NOTE : FHA mortgage guidelines are subject to change. The information below may be outdated.

For the second time in 4 months, the FHA is changing the way it charges mortgage insurance. The change is forcing homeowners and home buyers using FHA financing to make a choice — use the current system for FHA mortgage insurance, or to wait for the new one to take effect?

The answer roots in mathematics, but first, some FHA background.

Click here to get an FHA mortgage rate quote

.

How FHA-Insured Mortgages Work

Most people forget — the FHA is not in the business of making loans to homeowners. Rather, the FHA insure loans that lenders make to borrowers. The FHA puts out a set of guidelines says to banks that “so long as your borrowers meets these requirements, we will insure the loans you make to them.”

Now, banks don’t expect their FHA-backed loans to go bad, but when their loans default, the FHA steps in and makes payment on them similar to how any insurance-type company would operate. And, to fund these claims, the FHA uses its insured borrowers’ own money.

Homeowners backed by the FHA pay into the FHA insurance fund in two ways:

- With a one-time, upfront payment at closing called Upfront MIP

- With an monthly, pro-rated annual payment called Annual MIP

Mortgage insurance premiums kick off a lot of money and the FHA has been self-funded for years without issue. However, as FHA home loan defaults have climbed recently, so have insurance payouts to lenders. It’s put a ginormous strain on the FHA’s solvency.

For example, in September 2008, the FHA held $19 billion in reserves. Today, that number is $3 billion.

In the FHA’s own words, the groups reserves are “perilously low”.

Summarizing The FHA Mortgage Insurance Changes

As a means to help refill its coffers, therefore, the FHA is changing its upfront and annual mortgage insurance premium structure. It’s the second tweak of 2010 and the changes apply to FHA case numbers issued on or after October 4, 2010.

Under the updated mortgage insurance program, assuming a 30-year fixed rate FHA mortgage with at least 5 percent equity:

- Upfront MIP drops to 1.000% of the amount borrowed from 2.250%

- Annual MIP increases to 0.850% of the amount borrowed from 0.500%

For homeowners using an FHA-insured mortgage, the upfront cost of the loan will drop by a lot, but the long-term costs of the loan will grow.

Using a $200,000 mortgage as an example, upfront MIP falls to $3,000 from $7,750; monthly MIP jumps to $212.50 from $125.00. The FHA expects the change to yield an additional $300 million in premiums monthly.

Click here to get an FHA mortgage rate quote

.

Work The Change In FHA Premiums To Your Advantage

Homeowners wanting an FHA-insured mortgage should remember the October 4, 2010 implementation date.

If your FHA case number is assigned on, or after, that date, you will get the 1 percent upfront cost + the 85 basis points each year thereafter. If it’s assigned prior to, you’ll get the 2.25 percent + 50 basis points.

Or, simplified:

- Current system : Big upfront costs, low long-term costs

- New system : Low upfront costs, big long-term costs

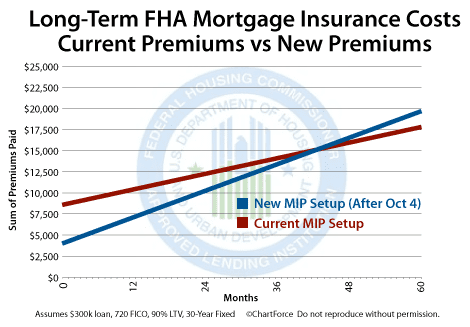

So which is best, then? It depends on your timeline.

The mathematical break-even point on the current FHA system versus the new one is Month 43. If you know you’ll sell or refinance in fewer than 3 years, 7 months, you should wait to start your mortgage application until after the October 4, 2010 changeover.

On the other hand, if this is your “last home for life”, give that application as soon as possible!

The math works for all loan sizes, too — from $75,000 all the way up to the FHA loan limits for your area.

Start Your FHA Home Loan Application Online

If you’re unsure of how FHA mortgage premiums work, or how the change will affect your payments, etc, ask for help.

Time to make a move? Let us find the right mortgage for you

.