Understanding minimum property requirements for a VA loan

You already know about the Department of Veterans Affairs’ eligibility requirements for borrowers. But did you know it also sets strict eligibility thresholds for the homes it’s willing to lend against?

Verify your VA loan eligibility with Veterans UnitedThese are called “VA minimum property requirements” (MPRs), and they are important when buying a home with a VA loan. Here’s what you should know.

In this article (Skip to...)

VA loan program overview

The VA loan program provides affordable mortgage loans for active-duty military service members and veterans. Unlike an FHA loan or conventional loan, the VA loan will finance a home purchase with no down payment and no ongoing mortgage insurance.

Because it’s a government-backed loan, VA lenders are able to offer lower interest rates, too. Although the VA has not set a minimum credit score requirement, lenders are allowed to establish their own minimums and many want to see a score of at least 580-620.

Keep in mind, the VA loan program does have its own eligibility requirements, and it also has extensive property requirements that can be confusing for first-time home buyers.

It’s important to have an understanding of the VA MPRs and to work with a loan officer and real estate agent who have familiarity with the program.

VA minimum property requirements: What’s important and what’s not

Before exploring the extensive list of VA MPRs, let’s consider what the Department of Veterans Affairs has to say about its requirements.

VA appraisers should take the general condition of the home into account when determining its appraised value. But an appraiser shouldn’t block a home purchase solely because of minor details, such as poor decoration or an overdue servicing of the furnace. The VA’s guidelines say:

“The appraiser should not recommend repairs of cosmetic items, items involving minor deferred maintenance or normal wear and tear, or items that are inconsequential in relation to the overall condition of the property. While minor repairs should not be recommended, the appraiser should consider these items in the overall condition rating when estimating the market value of the property.”

The overarching objective of MPRs is to make sure the home buyer is getting a property that is “safe, structurally sound and sanitary.”

But, the VA says, “The scope of MPRs also includes issues related to the property’s location and legal considerations.”

Complete list of VA minimum property requirements

In addition to ensuring that home buyers don’t overpay for a property, the VA appraisal process makes certain that the home is a safe, move-in ready primary residence for the buyer.

Check your eligibility for a VA home loan. Start here.VA appraisers provide a thorough examination of the property to ensure that it conforms with over 30 VA minimum property requirements that we explore below.

Keep in mind, though, that a VA appraisal is not a home inspection. And despite the extensive list of VA MPRs, a home inspection is still recommended to ensure there are no hidden issues with the property that could be costly to fix after moving in.

1. Marketable real estate

The home must be a single dwelling (which may include a multi-family dwelling with two to four units) that’s legally considered real estate and “readily marketable.” That last bit means that the home can easily be sold later. So it shouldn’t be likely to sit around for years waiting for a buyer to turn up.

You may be able to buy more than one parcel of land but they need to be “contiguous.” That means they adjoin each other. If there’s a road or waterway separating the parcels, the VA appraiser has to assess how that impacts the usefulness and saleability of the property.

2. Space and construction requirements

The home must be big enough for you and any other residents to live, sleep, cook and eat. It’ll also need sanitary facilities.

If its construction is unusual (for instance log homes, homes with an earth roof, or properties in a dome shape), it must still comply with local building codes. And the VA appraiser has to work out whether its out-of-the-ordinary qualities will make it less marketable when the time comes to sell again.

3. Accessibility

You must be able to access the home with a vehicle or as a pedestrian safely all year round. That access may be from a public or private road.

However, if neighbors share the private road, there may be legal issues. The VA loan program wants to see a fair, enforceable agreement about who pays for maintenance.

Additionally, you must have a permanent legal right to gain access. So, if you have to pass over other people’s land to get to your home, there must be an “easement” (a legal right to trespass) already in place.

There are also access rules concerning row houses and those built on the property line. These mostly concern accessing your backyard (it’s fine if you can only do so through the home) and being able to maintain the exterior.

4. Encroachments

Suppose a neighbor is “encroaching” (intruding) on the home. Maybe they’ve built a fence or part of a garage a foot on your side of the boundary. Or they might have a roof that extends over it. Or perhaps your seller is encroaching on a neighboring property.

Either way, the appraiser must report it. And someone will have to resolve the issue before you’ll get your VA loan.

5. Drainage and topography

Drainage rules are exactly what you’d expect. Waste and surface water must flow off your site quickly and positively. And it mustn’t “pond” (form pools) on your land.

Topography concerns physical threats to your site. So it mustn’t be subject to mudslides, avalanches or similar from neighboring properties.

Check your home buying options. Start here6. Geological or soil instability, subsidence and sinkholes

This concerns geological risks posed by your own property. And the only thing worse than your appraiser spotting these issues is when they miss them. Because you really don’t want to discover you have mudslides or sinkholes when you already own the home. And the same goes for “subsidence” (the gradual caving in or sinking of an area of land), which can undermine the home’s foundations in a very expensive way.

Suppose your appraiser suspects any of these to be risks. Then you or the owner will need to hire an expert geologist to say something different. And, if there’s evidence of existing damage to the home from such causes, a licensed contractor will have to fix it before you get a VA loan.

7. Special flood hazard area

If you want to buy a home or plot that floods regularly, you won’t get a VA loan. There are restrictions even if it doesn’t flood, but is in a high-risk area.

FEMA designates special flood hazard areas (SFHAs). You can still buy a home in one of these, but only if you buy flood insurance. Note that flood insurance is not included in standard homeowners insurance policies and must be purchased separately. If the home’s uninsurable or you can’t get that insurance, the VA won’t guarantee your loan.

That last paragraph applies in almost all SFHAs. But it doesn’t (you won’t need flood insurance) if your home’s in those zoned B, C, X or D by FEMA.

8. Non-residential use

VA minimum property requirements don’t bar you from buying a home that doubles up as your workplace. But it does impose conditions.

The property must primarily be for residential use. So you can’t purchase a huge warehouse with a tiny home in the corner. And your local authority must be cool with the business use you intend. So the property must either be correctly zoned or the authority must acknowledge its acceptance of your non-conforming use.

Three more rules:

- The business use mustn’t detract from the residential character of the property

- Only one business is allowed to operate from the home

- The VA appraiser mustn’t add value for business use or commercial fittings when determining how much the home is worth

You can see what the VA’s doing here. It guarantees loans on residential (not commercial) property but it’s happy to help when it reasonably can.

9. Zoning

Obviously, the VA wants to be sure the home is correctly zoned. That’s mostly because it may be hard for you to later sell a place that’s zoned improperly — and that could affect the value of the property.

It may still be willing to approve your loan if the home is incorrectly zoned. But only if the local authority accepts its status. This is called “legal non-conforming.” However, the appraiser must note that fact on her appraisal and assess whether (and by how much) that will affect the property’s value.

10. Local housing and planning authority code enforcement

Some areas enforce their local code requirements whenever a home is sold. If the place you want to buy is in such an area, your appraiser will pay special attention to the property’s compliance with the code.

Suppose the appraiser spots any improvements that are not up to code. They must note those failures. And they will make an allowance in the appraisal for the repairs necessary to remove them or make them compliant.

11. Water, gas, electricity and other utilities

Each home (or each unit, if you’re buying a multi-family dwelling with two to four units) must have an electricity supply sufficient to provide lighting and run necessary equipment. If your appraiser notices any exposed, frayed or otherwise dangerous wiring, that will have to be fixed before your loan can be approved.

VA minimum property requirements are concerned that your access to all your utilities can’t be challenged. So if your electricity, water, gas or sewer lines run over other people’s land or apartments, the VA wants to know that those people can’t suddenly choose to interrupt your services. This means you’ll need easements (you remember: those legal rights to trespass) that guarantee your continuing access. They must also allow contractors to get to utility lines to maintain and repair them.

All this is pretty standard stuff. And, if they need them, the vast majority of homes already have such easements in place.

One last thing: If you are buying one of those multi-unit dwellings, each unit must have its own service shut-offs.

12. Water supply and sanitary facilities

No surprises here. The VA wants to know that the home has a continuous supply of water that’s safe to drink (“potable”). And that supply must be adequate for showering, bathing and sanitary uses, as well as drinking.

The VA also insists on a hot-water supply, sanitary facilities, and the safe disposal of sewage. If there’s any doubt about whether the water’s potable, you may have to install a filtration system.

13. Individual water supply and shared wells

If you use a well, spring, lake, rainwater cistern, holding tank, or another private source (“individual water supply”), you’ll still need a safe and adequate supply.

Samples must be collected and tested by an independent expert. And your water must conform with local authority regulations or those of the Environmental Protection Agency. Also, the appraiser will look out for nearby sources of pollution and will want to be sure your supply is a safe distance from them.

You’ll have to sign a declaration that you’re aware of the status of your water supply. And that includes an acknowledgment of the need to maintain any filtration system or mechanical chlorinator that exists or is required.

Shared wells are okay providing they meet similar safe-and-adequate supply conditions. But there must be in place a fair and enforceable agreement with the other users over rights to supply and maintenance.

Some local authorities make connecting to the public water supply mandatory. If that’s the case where you are (and you can), you’ll have to.

Check your eligibility for a VA home loan. Start here.14. Individual sewage disposal

The same applies to your sewage system. If it’s possible, and the local authority says you must, you’ll have to connect to the public sewers.

If you can’t do that — or don’t have to — you can stick with the existing sewage system. However, that mustn’t create a nuisance or pose a threat to public health. If you’re putting in a new sewage system for any reason, it will have to conform with local health authority codes.

But what if all that exists is an outhouse? Perhaps surprisingly, that could be fine. It just has to be in an area where such facilities are “customary” (so probably not the Upper East Side of Manhattan) and it must comply with local health authority recommendations.

15. Community water supply and sewage disposal

Suppose the home you want to buy is in a homeowners’ association (HOA) area or a planned development. Sometimes, the HOA or a private company supplies water and/or sewage facilities.

The VA appraiser must note such an arrangement. And they must obtain documentary proof that water quality has been approved by relevant health authorities. Sewage must be processed in ways that stop it from being a threat to public health.

In the event that local or state authorities don’t monitor or enforce compliance, set rates and ensure swift resolution of issues, a trust deed will be needed. That’s a legal document that should ensure standards are maintained.

16. Hazards

You want your next home to provide a safe and healthy environment for its residents. And you don’t want it to be at risk from hazards that undermine its structural soundness or that spoil its occupants’ enjoyment of the property.

The VA feels the same way and will require the appraiser to let it know as quickly as possible if he identifies anything that threatens those.

17. Defective conditions

The VA minimum property requirements list some defective conditions that could block your loan approval:

- Construction defects

- Poor workmanship

- Continuing settlement (when soil shifts under the load of foundation structures)

- Too much dampness

- Leaks

- Decay

- Termite infestation

The appraiser will provide an appraised value of the home subject to repairs for these being carried out. But those repairs must fix the problem immediately and prevent recurrence as far as possible.

That appraised value should reflect the value the home will have after the repairs have been done. But you won’t get a VA loan till they’ve been completed.

18. Mechanical systems

The VA appraisal process is not a home inspection. If you want a full check of the structure and its systems (furnace, HVAC, appliances ...) you have to pay a specialist home inspector.

So the appraiser won’t normally check or test mechanical systems. However, they should normally note any obvious defects that suggest one fails to achieve the VA’s standards of being safe to operate and protected from destructive elements.

19. Heating

If the home is in an area with a mild climate, heating may not be needed. In other places, a heating system will be required that can maintain a temperature of at least 50°F in parts of the home that contain plumbing.

That may be a fireplace or space heater. But if either of those isn’t vented and isn’t electric, you’ll have to meet some conditions. The owner will need to call in a licensed heating contractor who must certify in writing that an approved oxygen-depletion sensor is in place. That must be up to the local building code or comply with the manufacturer’s recommendations.

There’s no requirement to have air conditioning, regardless of the local climate. But, if it’s installed, it must be operational. If it isn’t, the appraiser will value the home as if it’s working normally. But you won’t get your loan approved until it is.

20. Leased mechanical systems and equipment

Leased systems and equipment belong to someone else. So they can’t be included by the appraiser when she’s calculating the value of the home. This most commonly applies to fuel/propane storage tanks and energy generation systems based on solar panels, wind turbines or similar. If it’s leased, it doesn’t add value to the home.

Beware of leases that “encumber the title” (lessen your legal rights as the homeowner). Some power purchase agreements do that. Those might actually detract from the value of the home because they may make it more difficult to sell later.

21. Alternative energy equipment

Providing it’s not leased, alternative energy equipment may add value to the home. Solar, wind and geothermal all fall into this category. High-energy efficiency features can, too.

Your appraiser should bear these in mind when calculating the home’s value.

22. Roof covering

Don’t expect an appraiser to scramble over the roof. That’s a home inspector’s job.

However, an appraiser might spot defects either internally (through moisture in rooms or the attic suggesting leaks) or externally from the ground. If a roof’s leaking and already has three or more layers of shingles, all the existing shingles will have to be removed and a new layer laid.

Check your home buying options. Start here23. Attics

Again, it’s a home inspector’s job to get up into attics. Your VA appraiser probably won’t. They’ll view easily accessible areas but not others. And they won’t move insulation or the current owner’s possessions.

If they notice leaks or insufficient ventilation, they’ll value the home as if those don’t exist. But you’ll be told about them and you won’t get your loan till they’re fixed.

24. Crawl spaces

You’ve already guessed. It’s a home inspection’s job to enter crawl spaces and your home appraiser probably won’t do so.

But the appraiser should take a look from the access hatch. They’ll need to see that there’s adequate access to the space, that it’s clear of debris and that it’s properly ventilated. They’ll also want to be sure the gap between the (highest level of) ground and the floor joists provides enough space for maintenance work. And They’ll make sure there’s no worrying dampness or pools of standing water.

Those requirements are only important if it’s necessary to enter the crawl space in order to maintain or repair plumbing, ducts, and any other mechanical systems. If there’s no need ever to access the space, the home appraiser will just be looking out for adequate ventilation and an absence of excess moisture.

25. Basements

Again, dampness is the main issue here. But the appraiser will also look out for structural problems.

They’ll also look at the sump pump, if one’s installed. It needs to be safely hard-wired or plugged into a standard electrical outlet via a factory-fitted cord.

Check your VA home buying eligibility. Start here.26. Swimming pools

If a pool’s been winterized or is clearly not in use, the appraiser won’t normally deduct for repairs to the mechanical systems. Absent evidence to the contrary, they’ll generally assume they’re either working fine or will be cheap to fix.

Structural issues are a different story. If the appraiser spot large cracks or unstable sides, they can do one of two things: They can value the home as if the pool were sound but make it being properly repaired a condition of your getting your loan. Or, they can value the home as if it didn’t have a pool and make the filling in and making good (perhaps re-grading the yard) of the pool a condition of your getting a loan.

Proper above-ground pools (complete with a filtration system and decking) in good condition should usually be seen by the appraiser as adding value to the home. However, that applies only in areas where that type of pool is “customary and accepted in the market area.” In other words, if all the neighbors’ pools are swanky, in-ground ones, your above-ground pool may be seen as not adding value.

If your local authority sets standards for securing pools, yours must meet those. If the pool doesn’t, getting up to code will be added to your repairs list, and you won’t get your loan till it’s done.

27. Burglar bars

If burglar bars are fitted, each bedroom must have a quick-release mechanism on at least one window. The only exception is if there’s an exterior door from that bedroom that allows occupants to escape a fire easily. This is such an obvious safety consideration that you’re unlikely to object.

If quick-release mechanisms are not present or the home appraiser can’t confirm they work effectively, the removal of burglar bars will be added to your list of necessary repairs before you get your loan.

28. Lead-based paint

With standard, non-lead paint, the appraiser typically won’t take much notice of internal decoration. That counts as cosmetic. They may, however, require defective exterior surfaces to be repainted if damage may be being caused by weather.

When it comes to lead-based paint, the year 1978 is key here. If the home or any addition to it predates that year, then it may be assumed that the paint present is lead-based. The appraiser will identify any defective lead-based paint. And it will have to be remedied, regardless of cost.

It will need to be either entirely removed or covered and sealed. The former involves washing, scrubbing and wire-brushing to clear away any defective surfaces. And then the application of two coats of non-leaded paint.

Covering involves removing the paint and then covering with drywall, plywood or plaster. Only then can new paint be applied.

The VA takes this health threat very seriously. Not only will you not get your loan until the work’s completed, but an appraiser must later inspect the finished job to make sure it meets the required standards.

Check your eligibility for a VA home loan. Start here.29. Wood-destroying insects, fungus, and dry rot

This is more of a threat to the structure of the building than to human health. The VA appraiser will look out for evidence of an insect infestation (especially termites) as well as fungus and dry rot.

For termites, the appraiser will require an inspection by a specialist exterminator if there’s any evidence that they’re present or have been present. And any damage must be repaired before you can get your loan.

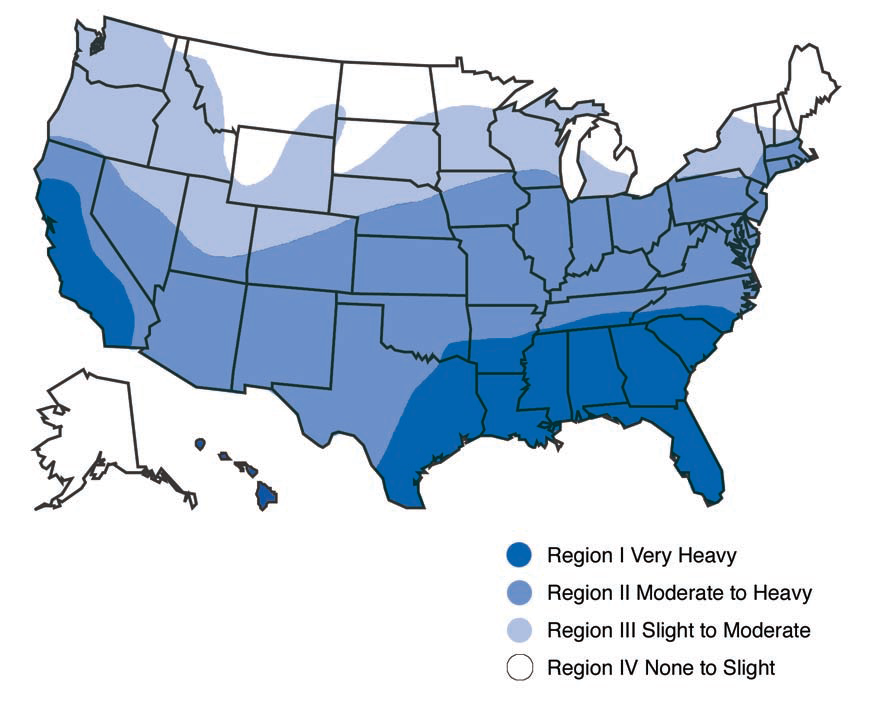

If the home is in an area designated “very heavy” or “moderate to heavy” on the following map, such an inspection will be required even if there’s no evidence of an infestation. If the property’s on the edge of one of those areas and you are unsure whether an inspection is required, you can get more localized information on the VA’s website.

Source: Relative hazard of subterranean termite infestations in the United States — USDA Forest Service

You probably won’t need an inspection if your home is a unit within a high-rise condominium. And they’re usually unnecessary for small, detached structures such as sheds, unless those count toward the value of the home.

30. Radon gas

Radon gas is an issue only if you’re buying a new home. In that case, the builder must certify that radon-resistant construction techniques were used. And that the home is up to all applicable codes for radon control.

31. Potential environmental problems

If there’s an actual or potential environmental problem, the appraiser must take its possible impact on the appraised value of the home into account. You may need state, local or federal authorities to certify in writing that there’s no issue.

If that’s refused because there is one, remedial work will have to be carried out before you’ll get your loan. The VA lists some examples of environmental problems, but there may be others:

- Oil and gas wells, whether operational or abandoned

- Underground storage tanks

- Chemical contamination (including methamphetamine, if you’re buying from a Walter White wannabe)

- Slush pits

- Soil contamination from sources on or off the property

- Hydrogen sulfide gas from petroleum product wells

32. Stationary storage tanks

The appraiser has to note the presence of any large storage tanks (1,000-gallon or bigger) within 300 feet of the property. That applies to buried (as in a gas station, for instance) and above-ground facilities. But only tanks containing flammable or explosive materials need to be reported.

If the tanks are likely to affect the value of the home, the appraiser must make the necessary deduction based on comparable sales nearby. And you, the military service member or veteran, will have to sign a document, acknowledging that you’re aware of the presence of the tanks.

33. Mineral, oil, and gas reservations and leases

There are two main threats from such leases. First, they may be an encumbrance, meaning they lessen your rights as the homeowner. And secondly, they may detract from the benefits you’d otherwise expect as a resident. In other words, they may make the home a less nice place to live.

The appraiser must assess how much either or both those affect the value of the property and adjust her appraisal accordingly.

Check your eligibility for a VA home loan. Start here.34. High-voltage electric transmission lines and high-pressure gas and liquid petroleum pipelines

High-voltage transmission lines and high-pressure gas and L-P pipelines require an easement. You’ll remember that’s a “legal right to trespass” and gives the line’s/pipeline’s owners certain rights. No part of the home nor any part of an addition (even a detached one) can be located within such an easement.

And, if the property is within 100 feet of one of these easements, the appraiser must mention it in his report.

35. Properties near airports

Your VA appraiser will know about the different noise- and accident-potential zones around a nearby airport. You can look them up on the FAA’s website.

The appraiser must take into consideration the proximity of the property to the airport and its presence in a zone when assessing the value of the home. They should try to find comparable sales to guide them.

You won’t get a VA loan on a new home that’s going to be built in a “clear zone” (aka “runway-protection zone”), because those are located near the end of an active runway. If you want to buy an existing home there (even if it’s newly built) or in an accident-potential zone, you’ll have to sign a document confirming:

"I am aware that the property being purchased is located near the end of an airport runway and this may have an effect upon livability, safety, value and marketability of the property."

36. Manufactured homes classified as real estate

The VA will guarantee loans on manufactured (once called “mobile”) homes, but there are strict conditions. Most importantly, the home has to officially be designated as real estate — rather than a “chattel” (personal belonging) or vehicle. You may be able to change its designation, but it must be zoned correctly.

In addition, it must conform with the US Department of Housing and Urban Development’s HUD Manufactured Home Construction and Safety Standards. It should normally come with a certificate and tags that confirm this.

Other rules mean it must:

- Have a foundation that can bear the weight of the home and also resist strong winds

- Conform with local and state regulations

- Have a floor area of at least 400 square feet if it’s a single-width unit or 700 square feet if it’s double-width

If you’re buying a new unit that’s yet to be installed, you’ll have to provide various plans and specifications.

Read more about getting a loan on a manufactured home here.

37. Modular homes

Mainstream modular homes are built in a factory, transported to the site and then assembled on traditional foundations. Once completed, you can’t tell that they weren’t traditionally constructed (“stick-built” or “site-built”) homes.

In other words, they’re every bit as good as any other home — and sometimes better, because it’s easier to build well in a factory environment. For that reason, appraisers should value modular homes in exactly the same way as they would any other.

38. On-frame modular homes

On-frame modular homes are very different from mainstream modular homes. They’re closer to manufactured homes, having been built on a chassis. Again, they must be officially designated as real estate.

To get a VA loan on one, it must have:

- Had all its original running gear (wheels and axles) removed

- A crawl space, complete with a vapor barrier and permanent masonry skirting with adequate ventilation

- Access to that crawl space

- A permanent foundation to which it’s secured and that meets state and local requirements

You think that sounds a lot like a manufactured home? You’re right.

39. Home inspections and waivers

By now you’ll be aware of the limitations of home appraisals. Their principal purpose is to establish the market value of the home. And the appraiser needn’t be an expert in construction.

If you have concerns about aspects of the structure, whether mentioned in the appraisal report or not, you should probably arrange a home inspection.

And, if you request a waiver on any repairs listed in your appraisal report, you stand a better chance of making your case if you include an inspection report.

Finally, most VA minimum property requirements protect you every bit as much as they do the department. Try to view them that way rather than as bureaucratic nitpicking. You may be glad you did.

Options to buy a home that does not conform to VA MPRs

Home buyers who have fallen in love with a home that doesn’t comply with the VA MPRs may struggle to buy it with a VA loan. However, that doesn’t mean you won’t be able to at all.

Check your VA home buying eligibility. Start here.The good news is that you do have options to purchase a home that does not meet the VA minimum property requirements. It may just take a little extra work.

- The current owner may first need to carry out repairs to get the property over the MPR threshold

- You may need to buy the property with a bridge loan so you can carry out the necessary work before getting a VA loan. A bridge loan is simply an alternate, temporary loan type which you replace with a VA loan later

- In rare circumstances, you may be able to get a waiver from the VA for repairs. But you’ll need your lender on your side. The home must already be safe, sanitary and structurally sound. And there’s no obligation on the VA to issue any such waiver

Talk with your loan officer and real estate agent to explore your options.

Apply for a VA home loan

VA loans are a zero-down payment way to purchase a home with low closing costs and competitive interest rates. And despite the lengthy list of minimum property requirements above, most homes fall well within VA guidelines.

Check your eligibility and today’s VA loan rates at the link below.

Time to make a move? Let us find the right mortgage for you