Lower FHA Mortgage Insurance Premiums (MIP) Might Spur Refinancing

By any standard, 2016 was a very good year for the FHA. It was so good that lower FHA mortgage insurance premiums are very much in play for 2017.

We all talk about “FHA mortgages,” but in reality the FHA doesn’t make loans. According to HUD, the FHA is actually the “largest insurer of mortgages in the world, insuring over 34 million properties since its inception in 1934.”

Verify your FHA loan eligibilityHow FHA Mortgage Insurance Works

When lenders originate loans that meet federal standards, borrowers get FHA backing — mortgage insurance. That’s why you may qualify to purchase a house with just 3.5 percent down if your FICO score exceeds 579.

Why will lenders finance with so little down? Because with FHA insurance, the government covers the lender’s losses if you don’t pay your loan.

Now we’re suddenly talking about insurance and not mortgages, but hang in there for a moment and you’ll see how insurance costs can impact monthly mortgage payments.

To make the FHA program work, the government collects two types of insurance premiums.

Upfront And Annual Premiums

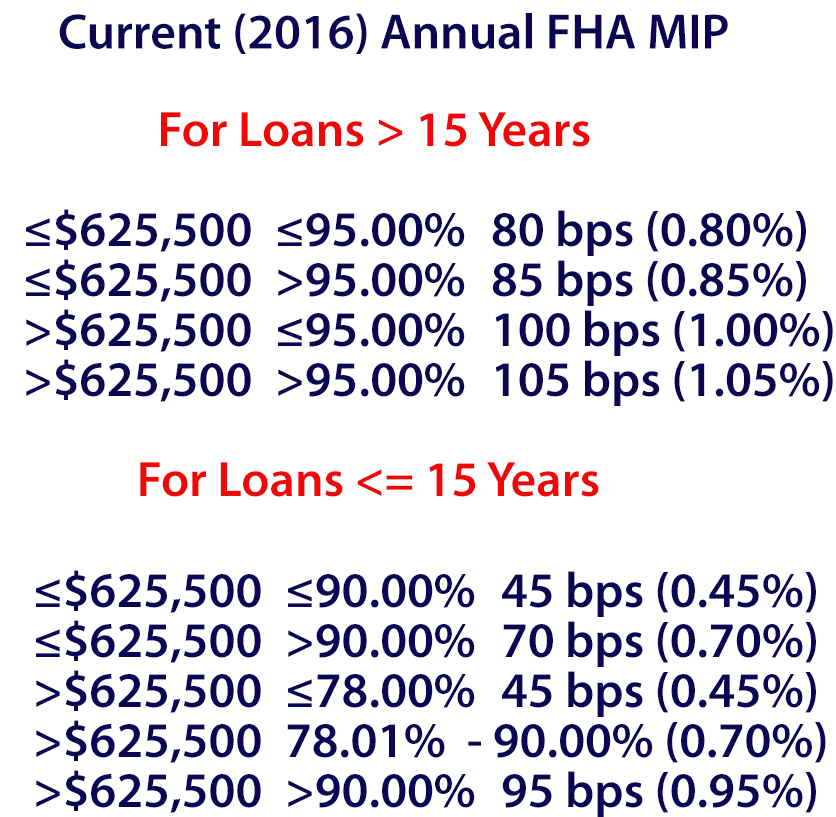

First, there’s an up-front mortgage insurance insurance premium (the upfront MIP) which now equals 1.75 percent of the loan amount. This sounds like a huge amount, but the good news is that you don’t have to bring that money to closing.

Instead, you can add it to the loan amount. Of course, a larger loan also means bigger monthly payments.

Second, there’s an annual mortgage insurance premium (the annual MIP). The premium for most borrowers now is .85 percent of the outstanding loan amount. To insure a $150,000 loan, you will pay about $106 a month. This amount drops each year as you pay down your loan balance.

The insurance premiums are collected to offset potential lender claims and the money is held in a reserve account known as the Mutual Mortgage Insurance Fund.

Congress says the FHA must have a cash reserve (the “capital ratio”) equal to at least two percent of its potential claims.

The FHA's Good News

It turns out that people love the FHA program, and the government has the numbers to prove it. More than 1.25 million FHA loans were issued in fiscal 2016, a period that ended September 30th.

Moreover, the reserve fund now has a 2.32 percent capital ratio. That’s more than 16 percent more than the 2.0 percent required by law.

You can see what’s coming next. If the reserves are piling up, then why not cut FHA premiums, lower borrower costs and finance more houses?

Will History Repeat Itself?

This is exactly what the FHA did at the start of 2015. It lowered the annual MIP from 1.35 percent to .85 percent. The result was nearly 330,000 additional loans.

So what about 2017? In an October news conference, HUD officials downplayed the possibility of any premium reductions for the coming year. That might have been the end of the discussion.

However, we will unexpectedly be getting a new crop of HUD officials as of January 20th.

The real estate industry surely wants to see FHA premium reductions. William E. Brown, president of The National Association of Realtors (NAR), said, “FHA can continue taking responsible steps to manage their risk even as they take action to make homeownership more affordable for lower- and middle-income buyers.”

“More affordable,” of course, is code for “We want lower FHA premiums.”

2 Reasons For Lower FHA Mortgage Premiums In 2017

In fact, there are two very strong reasons to suggest that FHA premium reductions may well take place in the coming year.

First, with a recovering housing market, the FHA is facing fewer claims. The higher premiums imposed to recover from huge losses of 2000 through 2009 are no longer needed.

Second, the FHA program is gushing with cash. It would be politically popular to cut insurance premiums. Home sales would be helped, and lower insurance costs would offset rising mortgage rates.

The goal of every new administration is to look better than the last one. Lowering FHA fees would be widely seen as a bold and pro-active step to pump up the housing market and help first-time and moderate-income borrowers.

As the old expression goes, what’s not to like?

What Are Today’s Mortgage Rates?

When looking at current mortgage rates, your mortgage insurance is also a facor if you out down less then 20 percent. Ask lenders for quotes including mortgage insurance if it applies to know. Understand also that your down payment and credit score affect your mortgage insurance rate as well as your mortgage interest rate.

Time to make a move? Let us find the right mortgage for you