Mortgage rates have dropped 9 weeks in a row, lowering conforming and FHA mortgage rates to bargain-basement levels, re-igniting the flames of last year’s Refi Boom.

But refinancing your mortgage is about more than just the rate. It’s about the costs, too. And high costs can negate the benefits of a refinance.

Verify your new rateWhat Are Mortgage Closing Costs?

Mortgage “closing costs” are fees paid to start a new mortgage; costs that wouldn’t be incurred if the mortgage never happened.

Closing costs can be grouped into two categories, labeled as:

- Origination/lender charges

- Third-party fees

“Origination Charges” are fees paid to the lender at closing; part of the lender’s bottom-line. Origination charges are often broken-down by line item and named things like underwriting fee, application fee and processing fee, for example.

Don’t get hung up on the semantics or nomenclature, though. Treat Origination Charges as a lump-sum figure. If it’s listed in the Origination Charges section on your Good Faith Estimate, it’s paid to the lender and that’s all that matters.

Different from Origination Charges are “Third-Party Fees”. Third-Party Fees are fees paid to parties other than the lender.

Third-party fees include the costs of appraisals, credit reports, settlement fees and government taxes. In general, they should usually be ignored when comparing mortgage offers to each other. This is because third-party fees tend to be fixed-fee line items; they’re 100% identical no matter which lender with which you choose to work.

Also, note that your Good Faith Estimate will include line-items such as Escrow Reserves and Per Diem Interest. These are not closing costs because they’re costs that would be incurred whether you gave the new mortgage or not. Escrow and per diem are “prepaid items” and don’t figure into a closing cost discussion.

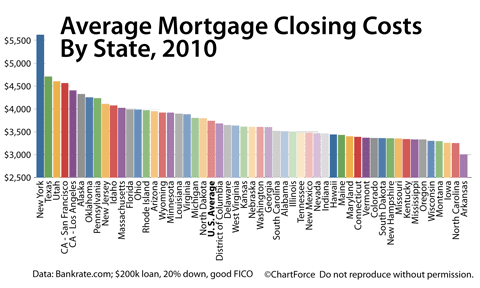

Mortgage Rates Are Falling; Closing Costs Are Not

Bankrate.com’s annual closing cost survey shows that typical mortgage closing costs are higher by 37 percent nationwide.

That’s a big (and costly) jump — especially in high-closing cost state like Texas. The good part, though, is that closing costs can be negotiable, in some respects, and when mortgage rates are falling, it’s pretty easy to beat the bank.

Instead of paying closing costs yourself, ask your lender to pay them on your behalf. It’s called a “zero-cost mortgage”.

Here’s how a zero-cost mortgage works:

- You’re eligible for a certain mortgage rate. Let’s say 5.000%.

- Your closing costs are $3,741, the national average.

- You willingly accept a rate of 5.250%, higher than for what you’re eligible

- In exchange for you paying more mortgage interest each month, the lender agrees to pay your closing costs for you. You pay nothing.

So, a zero-cost mortgage is exactly what it sounds like — a mortgage for which you pay nothing. Loan sizes don’t increase and nothing is “rolled in” to your balance.

Click here to get a rate quote

.

The downside to a zero-cost mortgage is that your monthly payment will be higher, but usually it’s by a negligible amount relative to the sum of closing costs waived at the time of closing.

Here’s a rough guide to how much mortgage rates increase on zero-cost loans (and depending on your state):

- Less than $100,000 : Add 0.75% to the market rate for “zero-cost”

- $100,000-250,000 : Add 0.50% to the market rate for “zero-cost”

- $250,000-400,000 : Add 0.25% to the market rate for “zero-cost”

- More than $400,000 : Add 0.125% to the market rate for “zero-cost”

Zero-cost mortgages can be an excellent strategy in a falling interest rate environment. Zero-cost loans eliminate sunk costs and offer an immediate payback on your investment (of zero).

Apply For A Zero-Cost Mortgage For Instant Savings

When the future of mortgage rates is uncertain, going zero-cost is a sure thing but not every bank offers zero-cost mortgages.

Time to make a move? Let us find the right mortgage for you