Thinking about refinancing a mobile home? It’s a smart move if you want to lower your monthly payments, get a better interest rate, or tap into your home’s value. But mobile home refinancing comes with unique rules. Your mobile refinancing options depend on the home’s age, size, classification, and whether it’s permanently installed. Here’s what to know.

Today’s “mobile homes” are really manufactured homes. This is true for any mobile or manufactured home built after June 15, 1976. The terms “mobile home” and “manufactured home” are often used interchangeably when referring to today’s manufactured home financing. We use both terms in this article.

Can you refinance a mobile home?

Yes, you can refinance a mobile or manufactured home, but the process differs from refinancing a traditional home. Mobile homes are usually considered personal property unless they’re attached to a permanent foundation and you own the land. This distinction plays a big role in both your eligibility for refinancing and the types of loans available to you.

Requirements to refinance mobile home loans

Mobile home refinancing can be complex, but understanding the requirements will help simplify the process. The first step is to determine whether your home needs to meet certain guidelines to qualify for financing.

To refinance mobile home loans, the property must be:

On land that you own (and that is not located in a mobile home park)

Affixed to a permanent foundation that conforms to HUD standards

Titled as real property (real estate)

Built after June 15, 1976

Without axles, wheels, or a towing hitch

A minimum of 12 feet wide and 400 square feet in size

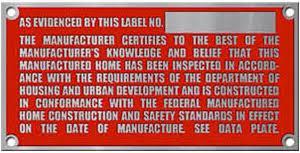

Your mobile home must also comply with building standards set by the U.S. Department of Housing and Urban Development (HUD). Look for a HUD tag (metal plate certification label) outside and a data plate (paper label) inside.

To refinance mobile home mortgages or manufactured home loans, you’ll need this HUD label, which should be found on the outside of the dwelling.

To get approved for a mobile home refinance, borrowers must also meet certain financial criteria.

The required minimum credit score typically ranges from 580 to 620 for most loan types.

Additionally, a qualifying debt-to-income ratio (DTI) is necessary. Although the acceptable DTI can vary, aiming for a ratio lower than 43% is generally a good benchmark.

Types of mobile home refinance loans

There are several ways to refinance a mobile home, depending on your financial goals and the type of property you own. To be eligible, most mobile home refinance loans require that the home be classified as real property, permanently attached to land you own, and meet certain condition and size standards.

“Manufactured homes typically have slightly higher rates regardless of other qualifying factors.”

— Jon Meyer, mortgage loan expert.

Below is a breakdown of the main mobile home refinancing options available and what you’ll need to qualify.

Loan type

Credit score minimum

Maximum LTV (%)

Maximum DTI (%)

Unique features or requirements

Conventional loan

620

80

43 to 50

Must be on permanent foundation; real property status

Cash-out refinance

620-640

75

43 to 50

Usually, higher interest rates

FHA refinance loan

580

97.75

43 to 50

Upfront and annual mortgage insurance

FHA Streamline Refinance

No minimum

NA

No DTI Check

Must already have an FHA loan. No appraisal required

FHA Title 1

No minimum

NA

45

Property can rest on leased land. No appraisal needed

VA refinance loan

No minimum

90

41 to 50

Must be a veteran. No mortgage insurance

VA IRRRL

No minimum

NA

No DTI Check

Must already have a VA loan; no appraisal required

USDA refinance loan

640

100

41 to 50

Rural areas only. Income limitations

USDA Streamline Refinance

No minimum

100

No DTI Check

Must already have a USDA loan. Simplified paperwork

Mortgage lenders may have varying credit score minimums, debt-to-income ratios, and maximum loan-to-value percentages based on their risk assessment criteria and specialization.

Conventional loans

Conventional loans are a good option for borrowers with good credit and at least 5% home equity. These loans usually require a minimum credit score of 620 and offer both fixed-rate and adjustable-rate terms. If you’re seeking a cash-out refinance, Fannie Mae allows it for multi-width manufactured homes, but not for single-wide units. This is an excellent way to tap into your home’s value and use the cash for renovations or other needs.

FHA loans

The Federal Housing Administration offers FHA loans to both first-time home buyers and manufactured homeowners. To refinance a mobile home with an FHA loan, you’ll need a credit score of at least 580. Loan terms typically range from 20 to 25 years for both mobile and manufactured homes, and the home must meet HUD standards. FHA refinance options include:

FHA Title 1 loansare exclusively for home improvements. You can borrow up to $25,090 for homes on owned land and up to $7,500 for manufactured homes on leased land.

FHA Streamline Refinance is designed for existing FHA borrowers. This option offers a faster and less expensive way to refinance, with limited documentation and no appraisal required in many cases.

VA loans

For veterans, active-duty service members, and eligible surviving spouses, VA loans offer competitive interest rates with no down payment needed. Refinancing a mobile home with a VA loan usually requires a credit score of 620 or above. The maximum loan term is 25 years, and the property must be your primary residence.

If you already have a VA loan, the Interest Rate Reduction Refinance Loan (IRRRL), also known as the VA Streamline Refinance, allows for quick refinancing with lower interest rates and minimal paperwork.

USDA loans

If you reside in a qualifying rural area, USDA loans offer an alternative way to refinance mobile homes, but only under certain conditions. The home must be less than one year old, permanently installed, and located in an area approved by the USDA. Income limits might also apply.

Additionally, existing USDA loan holders can use a USDA Streamline Refinance, which offers lower credit requirements and a simplified application process.

Mobile home refinancing rates are usually a bit higher than those for traditional mortgages. What you qualify for depends on a few key factors:

A score over 700 and a debt-to-income ratio under 43% typically unlock the best rates.

Newer homes that are permanently affixed and classified as real property tend to qualify for better rates than older or personal property units.

Rates vary widely between conventional, FHA, VA, and USDA loans, and each lender sets their own terms.

As with any mortgage refinance, shop around. Compare offers from at least 3–5 lenders to find the best mobile home refinance rates available.

How to refinance mobile home loans

Refinancing a mobile home takes a few extra steps, like saving pay stubs and making sure your home is classified as real property. Here’s what the mobile home refinancing process usually looks like.

1. Find out what kind of mobile home you have

Today’s “mobile homes” are often called “manufactured homes” or “modular homes.” In fact, the terms are often used interchangeably in the industry. But there are some key differences, and they can affect financing and refinancing options for your mobile home.

Raymond Brousseau, partner with River City Mortgage, explains:

Mobile home: A mobile home is a residence that has or used to have axles and wheels. It’s titled as a motor vehicle. “True” mobile homes were built prior to June 15, 1976.

Manufactured home: A manufactured home is constructed entirely in a factory. It’s brought to the home site in one or more pieces. These come in both single-wide and double-wide varieties.

Modular home: A modular home is mostly constructed in a factory, but it’s brought to the home site in multiple pieces to finish construction. Once built, you can’t move a modular home. These also come in both single-wide and double-wide homes.

2. Determine if your home is real property

If you have it, look at the title to determine if your mobile home is classified as real property. Alternatively, contact your county assessor’s office. This is frequently possible online. As a rule of thumb, you cannot refinance mobile home loans when the property is technically “mobile.” But if it’s fixed to a foundation and considered real property, it can likely be financed or refinanced.

“If your home is fixed to its foundation and considered real property, it can likely be financed or refinanced with a mortgage loan.”

— Raymond Brousseau, River City Mortgage

Technically, any manufactured home built prior to June 15, 1976, is considered a bona fide mobile home. Those built after that date are considered manufactured homes.

Because they’re titled as real property, you can refinance mobile home loans when the dwellings are permanently affixed to a foundation. But mobile homes not permanently affixed to a foundation are usually titled and financed as “personal property” and cannot be refinanced with a mortgage loan.

3. Convert personal property to real property

Before you can refinance mobile home loans, dwellings must be converted to real property when they’re currently titled as personal property.

Mobile or manufactured homes that don’t meet the requirements listed above are considered personal property. So you might need to make some changes to the home before you can be eligible for a mortgage refinance.

Converting your mobile home title into real property requires:

Certificate of title

Certificate of origin

Affidavit of affixture (demonstrates the home is permanently attached to land you own)

Additionally, according to Brousseau, “you’ll require a foundation certification from a qualified structural engineer. Plus, the home needs sufficient homeowners insurance coverage to qualify for a mortgage loan.” This process is easier today in some states, including Virginia, Maryland, Tennessee, Nebraska, Illinois, Missouri, Alaska, Iowa, and North Dakota.

4. Check with a mortgage lender

If you do qualify for a refinance, it’s important to consider the different types of refinancing options, such as a cash-out refinance or a streamline refinance, to determine which one is best for your financial situation.

Before you decide, you should also look at the terms of a new loan. This includes the interest rate, the monthly payment, and any fees that come with the refinance. You should also think about how long you plan to live in your home and if the savings from refinancing will be worth the costs.

5. Compare mobile home refinance rates and terms

To refinance mobile home loans, request quotes from multiple lenders and compare interest rates, fees, and terms to find the best offer. Be sure to specify that you’re refinancing a manufactured home, as this can affect the rates you’re quoted.

After choosing a lender, maintain regular communication with your loan officer and have all necessary documents about your manufactured home readily available, especially for the appraiser. If the goal of your refinance is to transition your manufactured home to real property, be sure to lock in your mortgage rate for a duration that accounts for the time needed to affix your home to its permanent foundation.

Pros and cons of mobile home refinancing

Refinancing mobile homes can help lower interest rates, reduce monthly payments, or get cash for renovations. But it’s not always the right move. Before you refinance a manufactured home, weigh the potential savings against the costs and long-term impact on your budget.

Lower monthly payments: Getting a lower interest rate or stretching out your loan term can lower your monthly payments, keeping more cash in your pocket.

Access to quick cash: A cash-out refinance allows you to use your home equity to pay for urgent expenses, such as medical bills or student loan debt.

Potentially better interest rates: If you got your original loan when interest rates were high, refinancing now could save you money over the life of the loan.

Mobile home refinancing cons

Closing costs: Refinancing involves closing costs, and if you’re changing your title status, there are additional fees to consider.

Legal fees: Depending on your situation, you might need a real estate lawyer or a title company, which adds to your costs.

Property tax implications: Changing your mobile home’s status from personal to real property may increase your property taxes.

Foundation costs: Some refinancing terms require placing your mobile home on a permanent foundation, which can be a significant expense.

Mobile home refinancing can strengthen your finances—or add new debt if you’re not careful. Take your time, look at your current mortgage and weigh your long-term goals.

Alternative mobile home refinancing option

If your mobile home isn’t classified as real property, you may not qualify for a traditional mortgage refinance. In that case, chattel loan refinancing is usually the only alternative.

Chattel loan refinance

The Consumer Financial Protection Bureau (CFPB) reports that most mobile home loans are chattel loans. A chattel loan refinance replaces your current personal property loan with a new one. Lenders often use this option when the home sits on leased land, the home lacks a permanent foundation, or the title still works like a vehicle title. Expect higher rates and shorter terms than a traditional mortgage, and plan to compare multiple specialty lenders.

“If you rent the site your mobile home is on, often the only financing option is a personal property loan,” according to Raymond Brousseau with River City Mortgage.

Refinance into a mortgage after you convert to real property

Some borrowers follow a two-step process. First, they move the home onto a qualifying permanent foundation, verify HUD compliance, and retitle the home as real property (often using an affidavit of affixture and foundation certification). Then, they refinance into a conventional, FHA, VA, or USDA mortgage if they meet program requirements. This approach can lead to better terms, but you must cover the costs of the conversion work and related paperwork.

Unsecured personal loan

A personal loan can be helpful when you need funds but can’t use your home as collateral in a mortgage refinance. Lenders base approval on your credit, income, and debt load. This option can move quickly and avoid title or foundation requirements, but the interest rate is usually higher than a mortgage rate.

Portfolio or specialty manufactured-home loans

Some credit unions and local banks provide manufactured-home loans. These “portfolio” programs can accept properties that don’t meet typical mortgage standards, but each lender has its own property rules, minimum loan amounts, and pricing. Ask upfront how the lender classifies the home and what title or foundation documents they require.

Refinancing options for mobile homes not permanently affixed to a permanent foundation (considered personal property or chattel) are limited. However, some lenders offer chattel loans designed specifically for mobile homes without a permanent foundation.

Mobile home refinancing costs can include origination fees, appraisal fees, credit report fees, title search and insurance fees, recording fees, and other closing costs. Consider these costs when deciding on manufactured home refinancing.

Some loan programs, such as FHA, USDA, or VA loans, may have more lenient credit history requirements for borrowers with lower credit scores. Consider improving your credit score before applying for refinancing.

Not all lenders offer manufactured home refinancing. You may need to search for a lender that works with you, possibly through a mortgage broker. Lenders also enforce minimum loan amounts, which could restrict financing options for lower-priced mobile or manufactured homes.

Yes, refinancing a mobile home mortgage can be worth it if you qualify for a lower interest rate or better loan terms. Homeowners can potentially save on monthly mortgage payments, reduce overall loan costs, or tap into their home equity for financial needs.

Check your mobile home refinancing options

Before refinancing, compare your potential monthly savings to how long you plan to keep your manufactured home. Lower mobile home refinance rates can reduce your payments, but the savings only make sense if you stay long enough to cover closing costs. If you’re unsure about your eligibility, contact a lender experienced in mobile home refinancing. A loan officer can examine your credit, income, and property details to advise which loan options suit you and how much you could save.

Ryan Tronier is a financial writer and mortgage lending expert. His work is published on NBC, ABC, USATODAY, Yahoo Finance, MSN Money, and more. Ryan is the former managing editor of the finance website Sapling and the former personal finance editor at Slickdeals.

Ryan Tronier is a financial writer and mortgage lending expert. His work is published on NBC, ABC, USATODAY, Yahoo Finance, MSN Money, and more. Ryan is the former managing editor of the finance website Sapling and the former personal finance editor at Slickdeals.

Aleksandra is an editor, finance writer, and licensed Realtor with deep roots in the mortgage and real estate world. Based in Arizona, she brings over a decade of experience helping consumers navigate their financial journeys with confidence.