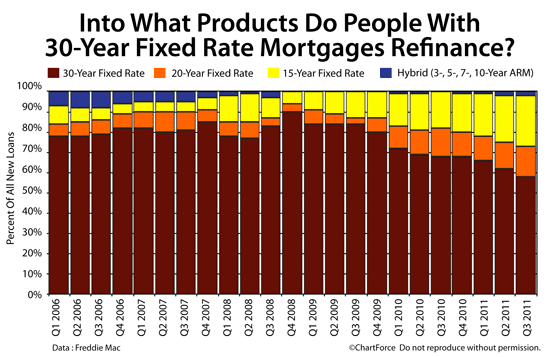

The 30-year fixed rate mortgage is less popular among refinancing homeowners.

Record-low mortgage rates are drawing refinancing households into shorter-term fixed-rate product such as the 20-year fixed-rate mortgage and the 15-year fixed-rate mortgage.

Click here to get mortgage rates

.

Demand For 15-Year Fixed Rate Hits 8-Year High

According to a Freddie Mac report, as conforming mortgage rates have dropped nationwide, so has the average mortgage loan term.

Of all Freddie Mac-to-Freddie Mac refinances last quarter, 40% of refinancing homeowners who started with a 30-year fixed-rate mortgage transitioned into loans of shorter-term loan, led by the 15-year fixed-rate mortgage.

Not since 2003 have homeowners abandoned 30-year fixed rate mortgages so quickly. And, it’s easy to understand why the 15-year fixed-rate mortgage is so popular, too.

As with other mortgage types, the conforming 15-year fixed rate mortgage rate made a bevy of all-time lows this year. Rates just kept dropping. The difference with the 15-year fixed rate mortgage, though, is that its rates are falling faster as compared to its peers.

Check this mortgage rate difference between the 15-year and 30-year fixed-rate mortgage :

- January 2000 - June 2011 : Average mortgage rate difference of 0.49%

- July 2011 - September 2011 : Average mortgage rate difference of 0.82%

Today’s 15-year fixed-rate mortgage is “on sale”. Homeowners — from San Francisco, California to Arlington, Virginia— know a good deal when they see one.

Click here for a 15-year fixed rate mortgage quote

.

Is The 15-Year Fixed Rate Payment Too Expensive?

As homeowners switch into 15-year fixed rate mortgages, they’re faced with a trade-off.

They get lower mortgage rates, but higher monthly mortgage payments. This is because, with a 15-year fixed-rate mortgage, monthly payments are compressed over a shorter period of time as compared to a 20-year or 30-year fixed rate loan.

At today’s rates, a 15-year fixed-rate monthly mortgage payment is 48% higher as for a comparable 30-year fixed-rate loan. That’s true for all loan sizes.

Now, 48% more may seem like a much bigger payment each month (and it is!), but remember that with a 15-year fixed rate mortgage, over the life of the your loan, you’ll pay total interest costs to your lender equal to about 26% of your original starting balance.

By contrast, with a 30-year fixed rate mortgage, your long-term interest costs are roughly 71% of your original starting balance.

In other words, at today’s mortgage rates, for every $100,000 borrowed, with a 15-year fixed rate mortgage, you’ll save $45,000 in interest costs over the life of your mortgage as compared to a 30-year fixed rate mortgage.

That’s major.

Get A Mortgage Rate Quote For Your Loan

Whether you have an adjustable-rate mortgage, 30-year fixed rate loan, or otherwise, it’s a great time to at least consider shortening up your loan term. There’s short-term pain in the form of higher monthly payments, but the loan-term gains are palpable.

Time to make a move? Let us find the right mortgage for you

.