Key Takeaways

- USDA loans offer zero down and lower ongoing costs but are limited by location and income, making them best for eligible rural buyers.

- FHA loans are more flexible with credit and location but usually cost more over time due to higher mortgage insurance.

- The better loan depends on where you’re buying, your income, and whether lower upfront costs or broader eligibility matter more.

Choosing between a USDA loan vs FHA loan can shape everything from your down payment to where you can buy a home. USDA loans do not require a down payment, but they have specific location restrictions and income limits. FHA loans are more flexible with credit and available almost everywhere, though they usually cost more over time.

If you’re unsure which one fits your needs, this guide will help you understand the differences between USDA and FHA loans, so you can make a confident and informed decision.

In this article (Skip to…)

USDA vs FHA loans: A quick overview

USDA and FHA loans are both government-backed mortgage programs designed to make buying a home easier, but they are best suited for different types of buyers. If you’re purchasing in a rural area and meet income limits, USDA loans offer big advantages like no minimum down payment requirement and low mortgage insurance costs.

FHA loans, on the other hand, are available nationwide with no income restrictions and more flexible credit score requirements, though they typically require a down payment of 3.5% and come with higher mortgage insurance premiums. When comparing USDA loans vs FHA loans, the right fit depends on your location, income, and financial goals.

Check your home loan options. Start here

USDA vs FHA: Eligibility

Your eligibility is one of the biggest factors when choosing between a USDA home loan vs FHA loan. USDA loans are limited to single-family homes in approved rural areas, and you’ll need to meet income limits. FHA loans are more flexible. There are no restrictions based on income or location, and you can use them to purchase multi-unit homes, up to four units, as long as you live in one as your primary residence. Another important distinction is that FHA provides options for both fixed- and adjustable-rate mortgage loans, whereas USDA loans are exclusively offered as 30-year fixed-rate loans.

To see how FHA vs USDA loans compare side by side, check the comparison table below.

Check your home loan options. Start here| Criteria | FHA Loans | USDA Loans |

| Loan Requirements | Minimum credit score of 580 for 3.5% down payment Steady employment history Property must be primary residence | Must meet income eligibility Property must be in a USDA eligible area Property must be primary residence |

| Loan Limits | Vary by county, but typically up to $541,287 for single-family homes in most areas | No set loan limit, but the home must be modest in size for the area, and cannot have luxury features |

| Income Limits | None | Usually 115% of area median income (AMI) |

| Appraisal | Required Must meet HUD's minimum property standards | Required Must meet USDA's property and location requirements |

| Down Payment | Minimum of 3.5% with a credit score of 580 or higher 10% for credit scores between 500-579 | No down payment required |

| Mortgage Insurance | Upfront mortgage insurance premium (1.75% of the loan amount) Annual mortgage insurance premium (0.45% to 1.05% of the loan amount, paid monthly) | Upfront guarantee fee (1% of the loan amount) Annual fee (0.35% of the loan amount, paid monthly) |

| Interest Rates | Vary by lender, credit score, down payment, and other factors Typically lower for borrowers with good credit | Set by the lender, but can be as low as current market rates due to government backing |

| Closing Costs | Vary by lender, but can include appraisal fees, credit report fees, lender's origination fees, etc. Can be covered by seller or lender | Can include appraisal fees, credit report fees, lender's origination fees, etc. Can be rolled into the loan amount or paid by the seller |

Differences between USDA and FHA loans

When comparing USDA vs FHA loans, both programs strive to make homeownership more accessible, but they differ in meaningful ways. From how the loan is processed to what kind of properties qualify, understanding these details can help you decide which loan program fits your needs.

Check your home loan options. Start hereApplication process and underwriting

Both programs begin with preapproval, but USDA loans undergo two rounds of review: first by the lender and then by the U.S. Department of Agriculture. Applicants with a credit score of 640 or higher may qualify for streamlined, automated underwriting, while lower scores require manual review, which can extend the timeline.

FHA loans also involve lender review and typically close within 30 to 45 days. When weighing an FHA loan vs USDA loan, the extra underwriting step can make USDA loans slightly slower to close.

Loan limits

FHA loans have county-specific borrowing limits set by the Department of Housing and Urban Development (HUD). In 2026, the maximum FHA loan limit was set to $541,287 to over $1 million in high-cost areas. USDA loans don’t have formal loan limits. Instead, the maximum loan amount is based on your income, debts, and ability to repay.

Appraisal

An FHA appraisal ensures the property is worth the purchase price and meets HUD’s minimum standards for safety, soundness, and livability. USDA appraisals require those same checks, but also verify that the home is located in a USDA-eligible rural area and meets additional criteria, including that the property is modest in size, design, and cost.

Down payment

USDA loans do not require a down payment, making them especially attractive to buyers with limited financial resources. FHA loans require a minimum of 3.5% down with a credit score of 580 or higher, or 10% down if your score falls between 500 and 579.

Mortgage insurance

When choosing between USDA vs FHA loans, how each handles mortgage insurance matters. USDA loans include a 1% upfront guarantee fee and a 0.35% annual fee that lasts for the life of the loan unless you remove it by refinancing.

FHA loans include a 1.75% upfront mortgage insurance premium (MIP) and annual premiums between 0.15% and 0.75%, depending on the loan term. MIP continues until you repay the mortgage or refinance.

Interest rates

When comparing USDA vs FHA interest rates, both loans typically offer lower interest rates due to government backing. USDA interest rates tend to be slightly lower than FHA rates, although both are generally lower than conventional loan rates.

Closing costs

Closing costs, whether it’s USDA vs FHA, range from 2% to 6% of the loan amount. The USDA permits some or all of these expenses to be rolled into the loan if the home’s appraised value exceeds the purchase price. Both loan programs allow seller concessions to cover up to 6% of your closing costs.

Find the right mortgage for you. Start here

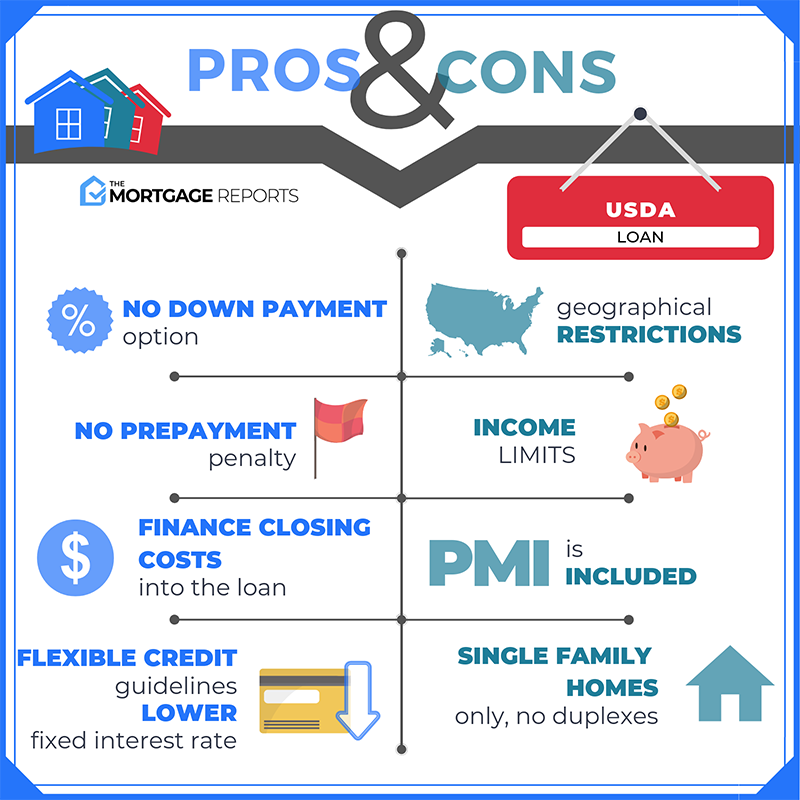

Pros and cons of USDA loans

Choosing between a USDA loan vs FHA often depends on where you’re buying, how much you earn, and what you can afford upfront. USDA loans offer zero-down financing in less populated areas, but they come with rules that won’t fit every buyer.

Check your home loan options. Start here

Pros

- No down payment required: USDA lets you finance the full purchase price, which can be a big help if you’re short on savings.

- Accessible for moderate-income borrowers: The program is designed to assist households that might struggle to qualify for traditional financing.

- Lower interest rates: Rates are typically more affordable than those on conventional loans.

Cons

- Location restrictions: Because USDA loans are part of a rural development initiative, they’re limited to homes in rural and suburban areas, not city centers.

- Property restrictions: Only available for single-family homes that you plan to live in full time. They can’t be used for investment properties or vacation homes.

- Income requirement: To qualify, your total household income has to stay below a set limit based on your family size and the area median income (AMI).

- Slower processing: Since USDA adds a second layer of loan approval, the process can take longer than an FHA or conventional loan.

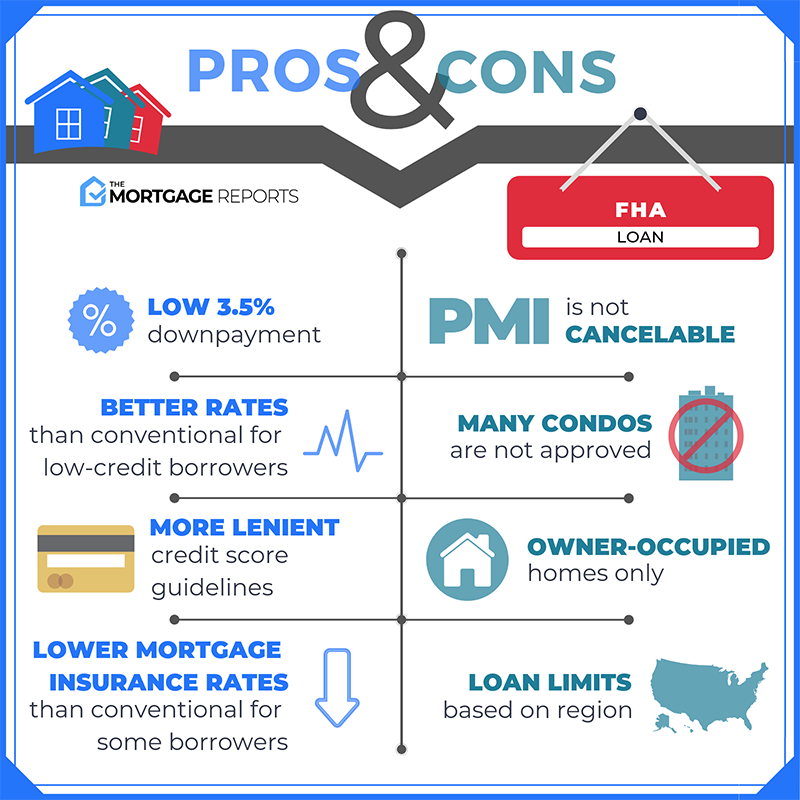

Pros and cons of FHA loans

FHA loans are popular low-down-payment loans with first-time home buyers who need flexible credit or income requirements. Although mortgage insurance costs may be higher, this program helps many to become homeowners who wouldn’t qualify elsewhere.

Check your home loan options. Start here

Pros

- No income limits or location restrictions.

- Lower credit score requirements than USDA or conventional loans.

- Greater flexibility in debt-to-income ratios (DTI), permitting larger loan amounts.

- Easier approval for borrowers with limited or nontraditional credit history.

Cons

- Higher mortgage insurance premiums than those of the USDA can increase your monthly payment.

- Mortgage insurance usually lasts for the duration of the loan unless you refinance.

- Can cost more in the long term if you have good credit and qualify for better mortgage rates with a conventional loan.

How to choose between USDA vs FHA loans

USDA and FHA loans are both backed by the federal government, with FHA loans insured by the Federal Housing Administration and USDA loans guaranteed by the U.S. Department of Agriculture. Neither agency lends money directly. Instead, they insure loans made by private mortgage lenders.

Check your FHA loan eligibility. Start hereSo, what does USDA vs FHA loans mean for you?

- It’s generally easier to qualify for a USDA or FHA loan compared to a conventional loan.

- Both loan programs charge upfront and annual mortgage insurance to help fund the loans.

- You can apply through most major mortgage lenders.

- Interest rates are competitive with other loan types.

- Both loan options are especially popular with first-time home buyers thanks to low upfront costs and flexible eligibility requirements.

The main drawback is mortgage insurance. With both programs, those premiums are added to your monthly mortgage payments for the life of the loan. To remove them, you would need to refinance into a different loan type later on.t of USDA or FHA mortgage insurance, you’d have to refinance your mortgage later on.

FAQ: USDA vs FHA loans

Compare USDA vs FHA mortgage rates

Thinking about buying a home? If you’re deciding between a USDA loan vs FHA loan or checking out VA loans, the best move is to compare. Understanding how each mortgage option works can help you find the best deal.

Ready to take the next step? Click below to compare rate quotes from top lenders and start your home search with confidence.

Time to make a move? Let us find the right mortgage for you