Should I buy a new or pre-owned home?

Buying a new home is the dream for many. Who wouldn’t want all-new appliances, fixtures, plumbing, floors, windows, finishes and other components? You wouldn’t have to worry about updating or repairing.

But not everyone thinks spanking new offers the charm of an existing home in an established neighborhood. And the economics of homebuying may favor buying “used.”

Verify your new rateCosts of new versus existing homes

The truth is that new construction is costly these days. And homebuilding has not kept pace with new buyers. With a low supply and high demand, a new home may not be your best option.

New construction: Should I do a long-term mortgage rate lock?

Instead, an existing home may be a better bet. There’s a greater supply of pre-owned houses to choose from. They’re more likely to fit your budget, too, especially if you’re a first-time buyer.

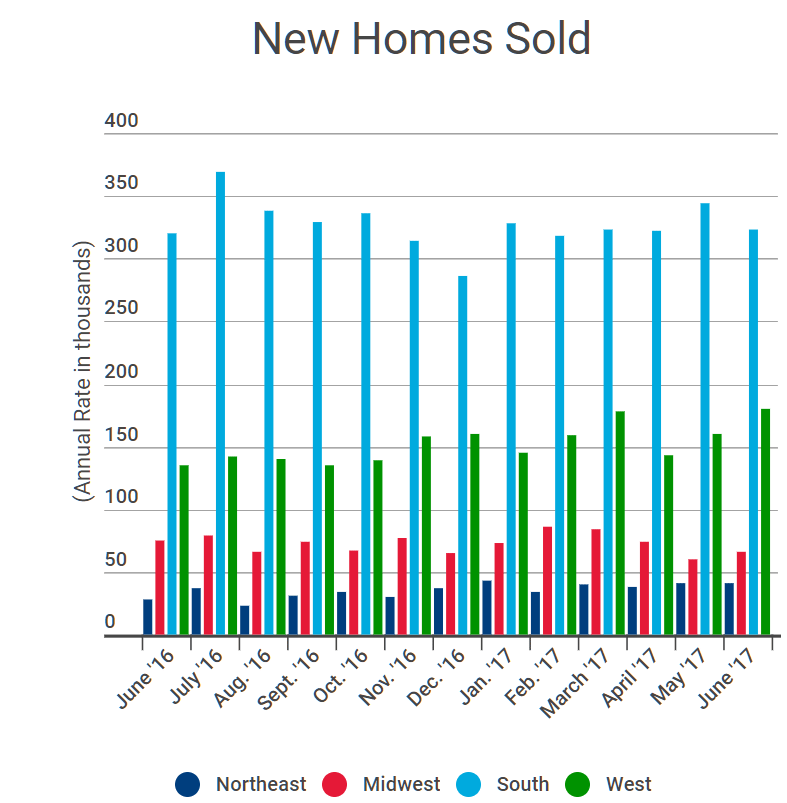

New data show that new construction is slightly on the rise – but so are prices. Learn the facts and compare new and resale homes carefully. Chances are you’ll land a better deal by picking the latter.

New facts on new homes

A recent report by Redfin offers some interesting findings about new construction:

- Single-family housing starts are up nine percent from last year.

- One in eight homes for sale today are newly-built. Five years ago, it was only one in 13.

- Most new homes are not affordable for first-timers. In September, newly-built homes sold for an average premium of $87,000 above the price for existing homes.

- A single-family home costs $240,000 to build today, on average. That’s the highest cost on record.

- High-end homes often cost builders nearly as much as affordable starter homes. But they sell for more, so they are much more lucrative for builders. This is why many builders avoid crafting lower-priced starter homes.

New home building tapered off over the last decade. But now, “we are finally seeing a slow steady increase in single-family housing starts,” said Redfin chief economist Nela Richardson in a prepared statement.

Complete guide to building a house of your own

Still, “High building costs are limiting the construction of homes that today’s buyers can afford,” she added. “This is why, even in the midst of extreme inventory shortages for existing homes, new homes are sitting on the market instead of selling.”

Reading between the numbers

In fact, only 15 percent of recent buyers are purchasing new homes today, per fresh data from the National Association of Realtors (NAR). That’s down from 28 percent measured in 2003 and near last year’s all-time low (14 percent).

“This can vary by region. Only five percent of buyers in the Northeast were able to purchase new construction in 2017,” says Jessica Lautz, the NAR’s managing director of survey research and communications. “Compare that to 19 percent in the South.”

The major takeaway here?

“There may have been slight increases lately. But the pace of new construction is still not where we’d like it to be,” Lautz says. “And new homes continue to remain out of reach for many first-time and single buyers.”

What’s holding builders back

Robert Dietz, chief economist at the National Association of Home Builders (NAHB), spoke at a recent National Association of Realtors conference. There, he said the high cost of building homes is having an effect on supply.

“Over the last five years, the total effect of building codes, land use, environmental laws and other rules have caused regulatory costs to rise 29 percent,” said Dietz.

Dietz gave other reasons why builders aren’t crafting more new homes:

- An aging workforce has led to a shortage of construction workers.

- Fewer lots are available.

- Building materials and land costs continue to rise.

- Builders are finding it hard to get construction loans.

“Depending on the region, raw land can be a challenge,” says Tamara Dorris, real estate professor at American River College. “In many developed metro areas, for example, any new developments need to be miles away from downtown. With many first-time buyers working downtown, this increases commute time. And with young families needing daycare, the downside increases.”

Thinking outside the big box

Yet, there are signs of hope. First, builders feel more optimistic lately. The NAHB’s builder sentiment index climbed to 70 in November, the highest score since March. Also, Dietz noted a shift toward building more townhomes and smaller homes. These can be more affordable for first-timers.

Loans for condos and townhomes

“A townhome could prove more affordable than a detached home. It can also involve less upkeep. If you can find a new townhome, this could be a decent strategy for a first-time buyer. You could build equity, sell it later and buy a detached or new home of your choice,” Lautz adds.

“But the downside of townhomes, as well as condos, are homeowners association dues. These can be steep. They also may lack yards and garages. Many first-timers value these features,” Dorris says.

Strategies for success

For these and other reasons, a pre-owned single-family home remains a popular choice.

“We polled recent buyers about why they bought a previously owned home versus a new home. The top reason they opted for the former was better price and better overall value. They also liked the charm and character that an existing home offers,” says Lautz.

To boost your odds of finding a new or resale home at the right price, try these tips:

- Consult with a mortgage expert. Learn what kind of financing you qualify for, which can narrow down your choices. “Get preapproved with a good lender. Then you can hunt for homes that work with your loan,” says Dorris.

- Put away as much as you can toward the down payment. “Be prepared to make financial sacrifices, like cutting back on entertainment and nonessential goods,” says Lautz. “Think about working a second job if you have to.”

- Enlist a skilled real estate agent. “Find an agent who knows your area of interest,” Dorris adds. “And trust your agent when it comes to making the best offer with respect to terms and concessions.”

The other way to reduce your housing costs is to find the right mortgage.

What are today’s mortgage rates?

Today’ mortgage rates are very stable and not moving up or down too much. This should remove some of the pressure on buyers right now.

Time to make a move? Let us find the right mortgage for you