NOTE : FHA mortgage guidelines change frequently. Relevant updates are posted to https://themortgagereports.com/fha-most-recent-updates. Information below may be outdated.

You can’t always believe what you read in the papers. Especially with respect to mortgages. Lending guidelines change fast — too fast for beat writers to keep up. The result is that papers sometimes publish out-of-date information.

It could be costing you thousands, too.

Click here to get a rate quote

.

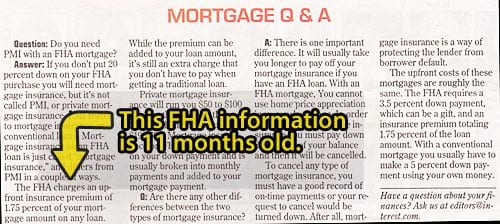

Newspapers Don't Track FHA Guideline Change(s)

Newspapers are losing revenue; closing, shrinking, and consolidating along the way. Profits are pressured. So, as one way to lower their costs, editors are increasingly replacing experienced beat writers with “syndicated” articles.

Syndicated articles are typically well-written pieces of content, addressing common topics clearly and plainly. And they’re plentiful. Editors can select from a pool of content and publish as-needed instead of keeping paid writers on-staff.

Syndication can be a great page-filling strategy, but following a path like that requires care. What was written last year is not always applicable today. And editors have to know the difference.

With respect to mortgages, unfortunately, they tend to not to. The syndicated article at top is 11 months — and 2 FHA guideline changes — behind-the-times.

The newspaper is giving bad information.

Click here to get a rate quote

.

The Story On FHA Mortgage Insurance Premiums

The FHA does not make loans to homeowners. Instead, it insures loans that lenders make to borrowers.

Here’s how it works.

The FHA prints a rulebook of income guidelines, asset guidelines, etc, and tells banks “so long as your borrowers meet the requirements in this rulebook, we will insure the loans you make against defaults.” If the loans default, the FHA then repays the banks’ claims using an insurance coffer that is self-funded by said borrowers.

The FHA’s insurance is officially “mortgage insurance premium” — often abbreviated as MIP. This is as compared to “private mortgage insurance”, or PMI, the type of insurance required on certain conventional, non-FHA loans.

FHA mortgage insurance premiums are collected in two parts.

- Some percentage of the loan size paid up-front at closing, paid by all borrowers.

- Some percentage of the loan size, paid monthly, paid by all borrowers.

And this is where syndication gets it wrong.

The snipped article incorrectly says the FHA’s upfront MIP is one-point-seven-five percent. That was true in 2010. Today, the upfront MIP payment is lowered to 1.00 percent — a steep discount from what borrowers used to pay. You wouldn’t know that from the article.

Furthermore, the piece omits the FHA’s changing monthly MIP.

As of April 18, 2011, every new FHA borrower faces a 0.25% increase to their monthly MIP. This increase is universal, and includes homeowners with the combination of a 15-year fixed mortgage and LTV under 90% for whom monthly MIP was previously $0.

Everyone pays the FHA’s monthly MIP now. That’s a really big deal.

Stay Up-To-Date On FHA Mortgage Guidelines

You can’t be expected to know when the papers are getting it right or wrong with respect to mortgages, so take the papers out of the equation. I update this website every day with news of the mortgage markets and changes coming down the pike.

Mortgage rates and mortgage markets change quickly and often. Unless you’re plugged in to the source, you’re probably just reading yesterday’s news.

Time to make a move? Let us find the right mortgage for you

.