What Is The Average Homebuyer Tenure In The US?

We all know people who have lived in their homes for 40 or 50 years or even longer. They raised their kids there and plan on retiring in the same house. But that’s not the average tenure.

It’s the exception to the rule of how long people really stay in their homes, according to many studies and trends done on homebuyers in America.

Verify your new rateWhat Affects Your Tenure In Your Home?

So many things can affect how long people stay in the homes they buy.

They might have to move because of a job or a sick elderly parent a few states away. They might need a bigger or smaller home depending on the size of their family or their needs. Or they might just want a whole different style or want to move into the city or move out into the country.

Everyone has wants and desires. And outside forces such as the housing crisis also prompt people to stay longer or shorter than they wanted to.

It’s Longer Than It Used To Be

In 2016, the tenure of homeowners increased to ten years. One more than the year before, according to the National Association of Realtors 2016 Profile of Homebuyers and Sellers.

The NAR report shows that people stayed in their homes only six to seven years before the housing downturn began. After 2008, this increased to nine years.

Many remained in their houses because their mortgage balances exceeded their property values. Just prior to 2007, the average tenure in a home was only six years.

But Everyone’s Different

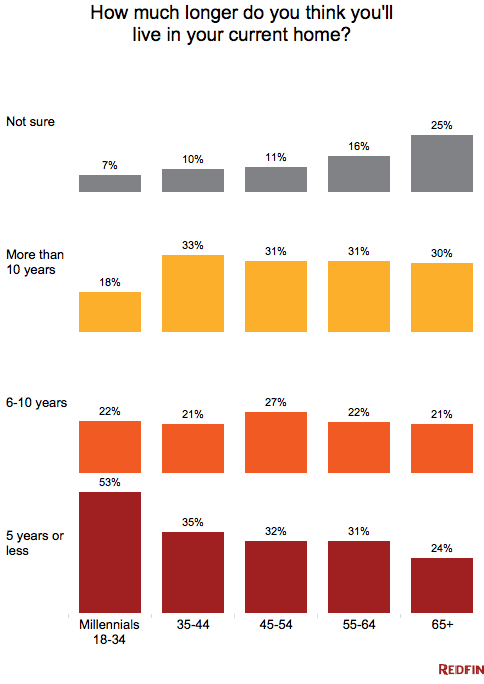

While buyers overall are remaining in their homes longer, not everyone is staying put for ten years. Younger buyers and first-timers are moving sooner. However, Millennials are more likely to keep their homes and rent them out than young homeowners in the past. according to researchers at Redfin.

If retirement, starting a family, or a work-related move is in your near future, it doesn’t really matter what everyone else is doing. You should plan your own mortgage needs based around your own five-to-seven year plan.

Time To Sell?

Those who hung on to their houses through the crisis and the last nine years have probably accumulated enough equity to sell their homes at a profit. Their patience after delaying a sale could earn them big rewards.

However, because interest rates and home prices are up, they may have fewer choices of homes to buy.

The 2016 NAR survey showed the reasons most sellers wanted to sell homes in 2016 include: needing more room (18 percent); desire to move closer to friends and family (15 percent); and job relocation (14 percent). The typical home seller was 54 years old with a median household income of $100,700.

Verify your new rateDecrease Migration, Increased Renovation

Despite Americans having higher education levels and more technological advances, migration has decreased since 1990. Migration stats fell for all groups no matter gender, education, race, income, marital status, employment status or metropolitan area, according to Urban Institute research.

Instead of moving, homeowners are taking out more home improvement loans, since they are staying long in their homes and need to maintain them longer.

The research also shows that interstate movers dropped to 1.5 percent from 2010 to 2015 from nearly three percent in the 1980s.

Rates Up, Sales Down

Rising interest rates for most mortgage programs could keep those with low rates from moving. This would keep inventory low, pushing prices higher. Those locked into a historically low three-to-four percent interest rates may find it hard to move up to a more expensive house and a higher rate.

One Pulsenomics survey of more than 100 housing experts and economists found that they expect interest rates to hit 4.75 percent this year for 30-year fixed-rate home loans.

Asked about the greatest impact on U.S. housing last year, 56 percent responded with “mortgage rate lock-in.”

A Little Perspective

Homebuyers should not be alarmed, however. For a median-priced home in the US, $312,900, financed with 20 percent down, the recent rate run-up from 4.0 percent to 4.25 percent only added $36 a month to its mortgage payment.

And those who expect to keep their homes six or fewer years could shave their mortgage rates down into the three percent range once again by choosing a 5/1 ARM instead of a fixed mortgage.

What Are Today’s Mortgage Rates?

Current mortgage rates have recently spiked, so borrowers will need to decide if they want to pay higher mortgage rates when they sell old homes and buy new ones. However, if you’re considering a move, don’t make a decision without running the numbers first.

Time to make a move? Let us find the right mortgage for you