Key Takeaways

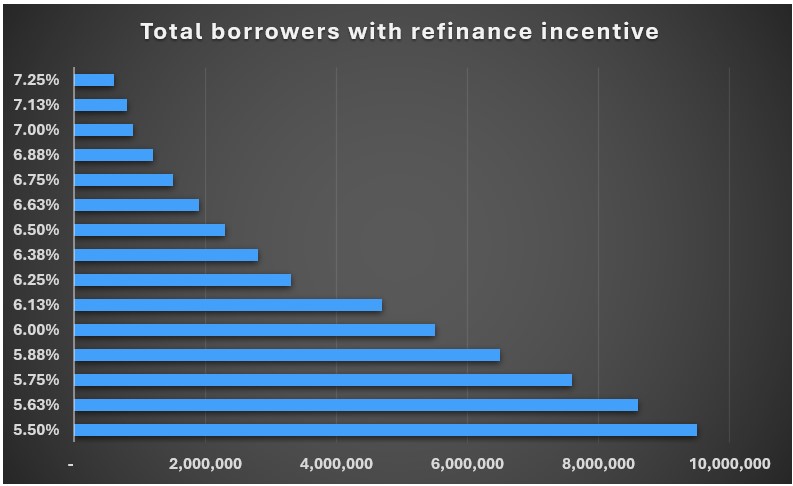

- If the average 30-year fixed rate mortgage hits 6%, it will unlock refinance incentives for 5.5 million borrowers.

- The total incentivized refinancers grow to 6.5 million at 5.88% and 7.6 million at 5.75%.

- Having the incentive to refinance typically means lowering your interest rate by at least 75 basis points (0.75%).

As interest rates fall, refinance incentives rise

Consensus industry forecasts for 2026 predicted gradually decreasing interest rates, driving a more welcoming borrowing environment compared to the last few years.

Early results have met expectations, with the average 30-year fixed rate mortgage dropping to 6.01% on Feb. 19 – the lowest point since September 2022 – according to Freddie Mac.

As mean interest rates hover near multi-year lows, refinancing opportunities expand. At 6% flat, nearly 5.5 million borrowers would be able to drop 75 basis points (0.75%) off their mortgage rate, according to Intercontinental Exchange’s February Mortgage Monitor Report. The cumulative incentivized refinancers then jumps to 6.5 million at 5.88%, 7.6 million at 5.75%, and 9.5 million at 5.5%.

Many of these incentivized borrowers originated their loans from 2022 to 2025. About 1.3 million of those homeowners have rates between 6.875% and 6.99%, with over 500,000 from 2025 alone. While every lender is different, there’s no official rule on how soon you can refinance your mortgage.

Total borrowers with refinance incentive

“Even small reductions toward 6% rates can significantly boost affordability, particularly for homeowners who could refinance into a lower rate and monthly payments,” said Andy Walden, head of mortgage and housing market research at Intercontinental Exchange. “When rates hit 6.04% on January 9, the number of homeowners in the money to refinance jumped by 20% and affordability hit its best level in four years. That said, affordability remains structurally challenged, with home prices still elevated relative to incomes and meaningful differences emerging across regions and borrower segments.”

When should you refinance your mortgage?

Whether you’re refinancing to drop your rate, eliminate private mortgage insurance, or convert your ARM to a fixed-rate mortgage – the time could be ripe to do it now.

The standard rule for when refinancing your mortgage puts you “in the money,” is when you can shave at least 75 basis points (0.75%) off your rate. Essentially, you’re finding the inflection point where you can lock in a rate low enough to both save money over the long-term and cover closing costs.

But everyone has different loan terms and goals, so even smaller reductions to your interest rate could make refinancing worthwhile. Need help figuring out how much rates need to fall before refinancing makes sense for you? Try our refinance calculator.

Refinancing will also require choosing and qualifying for the right refinancing loan type for your situation — which a good lender can help with.

Additionally, it’s important to note that every lender may offer slightly different rates. Finding your lowest rate will likely take a combination of knowing where to look and learning how to negotiate.

Video: When is it worth it to refinance your mortgage?

The bottom line

If you want to lower your interest rate and save on your monthly mortgage payment, refinancing can be the way. With the average rate sitting near 4-year lows, a growing number of borrowers find themselves with the financial incentive to refinance.

But one size does not fit all when it comes to refinancing your mortgage. Your ideal loan type will depend on your goals, timeline, and meeting the underwriting requirements.

Interest rates are notoriously volatile, so the opportunity window to lower your monthly payment can close suddenly and unexpectedly. If you’re ready to see what a refinance could mean for you, reach out to your lender today.

Time to make a move? Let us find the right mortgage for you