Mortgage rate forecast for next week (July 21-25)

Mortgage rates ticked up for the second straight week.

The average 30-year fixed rate mortgage (FRM) rose to 6.75% on July 17 from 6.72% on July 10, according to Freddie Mac. However, it does mark 26 consecutive weeks below 7% for the average 30-year FRM.

“While overall affordability headwinds persist, rate stability coupled with moderately rising inventory may sway prospective buyers to act,” said Sam Khater, chief economist at Freddie Mac.

The latest weekly mortgage applications showed a seasonally adjusted 10% decrease for the seven days ending July 11, according to the Mortgage Bankers Association.

“Purchase applications remained sensitive to both the uncertain economic outlook and the volatility in rates and declined to the slowest pace since May,” said Joel Kan, deputy chief economist at the MBA. “Refinance applications also dipped because of higher rates, led by VA refinances partially reversing their previous week’s gain.”

Find your lowest mortgage rate. Start hereIn this article (Skip to...)

- Will rates go down in July?

- 90-day forecast

- Expert rate predictions

- Mortgage rate trends

- Rates by loan type

- Mortgage strategies for July

- Mortgage rates FAQ

Will mortgage rates go down in July?

“Frankly, 7% is historically average, so the new normal is just a return back to the old normal.”

-Mike Hills, vice president at Atlas Real Estate

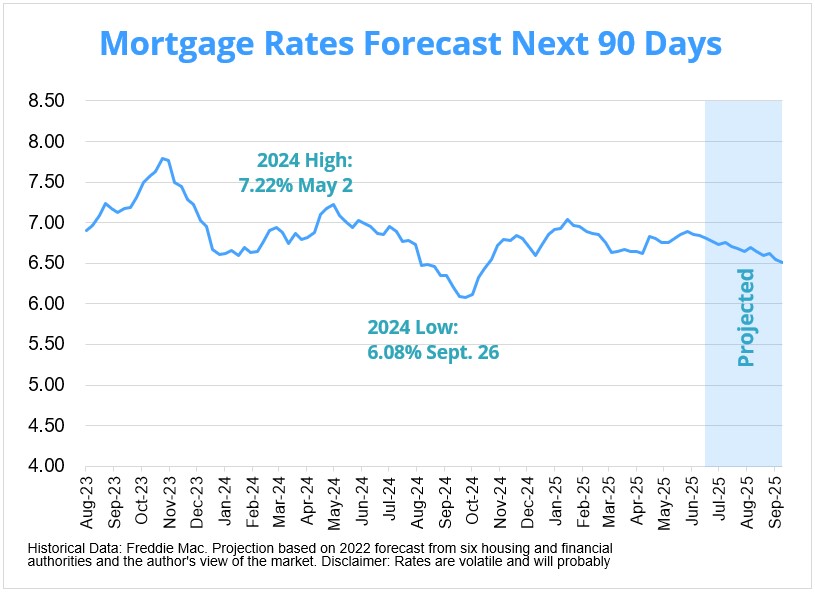

Mortgage rates fluctuated significantly in 2023, with the average 30-year fixed rate going as low as 6.09% and as high as 7.79%, according to Freddie Mac. That range narrowed in 2024, spreading from 6.08% to 7.22%.

Find your lowest mortgage rate. Start hereWith the economy probably heading into a recession, we may have already seen the peak of this rate cycle. But if inflation rises, mortgage rates could uptrend. Of course, interest rates are driven by many factors and notoriously volatile, so they could change direction any given week.

Experts from Realtor.com, First American, and others weigh in on whether 30-year mortgage rates will climb, fall, or level off in July.

Expert mortgage rate predictions for July

Jay Crowell, national retail division president at Cornerstone Home Lending

Prediction: Rates will moderate

“We saw that the Fed’s still in a cautious, wait-and-see stance. They’ve been leery about inflation, what’s going to happen with the trade tariff negotiations, and then the employment dynamics — which I don’t think have been as strong with some of the lookbacks having been revised. Policymakers are talking about maybe a quarter cut in July. But turmoil in the Middle East, in conjunction with tariffs, just leads to a lot of unknowns.”

Ralph DiBugnara, founder at Home Qualified

Prediction: Rates will moderate

“The interest rate market is a predicament going into July. Signs are pointing towards a cut, including the threat of war which historically equals a lower rate environment. But the Fed has held steady on let’s wait and see. Chairman Powell has commented that we don’t really know if tariffs will hurt inflation so he is pausing on any cuts right now. I do believe we are closer to lower mortgage rates than we were at the beginning of the year. Average rates for July should average around 6.875% for a 30-year fixed and 6.375% for 15-year fixed.”

Danielle Hale, chief economist at Realtor.com

Prediction: Rates will moderate

“July is a long month that offers the potential for a mortgage rate rollercoaster. Between the scheduled expiration of the reciprocal tariff pause early in the month and an FOMC meeting at month’s end, buyers and sellers could be in for ups and downs in mortgage rates even before factoring in closely watched updates on the labor market and inflation. The net of all of the ups and downs is likely to be that mortgage rates are little changed throughout July. I expect a generally downward trend for rates this year, but at a slow enough pace that it might not be noticeable in any given month.

“There are some factors that could usher in a new trend, however. If the labor market were to weaken, namely via slower job growth or higher unemployment, we could see mortgage rates move more quickly lower in anticipation of earlier Fed rate relief, perhaps as soon as July, though this is not my base case. I don’t expect a lower inflation reading to offer the same degree of reprieve given lingering concerns about the potential impact of tariffs on inflation, but a higher inflation reading could spark a more notable shift higher.”

Selma Hepp, chief economist at Cotality

Prediction: Rates will moderate

“While inflation has cooled and is closer to the Fed’s 2% target, overwhelming sentiment is that we are still in calm before the storm and the full impacts of tariffs are still to be felt. Similarly, the uncertain job market is keeping the Fed on the sidelines. In addition to the Fed’s two mandates competing against each other, the Fed’s job is complicated by remaining in the crosshairs of political pressures while trying to ensure it unequivocally maintains its much-needed independence.”

Mike Hills, VP of capital markets at Atlas Real Estate

Prediction: Rates will moderate

“I think it’s just going to stay mostly the same. May move up a little bit, may move down a little bit. Frankly, 7% is historically average, so the new normal is just a return back to the old normal. I think the days of 3% are probably long gone, likely forever. Those were artificially low. My humble opinion is trying to time the market is never going to work, because: you don’t know, I don’t know. Nobody knows what’s going on. The world is unpredictable, especially right now.”

Sam Royer, chief production officer at Salute Home Loans

Prediction: Rates will moderate

“I see them most likely staying pretty stagnant. I can’t imagine we’re going to have some major shift. I think the Fed’s holding on as tightly as they are because they’re trying to see how the tariffs will react.”

Sam Williamson, senior economist at First American

Prediction: Rates will moderate

“Mortgage rates are expected to remain in the mid-to-upper 6% range in July. Although rates have edged down slightly in recent weeks, persistent economic and policy uncertainty will likely prevent a meaningful decline. However, heightened geopolitical tensions could apply modest downward pressure, as investors shift toward safer assets like U.S. Treasuries.

“Several forces are keeping borrowing costs elevated. Inflation remains an ongoing concern, especially as major retailers announce price hikes in response to new tariffs. This has complicated the Federal Reserve’s ability to resume cutting interest rates. In June, the central bank held its benchmark rate steady for the fourth straight meeting while raising its inflation outlook through 2027. While two rate cuts are still projected this year, they are expected to come later than July. Meanwhile, concerns over rising federal debt have also pushed up yields on 10-year Treasury bonds, which mortgage rates closely track. If economic and policy conditions stabilize, a gradual decline could take shape later in the year. Until then, the higher-for-longer rate environment will likely remain.”

Mortgage interest rates forecast next 90 days

As inflation ran rampant in 2022, the Federal Reserve took action to bring it down and that led to the average 30-year fixed-rate mortgage spiking in 2023.

With inflation gradually cooling, the Fed made three rate cuts in 2024 (September, November, and December). Heading into 2025, many experts believed mortgage interest rates would gradually descend.

Find your lowest mortgage rate. Start hereOf course, rates could rise on any given week or if another global event causes widespread uncertainty in the economy.

Mortgage rate predictions for 2025

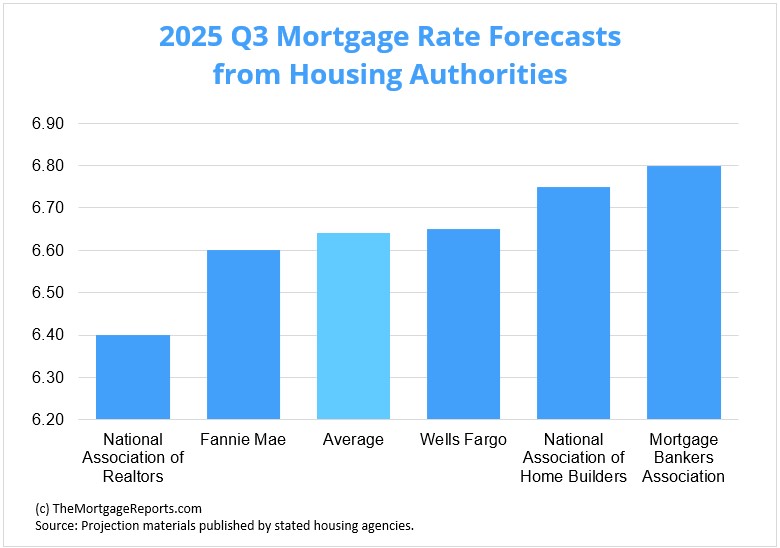

The 30-year fixed-rate mortgage averaged 6.75% as of July 17, according to Freddie Mac. Three of the five major housing authorities we looked at predict 2025’s third quarter average to finish below that.

National Association of Realtors sits at the low end of the group, projecting the average 30-year fixed interest rate to settle at 6.4% for Q3. Meanwhile, the Mortgage Bankers Association had the highest forecast of 6.8%.

| Housing Authority | 30-Year Mortgage Rate Forecast (Q3 2025) |

| National Association of Realtors | 6.40% |

| Fannie Mae | 6.60% |

| Wells Fargo | 6.65% |

| National Association of Home Builders | 6.75% |

| Mortgage Bankers Association | 6.80% |

| Average Prediction | 6.64% |

Current mortgage interest rate trends

Mortgage rates grew for the second week in a row.

The average 30-year fixed rate increased to 6.75% on July 17 from 6.72% on July 10. The average 15-year fixed mortgage rate similarly rose to 5.92% from 5.86%.

| Month | Average 30-Year Fixed Rate |

| June 2024 | 6.92% |

| July 2024 | 6.85% |

| August 2024 | 6.50% |

| September 2024 | 6.18% |

| October 2024 | 6.43% |

| November 2024 | 6.81% |

| December 2024 | 6.72% |

| January 2025 | 6.96% |

| February 2025 | 6.84% |

| March 2025 | 6.65% |

| April 2025 | 6.73% |

| May 2025 | 6.82% |

| June 2025 | 6.82% |

Source: Freddie Mac

After hitting record-low territory in 2020 and 2021, mortgage rates climbed to a 23-year high in 2023 before descending somewhat in 2024. Many experts and industry authorities believe they will follow a downward trajectory into 2025. Whatever happens, interest rates are still below historical averages.

Dating back to April 1971, the fixed 30-year interest rate averaged around 7.8%, according to Freddie Mac. So if you haven’t locked a rate yet, don’t lose too much sleep over it. You can still get a good deal, historically speaking — especially if you’re a borrower with strong credit.

Just make sure you shop around to find the best lender and lowest rate for your unique situation.

Mortgage rate trends by loan type

Many mortgage shoppers don’t realize there are different types of rates in today’s mortgage market. But this knowledge can help home buyers and refinancing households find the best value for their situation.

Find your lowest mortgage rate. Start hereWhich mortgage loan is best?

The best mortgage for you depends on your financial situation and your goals.

For instance, if you want to buy a high-priced home and you have great credit, a jumbo loan is your best bet. Jumbo mortgages allow loan amounts above conforming loan limits, which max out at $ in most parts of the U.S.

On the other hand, if you’re a veteran or service member, a VA loan is almost always the right choice. VA loans are backed by the U.S. Department of Veterans Affairs. They provide ultra-low rates and never charge private mortgage insurance (PMI). But you need an eligible service history to qualify.

Conforming loans and FHA loans (those backed by the Federal Housing Administration) are great low-down-payment options.

Conforming loans allow as little as 3% down with FICO scores starting at 620. FHA loans are even more lenient about credit; home buyers can often qualify with a score of 580 or higher, and a less-than-perfect credit history might not disqualify you.

Finally, consider a USDA loan if you want to buy or refinance real estate in a rural area. USDA loans have below-market rates — similar to VA — and reduced mortgage insurance costs. The catch? You need to live in a ‘rural’ area and have moderate or low income to be USDA-eligible.

Mortgage rate strategies for July 2025

Mortgage rates displayed their famous volatility throughout 2024. Fed cuts in September, November, and December, with the potential for more in 2025 provide optimism for descending rates.

Previously, the central bank held off on a rate hike at eight consecutive meetings, preferring to see if the economy would keep cooling organically. They finally deemed inflation’s downtrend as organic and made its first cuts since 2020.

Find your lowest mortgage rate. Start hereHowever, the Trump Administration’s upward wealth consolidation and ongoing inflation battles forced the Fed to hold in January, March, May, and June. As always, the committee said it would adjust its policies as necessary — which could mean additional cuts or possibly none at all.

Here are just a few strategies to keep in mind if you’re mortgage shopping in the coming months.

Be ready to move quickly

Indecision can lead to failure or missed opportunities. That holds true in home buying as well.

Although the housing market is becoming more balanced than the recent past, it still favors sellers. Prospective borrowers should take the lessons learned from the last few years and apply them now even though conditions are less extreme.

“Taking too long to decide to make an offer can lead to paying more for the home at best and at worst to losing out on it entirely. Buyers should get pre-approved (not pre-qualified) for their mortgage, so that the seller has some certainty about the deal closing. And be ready to close quickly — a long escrow period will put you at a disadvantage.

And it’s definitely not a bad idea to work with a real estate agent who has access to “coming soon” properties, which can give a buyer a little bit of a head start competing for the limited number of homes available,” said Rick Sharga.

If mortgage rates continue on a downward trajectory, more and more buyers will likely enter the market after being priced out on the sidelines. Being decisive (and prepared) should only play to your advantage.

Shopping around isn’t only for the holidays

Since interest rates can vary drastically from day to day and from lender to lender, failing to shop around likely leads to money lost.

Lenders charge different rates for different levels of credit scores. And while there are ways to negotiate a lower mortgage rate, the easiest is to get multiple quotes from multiple lenders and leverage them against each other.

“For potential home buyers, it’s important to get quotes from multiple lenders for a mortgage, as rates can vary dramatically, especially during such a volatile period,” said Odeta Kushi.

As the mortgage market slows due to lessened demand, lenders will be more eager for business. While missing out on the rock-bottom rates of 2020 and 2021 may sting, there’s always a way to use the market to your advantage.

How to shop for interest rates

Rate shopping doesn’t just mean looking at the lowest rates advertised online because those aren’t available to everyone. Typically, those are offered to borrowers with great credit who can put a down payment of 20% or more.

The rate lenders actually offer depends on:

- Your credit score and credit history

- Your personal finances

- Your down payment (if buying a home)

- Your home equity (if refinancing)

- Your loan-to-value ratio (LTV)

- Your debt-to-income ratio (DTI)

To figure out what rate a lender can offer you based on those factors, you have to fill out a loan application. Lenders will check your credit and verify your income and debts, then give you a ‘real’ rate quote based on your financial situation.

You should get three to five of these quotes at a minimum, then compare them to find the best offer. Look for the lowest rate, but also pay attention to your annual percentage rate (APR), estimated closing costs, and ‘discount points’ — extra fees charged upfront to lower your rate.

This might sound like a lot of work. But you can shop for mortgage rates in under a day if you put your mind to it. And shaving just a few basis points off your rate can save you thousands.

Compare mortgage and refinance rates. Start here

Mortgage interest rate FAQ

Current mortgage rates are averaging 6.75% for a 30-year fixed-rate loan and 5.92% for a 15-year fixed-rate loan, according to Freddie Mac’s latest weekly rate survey. Your individual rate could be higher or lower than the average depending on your credit score, down payment, and the lender you choose to work with, among other factors.

Mortgage rates could decrease next week (July 21-25, 2025) if the mortgage market takes a cautious approach to a possible recession. However, rates could rise if lenders account for the Federal Reserve taking measures to counteract inflation or if a global event brings economic uncertainty.

If inflation continues to dissipate and the economy cools or goes into a recession, it’s likely mortgage rates will decrease in 2025. Although, it’s important to remember that interest rates are notoriously volatile and are driven by many factors, so they can rise during any given week.

Mortgage rates may rise in 2025. High inflation, strong demand in the housing market, and policy changes by the Federal Reserve in 2022 and 2023 all pushed rates higher. However, if the U.S. does indeed enter a recession, mortgage rates could come down.

Freddie Mac is now citing average 30-year rates in the 7% range. If you can find a rate in the 5s or 6s, you’re in a very good position. Remember that rates vary a lot by borrower. Those with perfect credit and large down payments may get below-average interest rates, while poor-credit borrowers and those with non-QM loans could see much higher rates. You’ll need to get pre-approved for a mortgage to know your exact rate.

For the most part, industry experts do not expect the housing market to crash in 2025. Yes, home prices are over-inflated. But many of the risk factors that led to the 2008 crash are not present in today’s market. Low inventory and massive buyer demand should keep the market propped up. Plus, mortgage lending practices are much safer than they used to be. That means there’s not a subprime mortgage crisis waiting in the wings.

At the time of this writing, the lowest 30-year mortgage rate ever was 2.65%. That’s according to Freddie Mac’s Primary Mortgage Market Survey, the most widely used benchmark for current mortgage interest rates.

Locking your rate is a personal decision. You should do what’s right for your situation rather than trying to time the market. If you’re buying a home, the right time to lock a rate is after you’ve secured a purchase agreement and shopped for your best mortgage deal. If you’re refinancing, you should make sure you compare offers from at least three to five lenders before locking a rate. That said, rates are rising. So the sooner you can lock in today’s market, the better.

That depends on your situation. It’s a good time to refinance if your current mortgage rate is above market rates and you could lower your monthly mortgage payment. It might also be good to refinance if you can switch from an adjustable-rate mortgage to a low fixed-rate mortgage; refinance to get rid of FHA mortgage insurance; or switch to a short-term 10- or 15-year mortgage to pay off your loan early.

It’s often worth refinancing for 1 percentage point, as this can yield significant savings on your mortgage payments and total interest payments. Just make sure your refinance savings justify your closing costs. You can use a mortgage calculator or speak with a loan officer to crunch the numbers.

Start by choosing a list of three to five mortgage lenders that you’re interested in. Look for lenders with low advertised rates, great customer service scores, and recommendations from friends, family, or a real estate agent. Then get pre-approved by those lenders to see what rates and fees they can offer you. Compare your offers (Loan Estimates) to find the best overall deal for the loan type you want.

What are today’s mortgage rates?

Mortgage rates are rising, but borrowers can almost always find a better deal by shopping around. Connect with a mortgage lender to find out exactly what rate you qualify for.

Time to make a move? Let us find the right mortgage for you1Today's mortgage rates are based on a daily survey of select lending partners of The Mortgage Reports. Interest rates shown here assume a credit score of 740. See our full loan assumptions here.

Selected sources:

- https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- http://www.freddiemac.com/research/datasets/refinance-stats/index.page