Do you need 20% down to buy a house?

According to mortgage advisor Ivan Simental, that’s one of the most common questions first-time homebuyers ask.

“Twenty percent is a large down payment and can sometimes feel unrealistic and daunting,” Simental said on a recent episode of The Mortgage Reports Podcast. “If you’re trying to save a 20% down payment, that can be a bit scary at times.”

Fortunately, 20% down isn’t always necessary. Many home buyers today can qualify with as little as 5, 3, or even 0% down.

Simental says it’s important to weigh the pros and cons of a big down payment before putting it all on the line. Here’s what to consider before you buy.

Check your low down payment mortgage eligibilityListen to Ivan on The Mortgage Reports Podcast!

Is it best to put 20% down?

The right down payment size is personal. It depends on your home buying goals, your personal finances, and the local real estate market where you want to buy.

While you might think putting more money down is always better, that’s not necessarily the case. There are both pros and cons to making a 20% down payment.

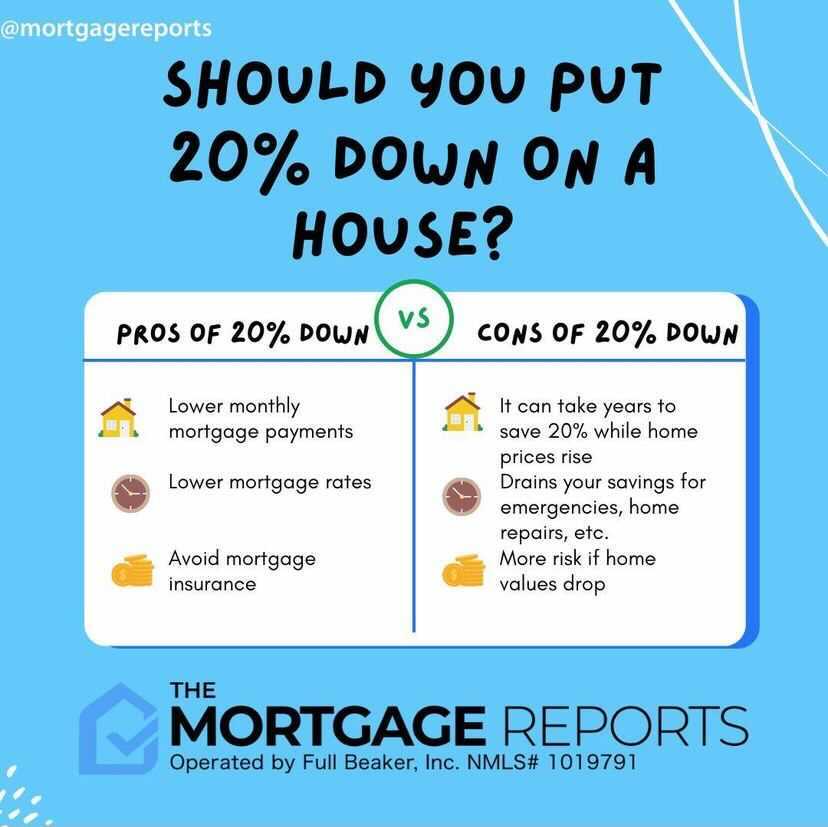

| Pros of 20% down | Cons of 20% down |

| Lower monthly mortgage payments | It can take years to save 20% while home prices rise |

| Lower mortgage rates | Drains your savings for emergencies, home repairs, etc. |

| Avoid mortgage insurance | More risk if home values drop |

Yes, putting 20% down lowers your home buying costs. Borrowers who can make a big down payment will save a lot over the life of their mortgage loan.

But a smaller down payment allows many first-time home buyers to get on the housing ladder sooner. They can start building home equity and reap the benefits of homeownership without waiting years to save 20% down.

Let’s dig into each of these pros and cons a little deeper.

Image: The Mortgage Reports Instagram

Pros of a 20% down payment

Lower monthly mortgage payments are the biggest perk of putting 20% down.

When you make a larger down payment, you have a smaller loan amount This means a lower monthly payment and less mortgage interest paid over the long haul.

Let’s look at an example:

- Say you’re buying a $200,000 house with a 30-year loan at a 3% interest rate

- If you were to make a 20% down payment, your payment would be just $675 per month

- With a 5% down payment, your monthly payment would jump to $800 — an extra $125 per month

Another benefit is that higher down payments typically mean lower mortgage interest rates.

The less money a homeowner borrows, the less risky their loan is for a mortgage lender. Lenders reward this lower risk with a reduced rate and lower long-term borrowing costs.

Finally, a 20% down payment lets you avoid mortgage insurance.

On conventional home loans, private mortgage insurance (PMI) costs about $30 to $70 per month, according to Freddie Mac. This can add up significantly over time.

Other low-down-payment mortgage loans, like the FHA and USDA programs, require mortgage insurance regardless of down payment size. Only VA loan borrowers are free of monthly mortgage insurance payments.

By putting at least 20% down on a conventional loan, home buyers can avoid this added cost and save thousands over the life of the loan.

Verify your home buying eligibilityCons of a 20% down payment

The biggest disadvantage of a large down payment is that it whittles down your savings — and the funds you have leftover for potential emergencies.

As Simental puts it, “If this 20% is your entire life savings, and you’re not going to have any more money for emergencies or that six-month cushion that a lot of people will tell you that you should have for an emergency fund, I would strongly urge you not to put 20% down.”

Another big drawback is that saving a 20% down payment can take years.

- Say you want to buy a $300,000 home

- 20% down requires $60,000 in cash

- If you save $500 per month, it will take 120 months to save $60,000

- That’s 10 years to save a 20% down payment!

Keep in mind, home values are likely to keep rising year over year. So the longer you wait on a 20% down payment, the higher that down payment amount gets.

For many people, then, saving 20% is simply not realistic.

Putting 20% down may also be a bad idea if you don’t plan to own the home long. For one, it lowers your rate of return once you sell. On top of this, it puts more of your money at risk should your home’s value drop.

Low down payment loan options

Fortunately, a 20% down payment isn’t your only option.

There are many loan programs that allow for much lower down payments. And as long as you can afford the monthly payment (and potential mortgage insurance) these loans come with, they could be a good choice for you.

Here’s how down payment requirements break down by loan program:

- FHA loans: Backed by the Federal Housing Administration, these loans require a minimum down payment of 3.5% if you have a 580 credit score or higher, and 10% if your score is 500-579. These loans require both a monthly and upfront mortgage insurance premium (MIP)

- USDA loans: These are loans for use in certain rural and suburban areas. If you’re buying a property in an eligible region, you’ll need zero down payment whatsoever. Credit score requirements typically start at 640

- VA loans: VA loans are mortgages backed by the Department of Veterans Affairs. If you’re a veteran or military member, you may qualify for this type of loan. Like USDA loans, they require no down payment at all

- Conventional loans: Conventional mortgage down payments go as low as 3% of the purchase price. That’s just $6,000 on a $200,000 house. The Fannie Mae HomeReady loan, Freddie Mac Home Possible loan, and Conventional 97 program all allow just 3% down

- Jumbo loans: Jumbo loans are required if you go above the conforming loan limit ($[currrent_loan_limits] in most parts of the U.S.). While many jumbo loans require 20% down, some lenders today offer them with as little as 10% or even 5% down

Another option? Look into down payment assistance programs in your local housing market.

Down payment assistance (DPA) can offer grants or loans to help cover your down payment and/or closing costs. These programs are typically offered by state and local governments as well as nonprofits.

Eligibility requirements vary, so check with your loan officer or real estate agent about DPA programs in your area.

The bottom line

Don’t let the idea of a big down payment scare you away from a home purchase.

“If you’re stuck on ‘Hey, I need this 20% down payment because that’s what I’ve been taught — that’s what I grew up thinking,’ then get that out of your head,” Simental said.

“You no longer need a 20% down payment to buy a house.”

If you find yourself questioning what down payment to make, reach out to a qualified mortgage loan officer. They can advise you on all your loan options, as well as the costs they’ll come with.

Time to make a move? Let us find the right mortgage for you