Editor's note: This article was originally published on June 10, 2020, and updated on July 28, 2020, with the latest Fed forecasts

Don’t wait on the Fed for lower mortgage rates

Mortgage rates have hit record lows five times this year. They’re currently resting at or near their lowest levels in 50 years.

That’s in part thanks to the Fed, whose intervention in the mortgage market has forced and kept rates down during the COVID pandemic.

But with the Fed already injecting capital into the mortgage market, and holding its benchmark rate near 0%, there’s little it can do to push mortgage rates lower still.

That means home shoppers and refinancers shouldn’t wait on the Fed.

For those ready to buy or refinance, there aren’t many reasons to hold off on locking a rate.

Find and lock a low rateFOMC expected to hold interest rates steady this week

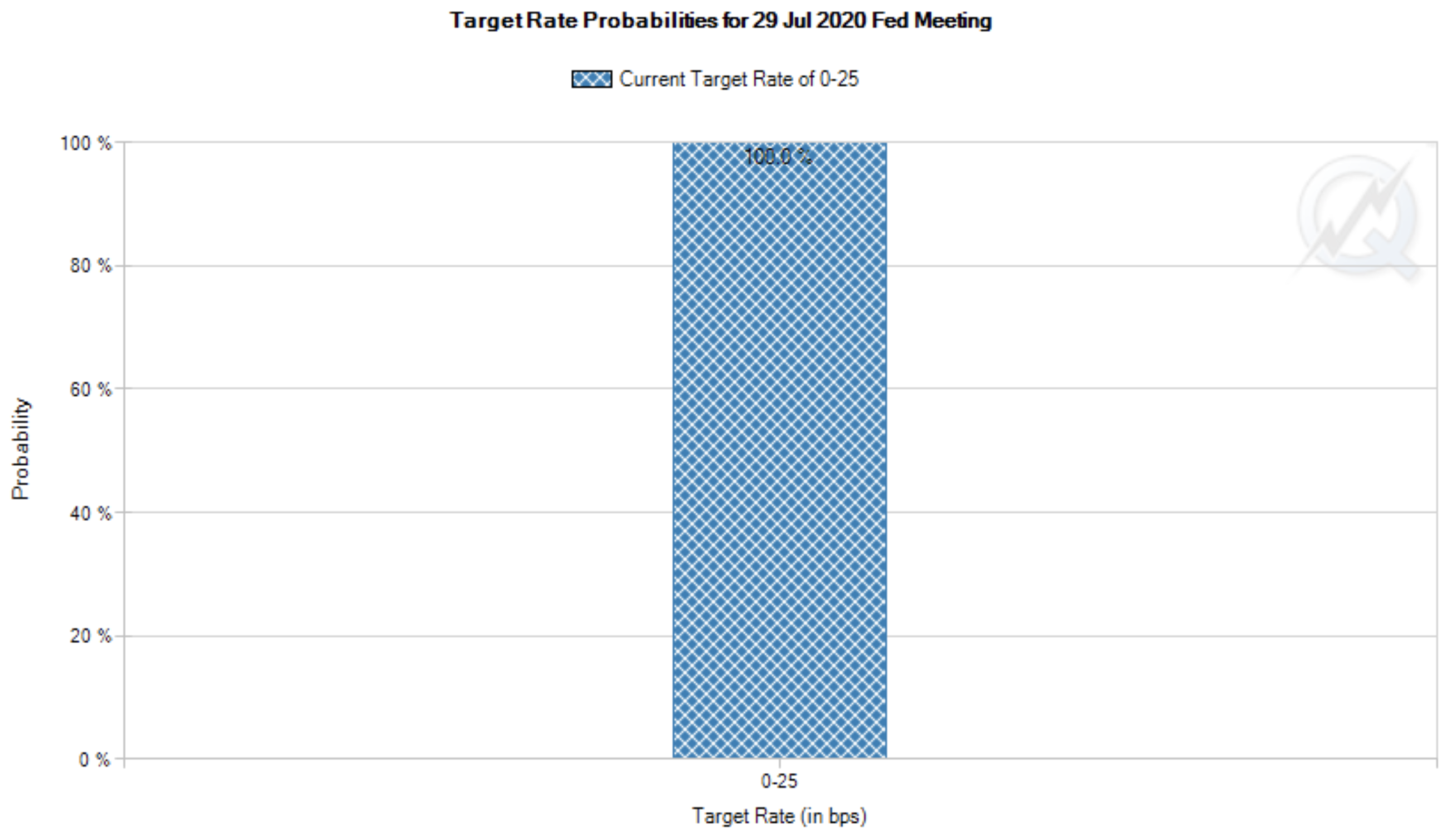

CME Group’s FedWatch tool is citing a 100% probability that the FOMC — the Fed’s decision-making body — will not change its current target interest rate of 0-0.25% when it meets this week.

Image: CME Group FedWatch

What’s more, the FOMC stated at its last meeting that it intends to hold its benchmark rate steady until 2021 or 2022.

Fed policy isn’t likely to change until the U.S. starts making real progress toward economic recovery post-coronavirus.

Although the FOMC does not set mortgage rates, the overall low-interest environment means mortgage shoppers can expect historic rates to continue for quite some time.

Find a low mortgage rateWhat to look for in this week’s FOMC statement

As we mentioned above, the Fed has no intention of changing its target interest rate any time soon.

But there’s a chance it could update its policy on quantitative easing (QE) — the process by which the Federal Reserve buys up mortgage-backed securities to keep borrowing costs low.

If the Fed decides to increase its mortgage purchase program, it could potentially force mortgage rates lower. QE was a big driver behind the downward rate movement in recent months.

After its most recent meeting, the FOMC indicated it would keep buying mortgages at the current pace.

But a change to that policy is the one thing borrowers should look out for if they want a heads up on potential rate movements.

Fed agrees: Rates aren’t rising any time soon

Admittedly, the reasons for the current low rate environment are nothing to cheer about.

The Fed’s interest rate policy is based on wildly uncertain economic times for the foreseeable future.

Coronavirus has ravaged the U.S. economy and led to record-high unemployment. Worldwide, things aren’t much better.

The silver lining, though, is a Fed that unanimously favors a fed funds rate near 0%. The Fed doesn’t control mortgage rates, but the group sure can help them stay low.

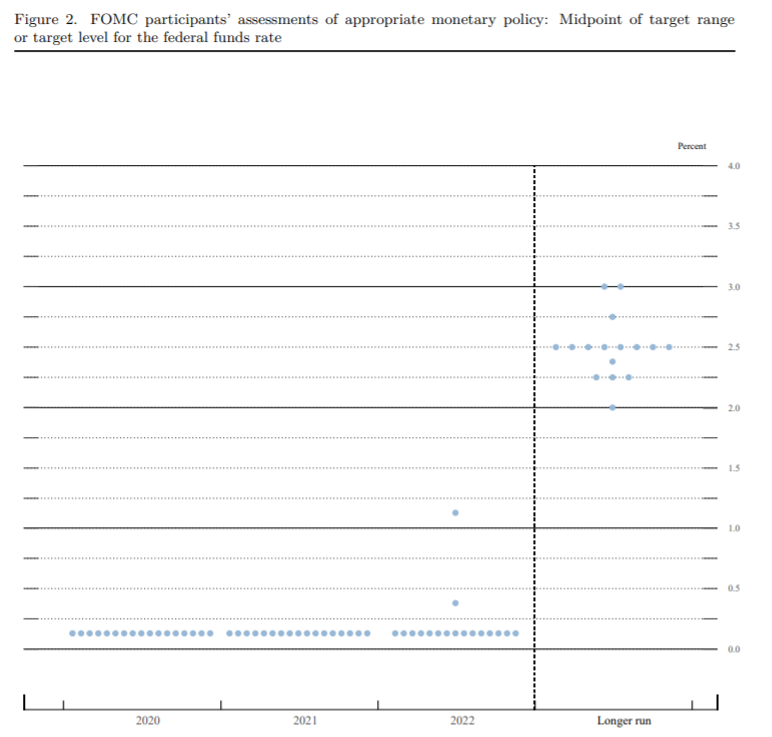

In a rare show of solidarity, every single Fed member predicted low rates through 2021, with only two dissenters saying rates would rise in 2022. Each dot in the below image represents a Federal Reserve member, hence this chart’s nickname, the “dot plot.”

Typically, these dots are somewhat spread apart: some Fed predict or even argue for a higher Fed rate in the future.

But this chart shows a rare, nearly across-the-board agreement that rates should stay low for some time.

Your next move as a mortgage shopper

As mentioned, mortgage rates don’t follow the federal funds rate perfectly. Mortgages could get more expensive even as the Fed uses its full power to keep all rates low.

With that argument, those seeking to purchase a home or refinance shouldn’t wait. Rates are near 50-year lows right now, and it will be hard for them to go lower.

But if you’re in the market to buy or refi in coming years, be encouraged.

Many people are working to raise their credit score, advance their career, or set a budget. In these cases, they can likely breathe a sigh of relief. Low rates will probably be a round in a year or two when they are ready.

No matter what your home finance timeline, today’s meeting of the Federal Reserve should brighten your day.

It appears mortgage rates will continue their record-breaking streak.

Time to make a move? Let us find the right mortgage for you