Key Takeaways

- An FHA Streamline Refinance lets you refinance without verifying income, employment, or credit under the non-credit-qualifying option.

- You can only use an FHA Streamline Refinance if your current mortgage is an FHA loan.

- The refinance must provide a "net tangible benefit," such as lower mortgage payments or a lower interest rate.

- You cannot take cash out with an FHA Streamline Refinance.

If you currently have an FHA mortgage, the FHA Streamline Refinance is the easiest way to get a lower rate and monthly payment.

The FHA Streamline is a “low-doc” refinance with limited paperwork required. The lender doesn’t have to verify your income or credit, and there’s no home appraisal. That means a Streamline Refinance closes faster than other loans and has slightly cheaper closing costs.

Thanks to the FHA Streamline Refinance, borrowers with FHA loans have easier access to today’s competitive FHA refinance rates than most other homeowners.

In this article (Skip to…)

- Streamline Refinance rates

- How the loan works

- Benefits

- Drawbacks

- Requirements

- Mortgage insurance premiums

- Streamline vs cash-out refi

- FAQ

What is an FHA Streamline Refinance?

An FHA Streamline Refinance is a simplified refinancing option for homeowners with an existing FHA loan. It replaces the current mortgage with a new one at a lower interest rate or monthly payment, skipping many standard underwriting steps. The program usually eliminates the need for a home appraisal and, in many cases, income and credit verification. This allows borrowers to refinance more quickly and with less paperwork than a traditional refinance.

Check your FHA Streamline Refinance eligibility. Start hereBenefits of the FHA Streamline Refinance program

- Competitive refinance rates: FHA loan rates currently average 6.7% (6.741% APR).* This is a lower rate compared to much of the mortgage industry

- Lower MIP rates: If you got an FHA loan prior to 2023, you can access today’s lower annual mortgage insurance premiums using FHA streamline refinancing

- MIP refund: Homeowners who use the FHA Streamline Refinance may be refunded up to 68% of their prepaid mortgage insurance, in the form of an MIP discount on the new loan

- No appraisal: You could use the FHA Streamline Refinance even if your current mortgage is underwater

- No verification of job or income: You may be eligible for FHA Streamline refinancing even if you recently lost your job or took a pay cut

- No credit check: A low credit score won’t stop you from using the FHA Streamline’s non-credit qualifying option. This is almost impossible to find with other refinance loans

If you have an existing FHA loan and want to refinance into a lower interest rate, the FHA Streamline Refinance should be your first stop. Its benefits are nearly unmatched by any other refinance option.

*Interest rates updated daily according to The Mortgage Reports' lender network. See our full rate assumptions here

FHA Streamline Refinance rates

Today’s average 30-year FHA rate is 6.7% (6.741% APR) according to our lender network. But remember, the FHA mortgage insurance fee adds 0.55% in annual costs. This also applies to Streamline Refinances.

Verify your FHA Streamline Refinance eligibility. Start hereToday’s FHA refinance rates, May 19, 2026

| 30-Year FHA Fixed Rate | 6.7% (6.741% APR) |

| 15-Year FHA Fixed Rate | 6.7% (6.741% APR) |

| 30-Year Conventional Rate | 6.692% (6.758% APR) |

| 15-Year Conventional Rate | 6.011% (6.102% APR) |

Interest rates are for example purposes only. Your own rate will vary. See our rate assumption here.

How does the FHA Streamline Refinance work?

An FHA Streamline Refinance replaces your current FHA loan with a new FHA mortgage aimed at lowering your rate, reducing your monthly payment, or providing a more stable loan option. You can select a fixed-rate or adjustable-rate mortgage with a 15- or 30-year term, and the FHA does not impose a prepayment penalty. The program allows you to refinance from a 30-year loan into a 15-year loan within specific payment limits, or extend a 15-year loan to 30 years to lower monthly payments, even if this increases total interest paid over time. FHA Streamline rates align with FHA purchase rates, and the program permits refinancing with little or no equity, as long as every loan meets the FHA’s net tangible benefit requirement.

Common net tangible benefits include:

- Lower monthly principal and interest payments

- A reduced combined interest rate and mortgage insurance cost

- Moving from an adjustable-rate mortgage to a fixed-rate mortgage

- Shortening the loan term to reduce long-term interest

- More predictable payments through a more stable loan structure

Another big benefit is that FHA Streamline Refinance rates are the same as FHA home purchase rates. There’s no penalty for being underwater or having very little equity.

FHA Streamline Refinance pros and cons

| FHA Streamline Refinance Pros | FHA Streamline Refinance Cons |

| Easy to qualify, especially with non-credit qualifying option | No cash-back allowed |

| Access today’s lower interest rates | Some lenders impose minimum credit score requirements |

| Lower MIP rates for some borrowers | You can’t shorten your loan term |

| No home appraisal is necessary | Closing costs can’t be rolled into the loan balance |

FHA Streamline Refinance benefits

The FHA Streamline Refinance comes with several benefits that make it an attractive option for some homeowners. Here are the key advantages:

1. Potential lower monthly payments

An FHA Streamline Refinance offers the opportunity to lower your monthly mortgage payment by securing a lower interest rate.

The FHA has certain guidelines on how this is achieved, but if followed, you can enjoy smaller monthly payments. While you can’t extend your loan term by more than 12 years to achieve this, you can still lower your payment by reducing your interest rate, especially when switching from an adjustable-rate to a fixed-rate mortgage.

2. Options for underwater mortgages

The FHA Streamline program allows you to refinance even if you owe more than your home’s current value—an “underwater mortgage.” This is unique in that many refinancing options do not allow this.

You can still refinance through FHA Streamline even if your home value has decreased because the main factor determining your loan amount is the outstanding principal balance of your loan.

Check your loan options. Start here3. No home appraisal

The biggest difference between the FHA Streamline Refinance and most traditional mortgage refinance options is that the FHA Streamline Refinance doesn’t require a home appraisal.

Instead, the FHA will allow you to use your original purchase price as your home’s current value, regardless of what your home is actually worth today.

This “appraisal waiver” simplifies the refinancing process, allowing homeowners to bypass the traditional appraisal step entirely. With no appraisal required, the FHA Streamline Refinance can provide faster approval and fewer costs, making it an appealing option for many borrowers.

4. You may not need to verify income and credit score

Another big plus is that it’s fairly easy to get an FHA Streamline Refinance loan, especially the non-credit-qualifying type.

The non-credit qualifying FHA Streamline Refinance does not require most of the typical verifications you’d need to get a new mortgage.

As it’s written in the FHA’s official mortgage guidelines:

- Employment verification is not required with an FHA Streamline Refinance

- Income verification is not required with an FHA Streamline Refinance

- Credit score verification is not required with an FHA Streamline Refinance (though most lenders will check credit)

When you put it all together, you can:

- Be out-of-work

- Have no income

- Have a shaky credit report

- Have no home equity

Yet, you could still potentially be approved for an FHA Streamline Refinance’s non-credit qualifying option. That’s not as crazy as it sounds, by the way.

To understand why the FHA Streamline Refinance is a smart program for the FHA, we have to remember that the FHA’s chief role is to insure mortgages, not underwrite them.

It’s in the FHA’s best interest to help as many people as possible qualify for today’s competitive mortgage rates. Lower mortgage rates mean lower monthly payments, which, in theory, leads to fewer loan defaults.

This is good for homeowners who want lower mortgage rates, and it’s good for the FHA. With fewer loan defaults, the FHA has to pay fewer insurance claims to lenders.

In short, the FHA is helping itself when it helps you, which is why the requirements for the Streamline refi are so lenient.

5. FHA MIP refund

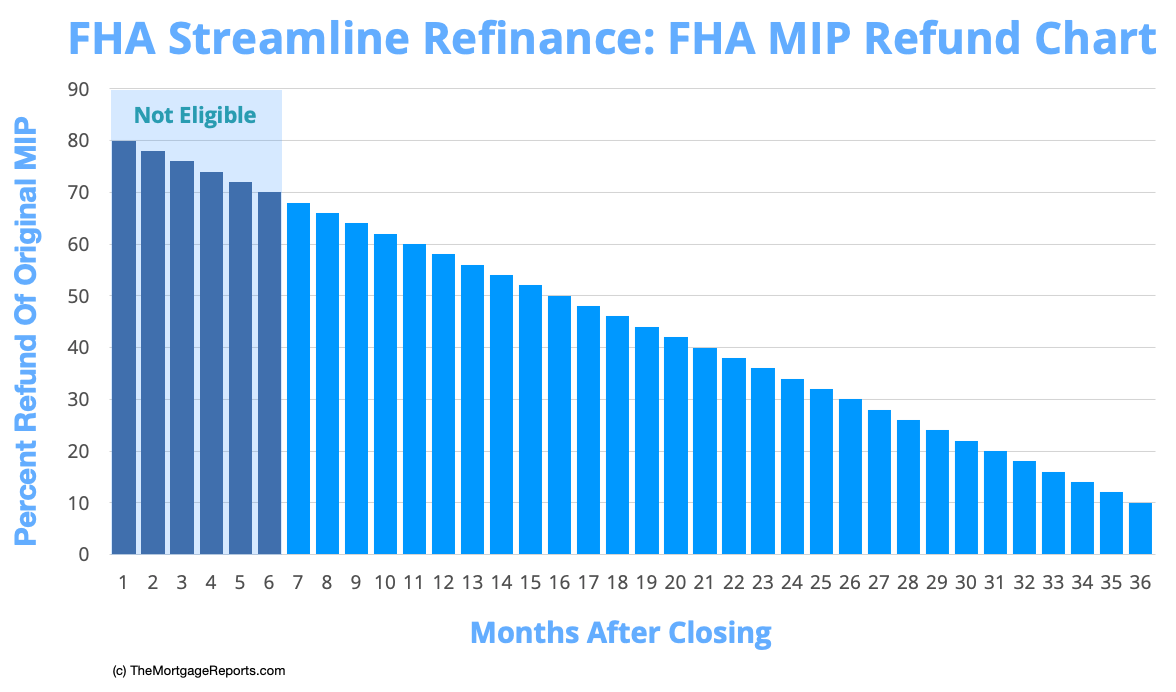

There’s an additional benefit for FHA-backed homeowners refinancing within the first three years of their existing loan origination.

The FHA provides a partial refund on the upfront mortgage insurance premium (UFMIP) you paid when you first got your FHA loan.

The size of the refund diminishes as the three-year window elapses.

For example, a homeowner who refinances an FHA mortgage after 11 months is granted a 60% refund on their initial FHA UFMIP.

Thirty days later, the refund drops to 58%. After another 30 days, it drops to 56%, and so on.

| Months After Closing | MIP Refund | Months After Closing | MIP Refund | Months After Closing | MIP Refund |

| 7 | 68% | 17 | 48% | 27 | 28% |

| 8 | 66% | 18 | 46% | 28 | 26% |

| 9 | 64% | 19 | 44% | 29 | 24% |

| 10 | 62% | 20 | 42% | 30 | 22% |

| 11 | 60% | 21 | 40% | 31 | 20% |

| 12 | 58% | 22 | 38% | 32 | 18% |

| 13 | 56% | 23 | 36% | 33 | 16% |

| 14 | 54% | 24 | 34% | 34 | 14% |

| 15 | 52% | 25 | 32% | 35 | 12% |

| 16 | 50% | 26 | 30% | 36 | 10% |

Note: FHA homeowners are only eligible for the Streamline Refinance program after six months. Thus, eligibility for an MIP refund starts at seven months.

This is why it’s rarely a good idea to “wait to refinance” an FHA loan.

With the FHA Streamline Refinance program, the sooner you refinance, the bigger your refund and the lower your total loan size for your new mortgage.

This lowers the monthly payment and preserves the home’s equity, which are two huge positives.

Verify your FHA Streamline Refinance eligibility. Start here

Disadvantages of an FHA Streamline Refinance

Despite the potential advantages of an FHA Streamline Refinance, there are several drawbacks that should be carefully considered.

- Closing costs: Borrowers will have to pay upfront closing costs, as the FHA doesn’t allow them to be rolled into the loan amount. Even though there’s a chance for these to be lower, given that appraisals or credit checks may not be necessary, the additional expense remains a concern. Some lenders might cover these fees with a no-cost Streamline Refinance, but this often results in higher interest rates

- Limited cash back: If you’re seeking to tap into your home equity for a large cash payout, the FHA Streamline Refinance might not be your best bet. This refinancing option restricts cash back to a maximum of $500. For those requiring substantial cash out, it would be better to explore other avenues, such as an FHA cash-out refinance

- Mortgage insurance requirements: FHA loans, including Streamline Refinances, mandate both annual mortgage insurance premiums (MIP) and an upfront mortgage insurance premium (UFMIP). This recurring cost protects your lender if you default on your loan, but it can add significantly to your long-term financial burden. To get rid of MIP, one must convert their FHA loan into a conventional one, which typically requires a credit score of at least 620 and reaching 20% equity in the home. This might not be viable for all borrowers

So, while the FHA Streamline Refinance can offer benefits, these disadvantages can significantly affect its value to potential borrowers. It is crucial to weigh the pros and cons carefully before choosing this, or any, refinancing option.

FHA Streamline Refinance guidelines and requirements

The FHA defines the baseline requirements for a Streamline Refinance, but lenders can add their own rules, including minimum credit scores or additional review steps. If your lender applies stricter standards, you can shop around for one that follows FHA guidelines more closely.

- Three months of on-time mortgage payments: You need to have a consistent payment history for at least the past three months. A maximum of one late payment is allowed in the last 12 months, but loans must be current at closing.

- 210-day waiting period: Borrowers must wait 210 days after their last purchase or refinance and have made six on-time payments on their current FHA-insured loan before they can apply.

- Interest rate reduction requirement: The refinance must result in a lower interest rate, typically by at least 0.50%. Alternatively, refinancing from an adjustable-rate mortgage to a fixed-rate mortgage can qualify as a benefit.

- Net tangible benefits test: ensures that a refinance provides meaningful financial advantages to the borrower, such as lower monthly payments, a more stable loan, or a shorter loan term. It prevents refinancing that would leave you in a worse financial position.

Types of FHA Streamline Refinance loans

The Federal Housing Administration offers two different FHA Streamline Refinance options:

Verify your FHA Streamline Refinance eligibility. Start here- Credit-Qualifying Streamline Refinance: Lenders will check your credit score and debt-to-income ratio to see whether you’ll be able to make the loan’s payments

- Non-Credit Qualifying Streamline Refinance: Lenders can approve this refinance without checking your credit score or verifying your income. This is the most common option

Why would anyone choose the credit-qualifying option and go through the full underwriting process?

Well, there are times when credit qualification is necessary, like when you’re adding a new co-borrower to the loan or removing an existing co-borrower. In other cases, qualifying for the loan all over again could save you money. If your credit profile has improved a lot since you got your original loan, you might qualify for an even better interest rate, for example.

Note that cash-out refinancing is not permitted under the FHA Streamline Refinance, but it is allowed with the FHA cash-out refinance.

Should you use the FHA Streamline Refinance?

What documents do I need for an FHA Streamline Refinance?

The FHA Streamline Refinance is a “low-doc” refinance loan, meaning it requires less paperwork than most other mortgages. But you’ll still need some documentation, including:

- A loan application

- A current mortgage statement showing a six-month payment history

- Contact information for your employer (the lender may verify employment but not income)

- Two months’ worth of bank statements showing you can cover out-of-pocket closing costs

- Utility bills show you use the home as a primary residence

If you use the FHA’s credit-qualifying Streamline Refinance, you will need to “re-qualify” with your income and credit score. This option would be required if you were removing a co-borrower from the loan.

What happens to FHA mortgage insurance if you use the Streamline Refinance?

Like other FHA loans, the FHA Streamline Refinance requires borrowers to pay mortgage insurance.

Verify your FHA Streamline Refinance eligibility. Start hereEven if you’ve built equity in the home since purchasing it, the FHA Streamline Refinance cannot be used to eliminate the mortgage insurance premium (MIP).

FHA borrowers are required to make two types of mortgage insurance payments:

- Upfront Mortgage Insurance Premium (UFMIP): 1.75% of the loan amount added to your loan (not due as cash at closing)

- Annual Mortgage Insurance Premium (MIP): 0.55% of the loan amount split into 12 installments, which are paid with your mortgage each month

This is true for Streamline Refinance loans as well as purchase loans.

“For borrowers who qualified for an MIP refund, the refund can be applied toward this total new upfront cost,” adds Meyer.

1. Upfront Mortgage Insurance Premium (UFMIP)

Not all refinancing households will pay the full amount of upfront MIP.

As shown in the chart above, those using an FHA Streamline Refinance within three years of their original loan stand to get an upfront MIP refund.

This can significantly lower the amount of UFMIP added to your new loan and reduce the amount you have to pay overall.

2. Annual Mortgage Insurance Premium (MIP)

The annual MIP cost for an FHA Streamline Refinance is as follows:

- 30-year loan terms with an LTV over 90% have an annual MIP of 0.50%, payable for the life of the loan

- 15-year loan terms with an LTV over 90% have an annual MIP of 0.40%, payable for the life of the loan

- 30-year loan terms with an LTV under 90% have an annual MIP of 0.50%, payable for 11 years

- 15-year loan terms with an LTV under 90% have an annual MIP of 0.15%, payable for 11 years

If you got your existing FHA loan before March 2023, when MIP rates were higher, you could lower your MIP rate with an FHA Streamline Refinance.

The FHA’s MIP rules have changed a lot over the years, and the age of your loan will help determine how much you could save.

If your current FHA MIP is higher than what’s shown above, consider starting a refinance immediately to benefit from a new, lower FHA MIP.

Verify your FHA Streamline Refinance eligibility. Start hereFHA MIP Cancellation Policy

The FHA requires most homeowners to pay mortgage insurance for the life of the loan.

Only homeowners with a starting loan-to-value ratio of 90% or less can cancel mortgage insurance after 11 years. (An LTV of 90% or less means you made at least a 10% down payment.)

Verify your FHA Streamline Refinance eligibility. Start hereRefinancing homeowners could also bring cash to closing to reduce their loan balance and change their MIP disposition. However, not everyone will have the cash to make such a move.

This is why, when exploring an FHA Streamline Refinance, you should also look at other mortgage refinance options, including conventional mortgage loans via Fannie Mae or Freddie Mac.

If you can qualify for a low rate, conventional loans have a big plus: You can cancel private mortgage insurance (PMI) once your loan-to-value ratio falls below 80%.

The FHA allows its homeowners to refinance to a conventional loan to cancel the FHA MIP.

FHA Streamline Refinance vs. FHA Cash-Out Refinance

Compared to FHA Streamline Refinance loans, the FHA cash-out refinance has an obvious benefit: you can use it to access cash from your home equity.

Say, for example, that you owe $250,000 on your current loan but your home is worth $350,000. The difference between these two numbers—$100,000—is your home equity.

Verify your FHA Streamline Refinance eligibility. Start hereWith a cash-out loan, you could access part of this equity while also refinancing your entire mortgage. Your loan amount would increase as a result.

With an FHA Streamline Refinance, your loan amount cannot increase to generate cash back, even if you do have the equity to back a larger loan.

If you’re considering a cash-out refinance instead of a Streamline loan, know that:

- You’ll need to qualify with your debt, income, and credit score

- You’ll need a new home appraisal to verify your home’s value

- You can refinance any type of mortgage, not just an FHA loan

- Your loan amount will increase so your annual MIP will, too

- You won’t be able to access all your equity — only up to 80%

- Your mortgage rate could increase since cash-out loans are riskier

A Streamline loan is designed for simplicity, so it can avoid most of the additional steps cash-out loans require.

FHA Streamline Refinance FAQ

Compare FHA refinance options. Start hereCheck your FHA Streamline Refinance eligibility

FHA mortgage rates are competitive, and homeowners typically close faster with an FHA Streamline Refinance. Remember: the sooner you close, the bigger your FHA MIP refund.

Start by comparing current FHA refinance rates to see how much you could save.

Time to make a move? Let us find the right mortgage for you