In this article:

While many people buy their new homes while simultaneously selling their old ones, that doesn’t work for everyone. If you’re a home seller who will be shopping and applying for a new mortgage in the near future, you’ll need to keep these documents at hand:

- The closing statement for the sale of your current house

- Proof of the transfer of your home sales proceeds to your bank or investment accounts

- Documentation supporting your income and assets

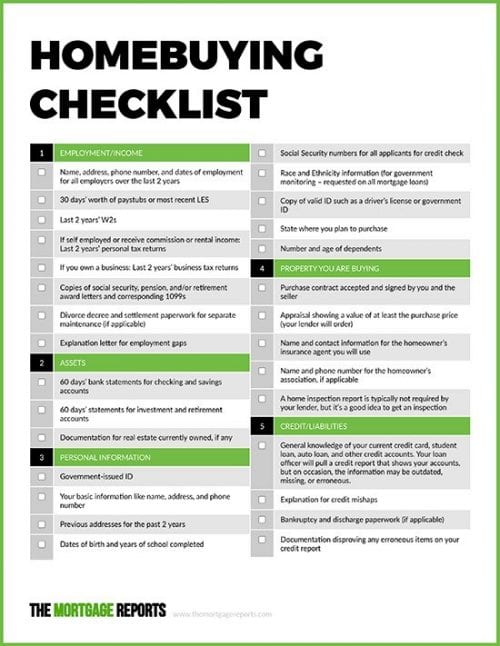

For a full breakdown of all paperwork, download our home buying checklist.

Verify your new rateCheck your credit, find a lender

It’s true that shopping and applying for a mortgage is not nearly as enjoyable as house hunting. But not shopping for a mortgage can cost you. A significant number of respondents to a Consumer Financial Protection Bureau (CFPB) survey admitted that they put off contacting a lender at all until after they had found a house to buy.

There are several reasons that this is a bad idea:

- Studies show that contacting more lenders means paying less for your mortgage

- You don’t know what you can afford until you see what rates and programs are available to you

- Home sellers and agents will not respect you or your offer if you are not pre-approved for your loan (or at least pre-qualified)

So how do you shop for a lender? Check your credit and your bank account. Then contact lenders online, by phone or in person.

It is helpful if you pull your credit report (for free at www.annualcreditreport.com, which is the government’s sponsored site). You can purchase your credit scores as well, which will help you give lenders an estimated credit score when you obtain mortgage quotes. They need that to estimate your rate.

Related: 5 things a truly great mortgage lender does

Lenders should be willing to provide you a Loan Estimate, worksheet or loan scenario, showing the rate and costs of a mortgage applicable to you. Be able to tell them how much you have for a down payment, provide an estimated credit score, and what you want to spend for a home. To provide a usable quote, lenders need this information.

They’ll also want your gross (before tax) income and monthly debt payments to pre-qualify you for a new home loan.

Mortgage pre-approval

You really shouldn’t begin shopping for a house until you know what you can spend. Mortgage pre-qualification typically involves answering a few questions about your income, monthly debts like auto loans and credit cards, and indicating how much money you have for a down payment and closing costs.

Related: Why every homebuyer needs a mortgage pre-approval before shopping

However, pre-qualification is not a commitment. The lender may not even check your credit, and won’t usually verify your income or bank balances either. Mortgage pre-approval (also called credit approval) is much better than pre-qualification, because it means that as long as the property you want meets the lender’s guidelines, you should be able to close.

Documents required for mortgage pre-approval

Mortgage lenders must, by law, make sure that you can afford your home loan payment as well as your other obligations. This is called the Ability to Repay (ATR) rule.

So you’ll have to come up with paperwork showing how much you earn, what you own, and what you owe. (Most of the time, your monthly accounts show up on your credit report.)

In most cases, lenders underwrite your application using automated underwriting software (AUS), which speeds the process considerably and tells you exactly what you need to supply to finalize your credit approval. You’ll get a list of documents the human underwriter needs to sign off on before you get your pre-approval letter.

Related: 5 nosy questions to expect from your mortgage lender

Here are some of the items you may have to supply:

Employment/income

- Pay stubs covering one month or most recent Leave and Earnings Statement from the military

- Last two years’ W2s

- If self-employed, a commissioned employee (25 percent or higher), an employee with unreimbursed business expenses or real estate income, you’ll supply at least your last two tax returns. For income that is highly variable or unusual, you may need additional years.

- If you own a business, you need at least two years’ business tax returns.

- Proof of receipt for Social Security, pension, public assistance (if using to qualify) or other income. This usually means an award letter, check stub or direct deposit.

- Divorce decree and settlement paperwork for separate maintenance (if applicable)

- Explanation letter for employment gaps

Assets

- Two months’ bank statements for checking and savings accounts

- Two months’ statements for investment and retirement accounts

- Information for real estate already owned (use, income, if it’s on the market, estimated value, mortgages)

- The closing statement from the recent sale of your home

- Proof of the transfer of the proceeds of the sale to your bank or investment account

Personal information

- Government-issued ID

- Previous addresses for the past two years

- Dates of birth and years of school completed

- Social Security numbers for all applicants

- Race and Ethnicity information (for government monitoring – requested on all mortgage loans)

- State and county in which you plan to purchase

- Number and age of dependents

The property

- Purchase contract accepted and signed by you and the seller (if you have one picked out)

- Name and contact information for the homeowner’s insurance agent you will use

- Name and phone number for the homeowner’s association, if applicable

Credit/liabilities

- Your loan officer will pull a credit report that shows your accounts, but on occasion, the information may be outdated, missing, or erroneous. That information is incorporated into your application, and you’re responsible for its review and confirmation.

- Explanation for credit mishaps

- Divorce decree and settlement paperwork for child or spousal support expenses (if applicable)

- Bankruptcy and discharge paperwork (if applicable)

- Documentation disproving any erroneous items on your credit report