Key Takeaways

- The VA IRRRL lets eligible veterans refinance an existing VA loan to a lower rate or payment with minimal paperwork.

- Most borrowers can skip income, employment, and credit verification, and many lenders do not require an appraisal.

- Closing costs are typically lower than other refinance options and can often be rolled into the loan.

The VA IRRRL, or VA Interest Rate Reduction Refinance Loan, is a streamlined refinance option that allows eligible veterans and service members to replace an existing VA-backed mortgage with a new loan offering a lower interest rate, lower monthly payments, or a switch from an adjustable-rate loan to a fixed-rate loan. A VA IRRRL reduces much of the hassle typically involved in traditional refinancing by limiting documentation, often skipping income and credit checks, and frequently avoiding a home appraisal. However, the refinance must provide a net tangible benefit, meaning it lowers your monthly payment, reduces your interest rate, or replaces an adjustable-rate loan with a fixed-rate loan.

In this article (Skip to…)

- VA IRRRL guidelines

- VA IRRRL requirements

- VA IRRRL rates

- How it works

- IRRRL benefits

- VA Streamline lenders

- IRRRL vs. VA cash-out

- Pros and cons

- VA Streamline FAQ

VA IRRRL Streamline Refinance guidelines

When pursuing a VA IRRRL, following certain guidelines can help ensure a smooth and successful refinancing process. While not mandatory, these VA IRRRL guidelines are commonly adopted by lenders.

- Credit Score: A credit score of 620 or higher is often recommended to improve your chances of approval.

- Loan-to-Value (LTV) Ratio: Maintaining a reasonable LTV ratio is suggested, especially if you’re planning to roll closing costs into the loan.

- Payment History: Consistent payment history on your existing VA loan is encouraged, as it demonstrates financial stability, even though income verification isn’t required.

Remember that these VA IRRRL guidelines offer recommended practices that lenders typically follow to streamline the process, whereas requirements (covered in the next section) are the mandatory conditions that must be met to qualify for an IRRRL.

VA IRRRL Streamline Refinance requirements

To qualify for a VA Streamline Refinance (IRRRL) and meet VA IRRRL requirements, your current mortgage must be a VA home loan. Homeowners also need to satisfy underwriting standards set by the Department of Veterans Affairs.

Check your VA IRRRL eligibility. Start here2026 VA IRRRL requirements

- Existing VA Loan: The borrower must currently have a VA-backed home loan.

- Occupancy: The property being refinanced must be the borrower’s primary residence.

- Timely Mortgage Payments: The borrower should have a good payment history on the existing VA loan, with no more than one late payment in the past 12 months.

- Net Tangible Benefit: The refinance must result in a tangible benefit to the borrower, such as a lower interest rate, lower monthly payment, or a move from an adjustable-rate mortgage to a fixed-rate mortgage.

- Funding Fee: In most cases, a funding fee is required, but it can be included in the loan amount.

- No Cash-Out: IRRRL is designed for rate and term refinancing only; it does not allow for cash-out refinancing.

- No Appraisal or Credit Underwriting: In many cases, an appraisal or credit underwriting may not be required, making the process more streamlined.

You can easily figure out if you meet the VA IRRRL requirements by checking with your current mortgage lender, or any other lender that’s authorized to do VA loans (most are).

VA IRRRL rates today

VA IRRRL rates are some of the best mortgage rates on the market. Thanks to backing from the Department of Veterans Affairs, lenders can offer exceptionally low interest rates on these loans.

Check your VA IRRRL eligibility. Start hereVA IRRRL rates today, August 2, 2026

| Loan Type | Today’s VA Refinance Rate |

| VA 30-year fixed-rate | 6.485% (6.527% APR) |

| VA 15-year fixed-rate | 6.485% (6.527% APR) |

| VA 5/1 ARM | 6.391% (6.201% APR) |

Today’s starting rate for a 30-year VA IRRRL is 6.485% (6.527% APR), according to our lender network*, reflecting some of the best VA IRRRL rates today.

Of course, VA refinance rates vary by customer. Your rate will likely be higher or lower than average depending on your loan size, credit score, loan-to-value ratio, and other factors.

*Interest rates and annual percentage rates for sample purposes only. Average rates assume 0% down and a 740 credit score. See our full loan VA rate assumptions here.

How does the VA IRRRL Streamline Refinance work?

Like any refinance, the VA IRRRL replaces your current VA mortgage with a new loan that resets the term to 15 or 30 years, depending on the option you choose. The VA Streamline Refinance works differently from a standard refinance because lenders typically do not require income, employment, or credit verification, which minimizes paperwork and speeds up approval. You also don’t need a new Certificate of Eligibility (COE), as the IRRRL is only for an existing VA loan and automatically confirms your eligibility. Most lenders also skip the home appraisal, which often shortens the underwriting process and allows VA Streamline loans to close faster than other refinance options.

Check your VA IRRRL rates. Start hereIs the VA IRRRL program worth it?

The VA IRRRL program makes sense for many homeowners because it can lower the interest rate, reduce the monthly payment, or convert an adjustable-rate mortgage into a fixed-rate loan with minimal paperwork. The program allows borrowers to skip income and employment verification and often avoid a home appraisal, thereby speeding up the process and reducing documentation. Many lenders also allow closing costs to be rolled into the loan balance, reducing the need for upfront cash. The VA requires a net tangible benefit, meaning the refinance must provide a clear financial advantage, such as lower payments, more predictable loan terms, or long-term interest savings.

Benefits of a VA Streamline Refinance

The VA IRRRL lets veterans and service members refinance their current mortgage loan to a lower rate and monthly payment.

Check your VA IRRRL eligibility. Start hereThe biggest benefits of the VA Streamline refinance program compared to other VA loan refinance options are:

- Limited paperwork

- Low interest rates

- No private mortgage insurance (PMI)

- Appraisal typically not required

- May be able to refinance with little or no equity

- You might have low or no closing costs

- A low credit score won’t disqualify you

- Available to most veterans and active-duty members of the armed forces from all branches, including many Reserves and National Guard members

The VA IRRRL program appeals to many borrowers because it makes refinancing easier for existing VA homeowners. Still, lenders set their own rules, so borrowers should compare refinancing options to avoid credit checks or appraisals.

VA IRRRL mortgage lenders

It pays to shop around for the best mortgage lender when you do a VA Streamline Refinance. And that’s because not all lenders have the same rules.

Check your VA IRRRL eligibility. Start hereFor instance, when undergoing a VA IRRRL, some mortgage lenders require credit and income approval even though the VA doesn’t. And interest rates can vary a lot from one company to the next. So depending on which lender you choose, you may or may not have access to the full suite of VA IRRRL benefits.

Not sure where to start? For more information on how to choose a VA IRRRL lender, check out our review of the Best VA Loan Lenders.

VA Streamline Refinance vs. VA cash-out refinance

Generally, homeowners are not allowed to get cash back with the VA IRRRL program. There’s just one exception: IRRRL users may get up to $6,000 cash-back if they plan to use it for energy-efficient home improvements.

Verify your VA refinance eligibility. Start hereFor everyone else, there is a VA cash-out refinance loan.

A cash-out refinance allows borrowers to refinance their existing loan at a lower rate while also taking cash out of the home’s equity. This replaces your existing mortgage rather than simply withdrawing cash like a home equity loan.

A qualified borrower can refinance up to 100% of the home’s value (100% LTV) using a VA loan in some cases. Another benefit is that the VA cash-out refinance can be used regardless of your current loan type, whether VA, USDA, FHA, or conventional.

Just like the VA Streamline Refinance loan, the home must be used as a principal dwelling by the owner. There is no set period of time that you must have owned your home, however, you must have enough equity to qualify for the loan.

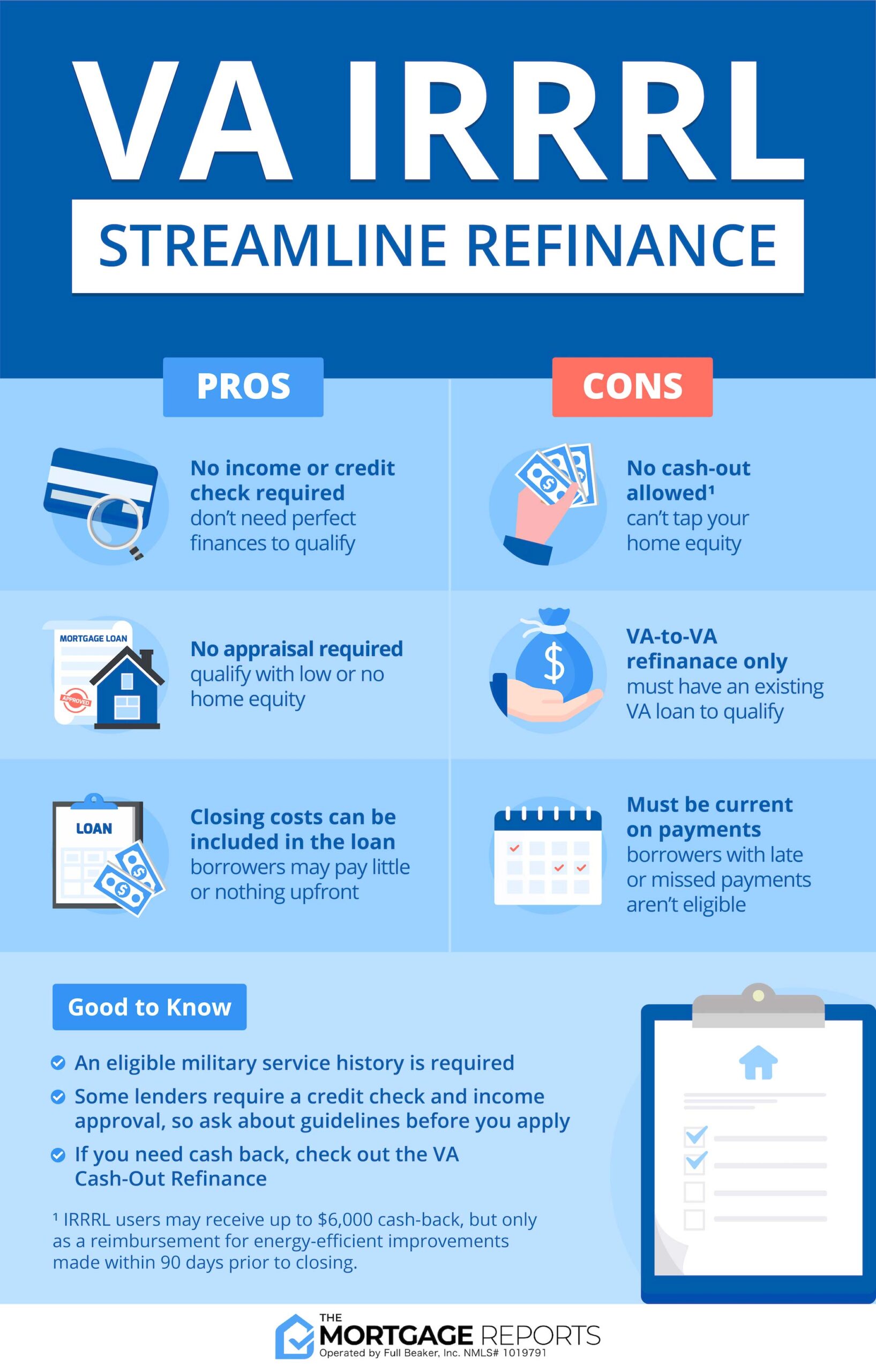

VA IRRRL program pros and cons

The VA IRRRL program offers both advantages and disadvantages for eligible veterans looking to refinance their existing VA-backed home loans.

Check your VA IRRRL eligibility. Start hereVA IRRRL pros

- Less documentation requirements — no credit report or COE

- No appraisal required

- Can apply to non-owner occupied properties

- Closing costs can be added to the loan, meaning no out-of-pocket costs

- May borrow up to $6,000 cash for energy-efficiency improvements

VA IRRRL cons

- Must already have a VA loan to be eligible

- A lower interest rate and monthly payment must occur (unless refinancing from an ARM to a fixed-rate loan)

- A 0.50% funding fee is added to new loan amount (though, it’s much less than the VA cash-out)

FAQs about VA IRRRL Rates

Check your VA IRRRL eligibility. Start hereCheck VA refinance rates today

The VA Streamline Refinance is one of the simplest and fastest mortgage products available for consumers today. Check rates with top-rated and VA-approved lenders for your refinance.

Time to make a move? Let us find the right mortgage for you