Mortgage rate forecast for next week (May 4 - May 8)

The 30-year fixed mortgage rate ticked up slightly this week but remains near its lowest level in three consecutive spring homebuying seasons, signaling a market that continues to trade in a narrow band as borrowers and lenders alike wait for clearer economic signals.

According to Freddie Mac’s Primary Mortgage Market Survey (PMMS) on April 30, 2026, the 30-year fixed-rate mortgage averaged 6.3%, up from 6.23% the prior week. The 15-year fixed-rate mortgage averaged 5.64%.

The 30-year fixed-rate mortgage declined again this week to 6.23%. Rates currently stand at their lowest level in the last three spring homebuying seasons. This improvement, coupled with a pickup in purchase applications and refinance activity, as well as an increase in monthly pending home sales, underscores signs of improving momentum in the market.

| Average 30-year fixed rate | 1-week ago | 4-weeks ago | 3-months ago | 1-year ago |

| 6.23% | 6.30% | 6.38% | 6.09% | 6.83% |

The latest borrowing activity

The MBA Weekly Application Survey for the week ending April 18, 2026, showed total mortgage application volume declined 0.8% from the previous week. Purchase applications rose 1.0%, a modest but encouraging sign for the spring housing market. Refinance applications fell 3.0%, suggesting fewer borrowers see an advantage in refinancing at current rate levels.

The slight uptick in purchase activity aligns with improving spring inventory conditions in many markets, even as the refinance pullback reflects the reality that most current homeowners still hold rates well below today’s levels. For prospective buyers looking to understand lender offers, learning [how to read a loan estimate](https://themortgagereports.com/11306/how-to-read-a-loan-estimate) can help compare options effectively.

Find your lowest mortgage rate. Start hereThe overall picture is one of stability. Rates are not spiking higher, and they are not dropping sharply either. This range-bound environment is likely to persist through May as the market digests incoming inflation data and waits for the Federal Reserve’s next policy meeting in June.

- Will rates go down in April?

- 90-day forecast

- Expert rate predictions

- Mortgage rate trends

- Rates by loan type

- Mortgage strategies for April

- Mortgage rates FAQ

Will mortgage rates go down in May?

Mortgage rates are likely to stay range-bound in May 2026. The 30-year fixed currently sits at 6.3%, and neither inflation trends nor Federal Reserve policy suggest a significant move in either direction over the coming weeks. The Fed held rates steady at its April 29, 2026 meeting, and the next FOMC decision is not scheduled until June 16-17, removing one potential catalyst for rate movement during May.

-Tony Julianelle, CEO at Atlas Real Estate

Two key data releases could create short-term volatility. The Consumer Price Index (CPI) report lands on May 13, and the Personal Consumption Expenditures (PCE) price index follows on May 30. Both are critical inflation gauges the Fed relies on when making rate decisions. A hotter-than-expected CPI print could push mortgage rates toward the upper end of the 6.2% to 6.6% range, while a softer reading could provide brief relief. You can track how these data points have influenced rates over time on our [30-year mortgage rate history chart](https://themortgagereports.com/61853/30-year-mortgage-rates-chart).

Geopolitical uncertainty continues to play a role in rate direction. Ongoing conflict in the Middle East is adding inflationary pressure through energy markets while simultaneously driving demand for safe-haven assets like U.S. Treasuries. These opposing forces are helping keep rates locked in a tight range. For a deeper look at where rates may head beyond May, see our full [mortgage rate forecast](https://themortgagereports.com/32667/mortgage-rates-forecast-fha-va-usda-conventional).

The bottom line: meaningful rate declines in May are unlikely without a clear disinflationary signal or a shift in Fed guidance. Borrowers should plan around the current rate environment rather than waiting for a dramatic drop.

Expert mortgage rate predictions for April

Hannah Jones, Senior Economic Analyst at Realtor.com

Prediction: Rates will hold steady

Mortgage rates have made meaningful progress in April, falling to 6.23% this week, the lowest level in three consecutive spring homebuying seasons. That said, the ongoing conflict in the Middle East remains a significant source of uncertainty, and any further rate improvement will depend heavily on whether the current ceasefire holds and evolves into something more durable. With the FOMC widely expected to hold rates steady at its meeting next week, we don’t anticipate a major policy catalyst in either direction, leaving rates likely to hover near current levels in May, though volatility could quickly return if geopolitical conditions shift.

Dave Meyer, Chief Investment Officer at BiggerPockets

Prediction: Rates will hold steady

Mortgage rates are unlikely to move significantly in May, and the average rate on a 30-year fixed rate mortgage will likely remain in the 6.2%-6.6% range. Renewed inflationary pressures, spurred by the war in Iran, have pushed up bond yields and mortgage rates in recent months. Rates are unlikely to revert to recent lows until markets have a better line of sight on lower inflation. The Federal Reserve is also awaiting more inflation data, making a cut to the Federal Funds Rate highly unlikely at the next FOMC meeting. At this point, it seems more likely for rates to climb modestly in May, brought on by a potentially hot inflation print for April, than for rates to fall meaningfully — but significant movement in either direction is not expected.

Ralph DiBugnara, President at Home Qualified

Prediction: Rates will hold steady

Mortgage rates in May should stay relatively range-bound, likely hovering in the mid-to-high 6% range, with some day-to-day volatility. We’re still dealing with persistent inflation and a Federal Reserve that’s not in a rush to cut rates aggressively, which is keeping upward pressure on yields. At the same time, economic uncertainty and global tensions are creating moments where rates improve, but those dips have been short-lived. The reality is we’re in a higher-for-longer rate environment for now. For buyers, the key isn’t trying to time the market perfectly. It’s being prepared. The opportunities are still there, especially as inventory picks up and competition varies by market, but execution and strategy matter more than ever right now.

Sam Khater, Chief Economist at Freddie Mac

Prediction: Rates will moderate

The 30-year fixed-rate mortgage declined again this week to 6.23%,. Rates currently stand at their lowest level in the last three spring homebuying seasons. This improvement, coupled with a pickup in purchase applications and refinance activity, as well as an increase in monthly pending home sales, underscores signs of improving momentum in the market.

Lawrence Yun, Chief Economist at National Association of Realtors

Prediction: Rates will moderate

March home sales remained sluggish and below last year’s pace

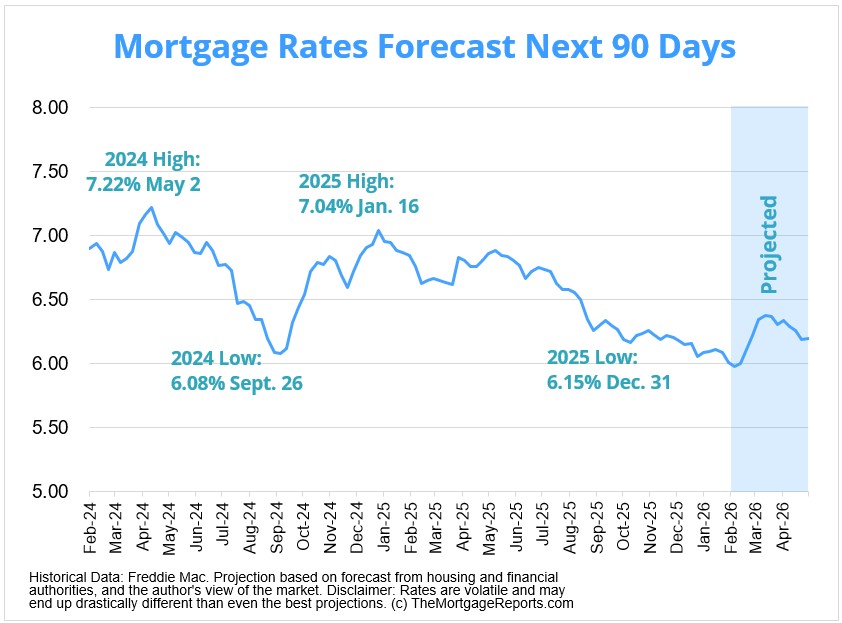

Mortgage interest rates forecast next 90 days

The Federal Reserve’s decision to hold its benchmark rate steady on April 29, 2026, was widely expected by markets. With the next FOMC meeting not until June 16-17, May represents a policy quiet period. The Fed has signaled it needs more data before considering any rate adjustments, and that data will arrive in the form of the May 13 CPI report and the May 30 PCE release. Unless one of those reports delivers a significant surprise, the Fed’s posture is unlikely to change before mid-June.

Inflation remains the central variable for mortgage rate direction over the next 90 days. Bond markets are pricing in a higher-for-longer scenario, with persistent price pressures in services and energy sectors keeping 10-year Treasury yields elevated. Mortgage rates track closely with the 10-year Treasury, so any sustained move lower in rates will require convincing evidence that inflation is decelerating toward the Fed’s 2% target.

Find your lowest mortgage rate. Start hereBorrowers should watch three things closely over the next three months: the May CPI and PCE inflation readings, the June FOMC meeting and any updated dot-plot projections, and developments in the Middle East conflict that could affect global energy prices. Each of these has the potential to push rates in either direction, but absent a clear catalyst, expect rates to stay within a relatively narrow band.

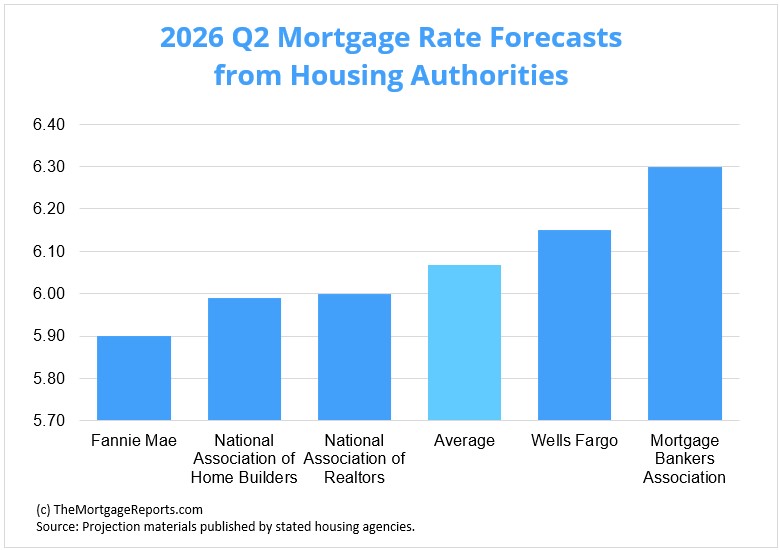

Mortgage rate predictions for May 2026

Major housing authorities are projecting that mortgage rates will remain near current levels through Q2 2026. Both Fannie Mae and the Mortgage Bankers Association forecast the 30-year fixed rate at 6.30% for this quarter. The consensus average is 6.30%.

The alignment between Fannie Mae and the MBA is notable. Both organizations are projecting 6.30%, reflecting a broad consensus that rates will hold steady barring an unexpected economic shift. This agreement suggests that neither a meaningful decline nor a significant spike is the base case for the near term.

| Housing Authority | 30-Year Mortgage Rate Forecast (Q2 2026) |

| National Association of Home Builders | 5.99% |

| National Association of Realtors | 6.00% |

| Wells Fargo | 6.15% |

| Fannie Mae | 6.30% |

| Mortgage Bankers Association | 6.30% |

| Average Prediction | 6.148% |

Current mortgage interest rate trends

As of April 30, 2026, the 30-year fixed mortgage rate stands at 6.3% according to Freddie Mac’s PMMS. The 15-year fixed rate is 5.64%. These rates represent the most widely cited benchmark for the U.S. mortgage market and reflect averages across a broad range of borrower profiles and lender offerings.

Compared to the prior week, the 30-year rate rose 7 basis points from 6.23%. That week-to-week fluctuation is consistent with the type of modest volatility the market has experienced throughout the spring. Rates have not broken decisively in either direction, instead oscillating within a relatively tight range.

The broader rate trajectory over recent months tells a story of stubborn stability. After reaching multi-year highs in late 2023 and early 2024, rates gradually eased but have struggled to break below the 6% threshold in any sustained way. The 6.23% reading from the prior week marked the lowest level seen during the last three spring homebuying seasons, suggesting incremental progress even if the pace has been slow.

| Month | Average 30-Year Fixed Rate |

| March 2025 | 6.65% |

| April 2025 | 6.73% |

| May 2025 | 6.82% |

| June 2025 | 6.82% |

| July 2025 | 6.72% |

| August 2025 | 6.59% |

| September 2025 | 6.35% |

| October 2025 | 6.25% |

| November 2025 | 6.24% |

| December 2025 | 6.19% |

| January 2026 | 6.10% |

| February 2026 | 6.05% |

| March 2026 | 6.18% |

| April 2026 | 6.23% |

Source: Freddie Mac

Several factors are keeping rates from falling further. Persistent inflation, particularly in services and shelter costs, continues to weigh on bond markets. The Federal Reserve’s cautious approach to rate cuts means the federal funds rate remains elevated, and that stance filters through to mortgage pricing. At the same time, geopolitical uncertainty is adding a risk premium that supports higher yields.

Looking ahead, the path lower for mortgage rates likely requires a combination of decelerating inflation, a more dovish Fed tone, and reduced global uncertainty. None of those conditions are guaranteed in the near term. Borrowers tracking rate trends can review our [30-year mortgage rate history chart](https://themortgagereports.com/61853/30-year-mortgage-rates-chart) for context on how current levels compare to historical patterns.

For now, the market consensus points to rates holding near the 6.3% mark through the end of Q2 2026. Any meaningful move lower would likely require a catalyst that shifts the inflation outlook or prompts the Fed to signal rate cuts at its June meeting.

Mortgage rate forecast by loan type

Different loan types carry different rate profiles, and borrowers should understand how each product is positioned in the current environment. Your optimal loan type depends on your credit score, down payment, military service status, and property location. Here is what to expect across the major mortgage categories in May 2026.

Find your lowest mortgage rate. Start here30-year fixed-rate mortgage

The 30-year fixed is the most popular mortgage product in the U.S., and it currently averages 6.3% according to Freddie Mac’s April 30, 2026 survey. This rate is slightly above the prior week’s 6.23% but remains near the lowest level recorded during the past three spring homebuying seasons. The 30-year fixed provides payment stability over the full loan term, making it the default choice for buyers who plan to stay in their home long-term.

In a range-bound rate environment, locking a 30-year fixed near 6.3% offers predictability. Borrowers who want to compare rate offers from multiple lenders can benefit from learning [how to get the lowest mortgage rate](https://themortgagereports.com/17089/how-to-get-the-lowest-mortgage-rate) through strategic shopping.

The 15-year fixed-rate mortgage averages 5.64% as of April 30, 2026. The roughly 66-basis-point discount compared to the 30-year fixed reflects the shorter loan term and reduced risk to lenders. Borrowers who can handle higher monthly payments will save significantly on total interest costs over the life of the loan.

This product works well for homeowners who are refinancing and want to accelerate their payoff timeline, or for buyers purchasing below their maximum budget. The trade-off is a higher monthly obligation, so borrowers should ensure their budget has room for the increased payment before committing.

Jumbo loans finance properties that exceed conforming loan limits, which are $766,550 in most U.S. counties for 2026. Jumbo rates have historically traded at a premium to conforming rates, though competition among portfolio lenders has narrowed that gap in recent years. Borrowers considering a jumbo loan can review the specific requirements and current conditions in our [jumbo mortgage guide](https://themortgagereports.com/7844/jumbo-mortgage-loan).

Jumbo borrowers typically need strong credit scores, larger down payments, and significant cash reserves. In a stable rate environment like the current one, shopping among multiple lenders is especially important for jumbo products, as pricing can vary more widely than with conforming loans.

Mortgage rate strategies for May 2026

With the 30-year fixed rate at 6.3% and housing authorities projecting rates to hold near that level through Q2 2026, this is a market that rewards preparation over speculation. The upcoming June FOMC meeting is unlikely to shift policy expectations in the near term, and the May CPI and PCE data releases are the most likely sources of any short-term rate movement.

Find your lowest mortgage rate. Start hereBorrowers who wait for a dramatic rate decline may miss opportunities in a housing market where spring inventory is improving and purchase application activity is trending slightly upward. The 1.0% increase in purchase applications for the week ending April 18, 2026 suggests that many buyers are choosing to act in the current environment rather than sit on the sidelines.

The strategies below are designed to help buyers and refinancers make informed decisions in a stable but uncertain rate environment.

Every borrower’s situation is different, but a few principles apply broadly right now. Know your rate before you shop for homes, get multiple lender quotes, and understand the full cost of your loan beyond just the interest rate.

Rate lock strategy

In a range-bound rate market, the rate lock decision becomes straightforward. With the 30-year fixed at 6.3% and consensus forecasts showing no significant decline through Q2 2026, locking your rate at or near current levels protects you against the possibility of rates drifting higher on a hot inflation report.

A 30 to 45-day lock is standard for most purchase transactions. If you are further out from closing, ask your lender about extended lock options and whether a float-down provision is available. A float-down lets you capture a lower rate if rates decline before closing, typically for a small additional fee.

Borrowers who are undecided about locking should pay close attention to the May 13 CPI release. A higher-than-expected inflation reading could push rates toward the upper end of the 6.2% to 6.6% range, making a pre-CPI lock a reasonable hedge.

Refinancing at 6.3% only makes sense for borrowers who took out loans at significantly higher rates, typically 7% or above. The 3.0% weekly decline in refinance applications for the week ending April 18, 2026 reflects the reality that most homeowners are sitting on rates well below current levels.

If you purchased or refinanced during the rate peaks of late 2023 or early 2024, run the numbers on a refinance at today’s rates. Factor in closing costs, which typically run 2% to 5% of the loan amount, and calculate your break-even timeline. If you plan to stay in the home long enough to recoup those costs, refinancing could lower your monthly payment.

Refinance timing

Cash-out refinancing is another consideration for homeowners who have built significant equity. With home values still elevated in many markets, tapping equity at 6.3% may be preferable to higher-rate alternatives like personal loans or credit cards.

Spring 2026 is shaping up to be a more balanced market for buyers than the past few years. Inventory has been improving in many regions, and the 1.0% increase in purchase applications suggests growing buyer activity without the frenzied competition of previous cycles.

Buyers should get pre-approved before starting their home search. A pre-approval letter based on current rates gives you a clear budget and strengthens your offer in competitive situations. Compare offers from at least three lenders to ensure you are getting the best combination of rate, fees, and loan terms.

Do not wait for a rate that may not come. As Ralph DiBugnara noted, execution and strategy matter more than timing in this environment. A home purchase is a long-term financial decision, and the difference between 6.2% and 6.4% on a 30-year mortgage has a relatively modest impact on monthly payments compared to the cost of waiting while home prices continue to appreciate.

Home buying strategy

Consider whether buying down your rate with discount points makes sense. In a stable rate environment, paying upfront to reduce your rate by 0.25% or 0.5% can pay off if you hold the mortgage for several years.

Your credit score is the single biggest factor in the rate a lender will offer you. Even in a market where average rates sit at 6.3%, individual borrowers with excellent credit (740+) may qualify for rates meaningfully below the average, while those with lower scores could pay well above it.

- Your credit score and credit history

- Your personal finances

- Your down payment (if buying a home)

- Your home equity (if refinancing)

- Your loan-to-value ratio (LTV)

- Your debt-to-income ratio (DTI)

If you are planning to buy or refinance in the next 60 to 90 days, take steps now to optimize your credit. Pay down revolving balances to reduce your credit utilization ratio below 30%, and avoid opening new credit accounts or making large purchases on existing cards.

Check your credit reports at AnnualCreditReport.com for errors and dispute any inaccuracies Pay all bills on time, as payment history accounts for 35% of your FICO score Reduce credit card balances to below 30% of your available credit limit Avoid applying for new credit cards, auto loans, or personal loans before your mortgage application Do not close old credit accounts, as the length of credit history affects your score Ask your lender about rapid rescoring if you need a quick credit score improvement before closing

Borrowers who are several months away from purchasing should use that time to build a stronger credit profile. Even a 20-point improvement can move you into a better rate tier and save thousands over the life of your loan.

Compare mortgage and refinance rates. Start here

Mortgage interest rate FAQ

Current mortgage rates are averaging 6.23% for a 30-year fixed-rate loan and 5.58% for a 15-year fixed-rate loan, according to Freddie Mac’s latest weekly rate survey. Your individual rate could be higher or lower than the average depending on your credit score, down payment, and the lender you choose to work with, among other factors.

Rates are expected to remain relatively stable in early May 2026. The 30-year fixed rate currently sits at 6.3%, and with no FOMC meeting scheduled until June 16-17, there is no major policy catalyst on the immediate horizon. The May 13 CPI release is the next data point that could cause short-term rate movement in either direction.

If inflation continues to dissipate and the economy cools or goes into a recession, it's likely mortgage rates will decrease in 2026. Although, it's important to remember that interest rates are notoriously volatile and are driven by many factors, so they can rise during any given week.

Mortgage rates may rise in 2026. High inflation, strong demand in the housing market, and policy changes by the Federal Reserve in 2022 and 2023 all pushed rates higher. However, if the U.S. does indeed enter a recession, mortgage rates could come down.

Freddie Mac is now citing average 30-year rates in the 6% range. If you can find a rate in the 5s or 6s, you’re in a very good position. Remember that rates vary a lot by borrower. Those with perfect credit and large down payments may get below-average interest rates, while poor-credit borrowers and those with non-QM loans could see much higher rates. You’ll need to get pre-approved for a mortgage to know your exact rate.

For the most part, industry experts do not expect the housing market to crash in 2026. Yes, home prices are over-inflated. But many of the risk factors that led to the 2008 crash are not present in today’s market. Low inventory and massive buyer demand should keep the market propped up. Plus, mortgage lending practices are much safer than they used to be. That means there’s not a subprime mortgage crisis waiting in the wings.

At the time of this writing, the lowest 30-year mortgage rate ever was 2.65%. That’s according to Freddie Mac’s Primary Mortgage Market Survey, the most widely used benchmark for current mortgage interest rates.

Locking your rate is a personal decision. You should do what’s right for your situation rather than trying to time the market. If you’re buying a home, the right time to lock a rate is after you’ve secured a purchase agreement and shopped for your best mortgage deal. If you’re refinancing, you should make sure you compare offers from at least three to five lenders before locking a rate. That said, rates are rising. So the sooner you can lock in today’s market, the better.

Refinancing at 6.3% makes financial sense primarily for borrowers whose current rate is 7% or higher. If that describes your situation, calculate your break-even point by dividing your closing costs by your monthly savings to determine how long you need to stay in the home to recoup the expense. For borrowers with rates below 6%, refinancing at current levels would increase your costs.

It’s often worth refinancing for 1 percentage point, as this can yield significant savings on your mortgage payments and total interest payments. Just make sure your refinance savings justify your closing costs. You can use a mortgage calculator or speak with a loan officer to crunch the numbers.

Start by choosing a list of three to five mortgage lenders that you’re interested in. Look for lenders with low advertised rates, great customer service scores, and recommendations from friends, family, or a real estate agent. Then get pre-approved by those lenders to see what rates and fees they can offer you. Compare your offers (Loan Estimates) to find the best overall deal for the loan type you want.

What are today’s mortgage rates?

Mortgage rates are rising, but borrowers can almost always find a better deal by shopping around. Connect with a mortgage lender to find out exactly what rate you qualify for.

Time to make a move? Let us find the right mortgage for you1Today's mortgage rates are based on a daily survey of select lending partners of The Mortgage Reports. Interest rates shown here assume a credit score of 740. See our full loan assumptions here.

Selected sources:

- https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- http://www.freddiemac.com/research/datasets/refinance-stats/index.page