In this article:

Most creditors have a policy that defines applicants’ credit score ranges. In most cases, the credit score used is the FICO, and there are about 50 types of FICO scores. Here’s how credit bureau Experian ranks its FICO scores:

- Exceptional – 800 and above

- Very good – 740 to 799

- Good – 670 to 739

- Fair – 580 to 669

- Poor – 579 and lower

If you’re trying to finance a house, buy insurance or even get a job, your FICO score could impact what you’re offered.

Verify your new rateFICO score: What is it, anyway?

Related: Mortgage shopping with a 640 credit score? You have options

For those with credit scores below 580, 61 percent have historically been delinquent. If you’re a lender, you will certainly charge a lot less interest for someone with a high credit score than you will someone who represents 61 times more risk.

If you’ve ever wondered, “What is a good FICO score?” the answer is a sure and certain “it depends.” Higher is always better than lower, but for most mortgage borrowers, “just enough” can be perfectly okay.

FICO scores – “FICO” is a leading brand in the credit score industry – are crucially important for mortgage borrowers. If you have a solid credit score, you will pay less to borrow. If you have a weak credit score, your cost to borrow will increase. And in some cases, you will be unable to borrow at all.

Verify your new rateFICO scores are history

Credit scoring companies like FICO create scores based on your borrowing and repayment history. They analyze data from millions of consumers, and determine what factors accurately predict your risk of defaulting on loans.

Relayted: Why high income plus low credit score equals no mortgage

For example, people who miss mortgage payments are far more likely to file bankruptcy than those who do not. So missing a mortgage payment can really devastate your score.

The lower your score, the higher your risk.

What FICO scores don’t consider

Credit scores do not reflect income – it’s entirely common for people with big earnings to have weak credit, and for people with small wages to have great credit.

Credit scores may not include all of your bills. For example, if you rent a home from a private owner, he or she will probably not report your payment history to credit bureaus. In that case, it’s up to you to maintain records proving your on-time payment history.

Related: Renting credit score: You might need a higher FICO to rent than to buy

If you deal with payday lenders and other sources that don’t report your good payment history, it can cause credit score problems. That’s because only bad payment history makes to your report and score.

“If you don’t pay your loan back,” says the Consumer Financial Protection Agency, “And your lender sends or sells your payday loan debt to a debt collector, it is possible the debt collector might report this debt to one of the major national credit reporting companies. Debts in collection could hurt your credit scores.”

Errors

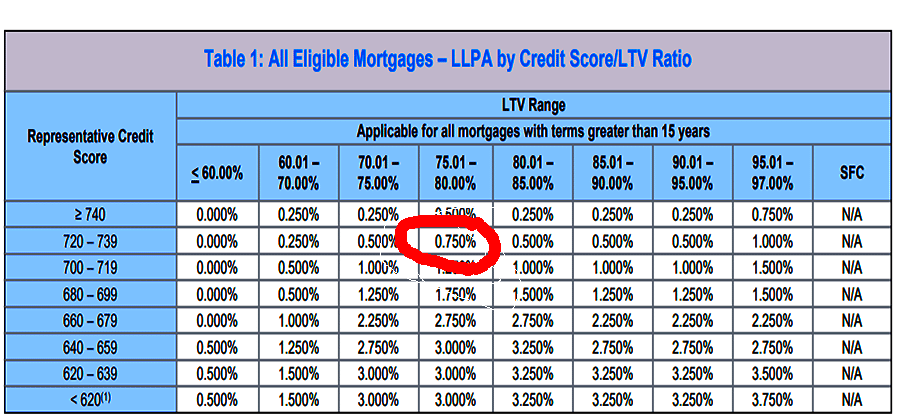

Incorrect or out-of-date information on your credit report can reduce your score. And that can cost you when you shop for a mortgage. Fannie Mae’s Loan Level Pricing Adjustment Matrix, pictured below, shows just how much extra a lower score can cost you.

Errors do happen. A few years ago, a study by the Federal Trade Commission found that “Five percent of consumers had errors on one of their three major credit reports that could lead to them paying more for products such as auto loans and insurance.”

Related: Use a "rapid rescore" to fix errors and qualify for a mortgage fast

Because of possible errors, it’s important to check your credit reports regularly. By law, you can do this for free with each of the three leading credit reporting agencies every 12 months. Go to AnnualCreditReport.com, the only site authorized by the federal government.

What FICO score do you need for a mortgage?

Most successful mortgage borrowers today have solid credit scores. According to Ellie Mae, the typical closed mortgage in October had a credit score of 724. However, you can get mortgage financing with lower scores.

HUD, the Department of Housing and Urban Development, allows FHA borrowers to purchase with 3.5 percent down with a credit score of 580 or better. Those with credit scores between 500 and 580 must put at least 10 percent down.

The VA has no credit score requirement. However, lenders who originate such financing can require minimum credit scores.

Related: What credit score do you (really) need for a mortgage?

Conforming (Fannie Mae and Freddie Mac) lenders generally want 620, but some may want more. For instance, if you’re looking for a cash-out refinance with duplex you may need to score at least 700.

Understand that just because a program like FHA allows lenders to approve an applicant with a 500 FICO score doesn’t mean lenders have to approve an applicant. In fact, getting a mortgage at that level is very difficult. If you have a low score but a decent payment history, you have a chance.

Fast ways to improve your credit score

The best way to improve your score is to develop good habits — pay your bills on time and don’t carry balances from month to month. But there are a few ways to speed up the process.

One way is to become an “authorized user” on accounts of family members or friends who already have good credit. You don’t actually use the account. You don’t even need to know the account number. But their good payment history will show up on your credit report and score.

Related: 5 ways to raise your FICO credit score today

Paying off credit card debt with a personal loan or home equity loan can improve your score because it reduces the utilization ratio of your revolving accounts. That ratio equals your credit card balances divided by the amount of your credit lines. If you have a $5,000 credit line and use $1,000, your utilization is 20 percent.

If you pay that off with an instalment loan, your utilization drops to zero. But don’t run the card up again or you will be worse off. Instalment loans are good sometimes because you have fixed payments that eventually erase your balance.

Best mortgages for good FICO scores

The “best” loan option will be the one which has the lowest cost and most-closely fits your financial needs. Your “best” loan option and what’s best for someone else may be completely different mortgage products, and that’s okay.

What counts is this: if you have a solid credit score, you have choices. You can let lenders compete for your business, and more competition means better rates and terms for you.

Time to make a move? Let us find the right mortgage for you