of buyers throughout the state.

- NC Home Advantage Mortgage: First-time and repeat home buyers may be eligible for a down payment loan of up to 3% of the mortgage balance.

- NC 1st Home Advantage Mortgage: First-time home buyers and military veterans are eligible for a down payment loan of up to $15,000.

With either option, the assistance loan begins to be forgiven in year 11 of your mortgage and is fully forgiven by year 15. However, it’s worth noting that if you sell, transfer, or refinance before year 11, you must repay the entire amount.

Additionally, for those looking for even more assistance, you can explore pairing the NC Home Advantage Mortgage with the Community Partners Loan Pool DPA program, which could provide an extra $50,000 in financial support.

More information is available on the North Carolina Housing Finance Agency’s website. And review HUD’s list1 of other homeownership assistance programs in the state.

Check your home buying eligibility in North Carolina. Start hereNorth Dakota down payment assistance

The North Dakota Housing Finance Agency (NDHFA) offers two programs, “Start” and “DCA,” to assist with upfront home buying closing costs. Both programs can provide up to 3% of the mortgage amount for your down payment, closing costs, and prepaid items.

To qualify, you’ll have to have a household income below certain caps. And the value of the home you’re buying may also be limited.

You can find details on the NDHFA website. And take a look at HUD’s list1 of other homeownership assistance programs in North Dakota.

Check your home buying eligibility in North Dakota. Start hereOhio down payment assistance

If you’re buying a home in Ohio, either the Ohio Housing Finance Agency (OHFA) or Communities First Ohio can help you with your down payment and closing costs.

OHFA Your Choice! DPA

The Ohio Housing Finance Agency has a down payment assistance program that provides either 2.5% or 5% of the home’s purchase price.

- The DPA takes the form of a loan that is forgiven after seven years. If you sell, transfer, or refinance before then, you will need to repay the loan.

- A credit score of 640 or higher is required for a conventional, USDA, or VA loan. Buyers who have FHA loans must have a FICO score of 650 or higher.

- Income limits and purchase prices limits apply.

OHFA Grants for Grads

If you are a recent graduate, OHFA also offers a 2.5% or 5% assistance loan to cover the down payment and closing costs. This loan is forgiven after five years if you do not refinance, move, or sell your home.

To qualify, you must have obtained a degree from an accredited college or university within the last 48 months. This includes associate’s, bachelor’s, master’s, doctorate, or other post-graduate degrees. Additionally, you need to complete a free home buyer education course from a HUD-approved counseling agency.

Get more information from MyOhioHome’s website.

Communities First Ohio DPA

If you’re eligible, Communities First Ohio might offer you a grant of 3%, 4%, or 5% of your home’s purchase price to help cover down payments and closing costs. Since it’s a grant, you don’t have to pay it back.

The rules and eligibility criteria will be similar to those for OHFA programs. However, qualified buyers will also require:

- FICO score of 620 or more

- Not exceed maximum income limits (varies by county)

- Use an approved lender

- Your property must be your primary residence

You may also be able to qualify for one of these grants more easily than you would for an OHFA loan. Because only the borrower’s income is considered, not the income of the entire household.

You can find more details on the program’s website. And consult HUD’s list1 of other homeownership assistance programs in Ohio.

Check your home buying eligibility in Ohio. Start hereOklahoma down payment assistance

The Oklahoma Housing Finance Agency (OHFA) and REI Oklahoma both offer down payment and closing cost assistance to homebuyers in the Sooner State.

OHFA Down Payment Assistance

The Oklahoma Housing Finance Agency offers its OHFA Homebuyer Down Payment Assistance program. This provides down payment assistance loans to eligible borrowers using a 30-year fixed-rate mortgage. Those secondary loans are 3.5% of the primary mortgage amount.

To qualify, you’ll likely need a credit score of 640 or better. And your household income will be capped according to family size and the county of purchase.

Learn more at OHFA’s website.

Check your home buying eligibility in Oklahoma. Start hereREI Home100 DPA

REI Oklahoma, a well-known nonprofit organization, offers affordable home financing through conventional or government loans, as well as down payment assistance for eligible borrowers.

Down payment assistance is provided in the form of a grant, which the organization refers to as a “gift,” or a seven-year forgivable second mortgage. Depending on your first mortgage, you could receive up to 5% of your loan.

You do not have to be a first-time home buyer to qualify. However, to be eligible for the REI Home100 program, you must meet the following criteria:

- A minimum credit score of 640

- Your debt-to-income ratio shouldn’t be higher than 45%

- Your income must be within the limits set by REI Oklahoma, which change depending on your mortgage type

- Use an REI Oklahoma approved lender

You’ll find more information and a list of approved lenders on the program’s website. And take a look at HUD’s list1 of other homeownership assistance programs operating in Oklahoma.

Oregon down payment assistance

Oregon Housing and Community Services (OHCS) offers down payment assistance programs for first-time buyers. Unfortunately, the OHCS site doesn’t say much about how much financial help buyers can get or how it works, so it’s best to call the housing agency directly for more information.

We do know this assistance is intended for low- and very low-income families and individuals, with a particular focus on underserved populations. The state agency sends money to various local agencies that provide direct assistance to home buyers.

There’s a list of those agencies on the OHCS website, along with the county or counties each serves. Links are provided there for every agency. Also check out HUD’s list1 of other homeownership assistance programs in the state.

Check your home buying eligibility in Oregon. Start herePennsylvania down payment assistance

The Pennsylvania Housing Finance Agency (PHFA) offers a variety of down payment assistance programs.

- PHFA Grant: Provides a $500 grant that can be used in conjunction with an HFA Preferred loan.

- Keystone Advantage Assistance Loan Program: Provides a second mortgage up to $6,000 or 4% of the purchase price, whichever is less. Paid off over 10 years at zero percent interest.

- Keystone Forgivable In Ten Years Loan Program (K-FIT): Offers up to 5% of the purchase price or appraised value (whichever is less). Forgiven over ten years at a rate of 10% per year.

- Access Down Payment and Closing Cost Assistance Program: You might be eligible for a no-interest loan of up to $15,000 for a down payment and closing costs if you or a family member has a disability. There are also additional funding options for accessibility modifications.

- HOMEstead DPA:. Assistance of up to $10,000 in the form of a zero-interest second mortgage loan. Funds are forgiven at a rate of 20% per year, so if you haven’t sold or refinanced by year five, you’ll own nothing.

- Employer Assisted Housing (EAH) Initiative. If your employer is part of an EAH program, then you may qualify for up to $8,000 in down payment and closing cost assistance in the form of an interest free loan amortized over 10 years.

Each program has its own eligibility criteria and a list of acceptable mortgage loan programs. You can get details from the agency’s website. And consult HUD’s list1 of other homeownership assistance programs in Pennsylvania.

Check your home buying eligibility in Pennsylvania. Start herePuerto Rico and U.S. Virgin Islands down payment assistance

Home buyers in Puerto Rico and the U.S. Virgin Islands may benefit from programs that offer down payment assistance, low-interest loans, and other valuable resources to make homeownership more attainable.

Puerto Rico Housing Finance Authority (PRHFA)

The Puerto Rico Housing Finance Authority (PRHFA) program is a valuable resource for low and moderate-income homebuyers in Puerto Rico. It provides low-interest loans and down payment assistance, making homeownership more accessible for those who need it.

Eligible households may receive up to a maximum of $55,000 in assistance, and properties in PRDOH-certified urban centers can potentially receive an additional $5,000 towards the purchase price.

Check your home buying eligibility in Puerto Rico. Start hereRead more about meeting the program’s requirements as well as qualifying properties on the PRHFA website.

Virgin Islands Economic Development Authority

“VI Slice” Moderate Income Homeownership Program is a valuable resource for home buyers in the U.S. Virgin Islands. This program aims to increase homeownership rates among moderate-income households in the U.S. Virgin Islands. It offers opportunities such as down payment and closing cost assistance, home purchase with rehabilitation, and new home construction.

Qualifying borrowers may receive a grant or a no-interest second mortgage of up to 20% of the home sale price, with a maximum of $85,000. You’ll need to meet a number of requirements, including:

- You must remain in the home as your primary residence for 10 years.

- The maximum combined loan-to-value ratio may not exceed 95%.

- You must secure your first mortgage from a participating lender.

You’ll find eligibility guidelines and property requirements in the program’s online brochure.

Rhone Island down payment assistance

For qualified first-time home buyers, Rhode Island Housing (RIHousing) offers a combination of grants and repayable down payment assistance loans to be used in conjunction with a RIHousing mortgage. The maximum purchase price for all DPA programs is $838,592, with income limits of $134,320 for a 1-2 person household and $154,468 for larger households.

RI Statewide DPA Grant

This is a more recent service from RIHousing that offers non-repayable grants for up to $17,500 in down payment and closing cost assistance. To qualify, a person must be a first-time buyer, purchase a primary residence, and satisfy the standard requirements for credit score, income, and homebuyer education.

10kDPA program

This initiative is meant for people who need to borrow up to $10,000 for a down payment. This is a no-interest loan that is repayable when the home is sold, transferred, or refinanced. To qualify, you must have a credit score of at least 660.

Extra Assistance program

This program offers a larger loan amount of up to 6% of the purchase price, up to a maximum of $20,000. This is a traditional second mortgage that requires equal monthly payments for 15 years at the same interest rate as the new mortgage. The advantages include a lower credit score requirement of just 620 and the ability to use it for both down payments and closing costs.

FirstGenHomeRI program

A dedicated program for first-generation homebuyers in select cities offering a $25,000 forgivable loan to be used for a down payment and closing costs. This is a zero-interest loan with no monthly payments that is forgiven after five years. Use of an approved lender and completion of a homebuyer education course are also requirements of the program.

Discover more at Rhode Island Housing’s website. And explore HUD’s list1 of other homeownership assistance programs in the state.

Check your home buying eligibility in Rhode Island. Start hereSouth Carolina down payment assistance

The South Carolina State Housing Finance and Development Authority, or SC Housing, provides both mortgage loans and several down payment assistance options.

SC Housing Palmetto Home Advantage Program

A DPA of up to 4% of the loan amount is also an option. To be eligible, a credit score of at least 640 is needed. This loan is comparable to the SC Housing Homeownership Program in that it has a ten-year forgiven term, a 0% interest rate, and no monthly payments.

SC Housing Choice Voucher Homeownership Program (HCV)

Participants in the Housing Choice Voucher program have the opportunity to transition from renting to homeownership. Eligible households can transform their rental vouchers into home purchase vouchers if they meet certain conditions. These include the household head having rented a home for a minimum of one year with an HCV/Section 8 voucher, maintaining good standing within HCV program requirements, and holding continuous full-time employment for at least one year.

SC Housing County First Initiative

County First offers a rural initiative for home buyers in underserved areas. It provides up to $8,500 in forgivable down payment assistance alongside special fixed-rate financing for both first-time and move-up borrowers, with options for FHA, conventional, USDA, or VA loans.

This funding is available to buyers in specific targeted counties across South Carolina who meet the SC Homebuyer Program’s income and home price limits. Eligible properties include single-family residences, condominiums, townhomes, and modular homes.

For more details, visit the agency’s website. Also check out HUD’s list1 of other homeownership assistance programs operating in South Carolina.

Check your home buying eligibility in South Carolina. Start hereSouth Dakota down payment assistance

The South Dakota Housing Development Authority (SDHDA) offers down payment assistance via the Fixed Rate Plus loan.

Fixed Rate Plus

Fixed Rate Plus can provide 3% or 5% of the purchase price to help with your down payment and closing costs. It takes the form of a second mortgage with 0% interest and no monthly payments. The loan amount comes due when you sell the home or refinance.

For more information, visit SDHDA’s website. And check HUD’s list1 of other homeownership assistance programs in the state.

Check your home buying eligibility in South Dakota. Start hereTennessee down payment assistance

Depending on which program you qualify for, the Tennessee Housing Development Agency’s Great Choice Home Loan offers down payment assistance of between $6,000 and $15,000.

Deferred Option

The Deferred Option offers a $6,000 forgivable second mortgage with no interest, which does not require payments and is forgiven after 30 years. However, if the home is sold or refinanced before the 30-year period ends, the loan must be repaid in full.

Amortizing Option

Alternatively, the Amortizing Option provides down payment assistance of up to 5% of the purchase price, capped at $15,000, which is paid back over 30 years with the same interest rate as your first mortgage.

You can use the funds from both loans towards closing costs and a down payment. All borrowers must first register for the state’s homebuyer education course.

For more details, go to the TDHA website. And read HUD’s list1 of other homeownership assistance programs in Tennessee.

Check your home buying eligibility in Tennessee. Start hereTexas down payment assistance

The TDHCA My First Texas Home and My Choice Texas Home programs offer significant down payment assistance to help make homeownership more accessible in Texas.

My First Texas Home

The My First Texas Home program offers up to 5% of the loan amount in down payment and closing cost assistance for first-time homebuyers. You must repay this assistance as a no-interest deferred loan when you refinance, sell, or pay off the mortgage. You can choose from FHA, VA, and USDA loan options, each offering a 30-year fixed-rate mortgage with a below-market interest rate.

My Choice Texas Home

The My Choice Texas Home program extends its reach beyond first-time buyers, offering up to 5% of the loan amount for down payment and closing costs. This program is designed for individuals interested in conventional loans, such as financing through a Fannie Mae HFA Preferred conventional loan, as well as government-backed loans. The assistance provided is designed to make the home buying process more affordable, regardless of buyer experience.

TDHCA MCC

Veterans and first-time home buyers can also benefit from the mortgage credit certificates (MCCs) offered by the Texas Homebuyer Program. You can receive a dollar-for-dollar reduction in your federal taxes with these.

Find more details about these programs on the TDHCA website, or see HUD’s list1 of other homeownership assistance programs in Texas.

Check your home buying eligibility in Texas. Start hereUtah down payment assistance

The Utah Housing Corporation (UHC) offers down payment assistance grants and loans for home buyers who secure their primary mortgage through UHC. These programs can potentially cover the entire minimum required down payment and some, or all, of the closing costs.

UHC Down Payment Assistance

To qualify for Utah Housing’s down payment assistance, you need to meet the requirements for a first mortgage with Utah Housing Corp through an approved lender. This lender will assess your financial needs and direct you to a suitable Utah Housing Corp loan that can cover your down payment and, potentially, your closing costs with a 30-year fixed-rate second mortgage. Given the limited information available, it’s important to speak with an approved lender to learn more about the terms of this DPA.

First-Time Homebuyers New Construction Assistance Program