Should you retire your mortgage before you retire?

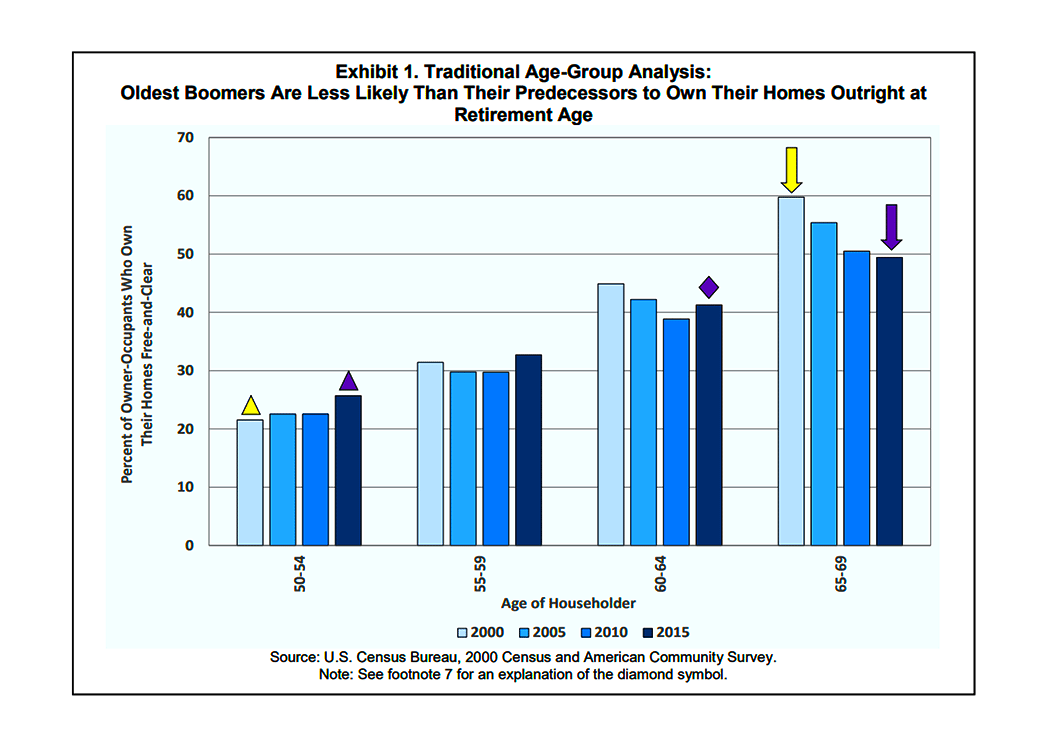

If you’re planning not to pay off your mortgage before retirement, you won’t be alone. Fewer than half of owner-occupiers in the age group 65-69 years were mortgage-free in 2015.

Verify your new rateWhat’s in and what’s out

That record-low number came from an October 2017 study by Fannie Mae. But the report revealed something even more surprising: Younger baby boomers, in the 50-59 years cohort, were actually more likely to own their homes outright than people the same age were in 2000.

In other words, the trend for carrying mortgages through into retirement may be losing ground. Fashions change. So, should you too be rethinking when to pay off your mortgage? It’s certainly a lively debate.

Why people retire with mortgages

There are two main reasons why people retire before paying off their mortgages:

- They have no choice — Especially following the Great Recession, many have seen their financial plans blown off course

- They strategically choose to keep their mortgages going — Some arguments for doing this to maximize wealth are compelling

Those in the first group can do little about their predicament. But those who choose keeping this debt in retirement might want to keep their decision under review.

When not paying down your mortgage makes sense

Does the end of your mortgage term happen to coincide with your retirement date? If not, paying down your loan by that deadline will mean paying more than your required monthly payment.

Here are some situations in which it’s often better to prioritize other things:

- If you have a pile of higher-interest debt — As a rule, you should pay down accounts with the highest interest rate first, and then work your way down to the lowest-interest account. That’s almost certainly your mortgage

- If you don’t have a good emergency fund — With medical expenses likely, you’re almost bound to need ready cash more in retirement than at other stages of life

- If you’re stinting on your 401(k) — If your employer is matching your contributions to your retirement fund, make sure you get the maximum benefit possible

Investment property mortgage rates: How much more will you pay?

- If you’ve a big mortgage and will be itemizing your tax deductions once you’re retired — Do the math

- If you’re planning on relocating or downsizing — Just pay off your mortgage as part of that transaction

- If you can get a better return on your money elsewhere — With mortgage rates so low (and generally tax-deductible) and markets so high, the chances of finding an investment where your cash will earn more are excellent

Most of those have been common sense for generations. But that last one has become more influential more recently. And that’s the one that needs thinking through.

First Law of Investment

What’s The First Law of Investment? If you Google it, you’ll find many learned suggestions. But here’s one used by some Wall Street insiders:

If God had not meant investors to be sheared, He would not have made them sheep.

5 home upgrades with the highest return on investment

That’s nasty, cynical and insulting. But it contains a kernel of truth: Few small, amateur investors can fully investigate stocks in which they invest. Nor can they track trends and changes in real time.

Large institutional investors with sophisticated automated trading are better positioned to protect themselves and react swiftly. Individuals can be left holding the bag when bad news erupts.

Forever blowing bubbles

Perhaps the first financial bubble happened in 1636-37 in the Netherlands. At one point, a single tulip bulb was worth the same as a house on an Amsterdam canal.

That sounds stupid now. But falling for the allure of a big shiny bubble has nothing to do with intelligence. In the 1720s, Sir Isaac Newton lost his shirt in the South Sea Bubble.

And bubbles have been a feature of capitalist economies ever since. The Great Depression followed one. The dot-com (or tech) bubble inflated between 1997 and 2000. A debt bubble burst in 2007-08.

Another bubble soon?

But there’s no reason to believe we’re all bubbled out. In June 2017, Forbes ran a feature under the headline, “The Next Recession: We Are Witnessing The Largest Twin Bubbles In History.”

Of course, alarmist predictions of economic doom are two-a-penny. But, after many years of booming stock markets, it’s easy to forget a simple fact: returns are a reward for risk. And the higher the reward, the greater the risk.

Risks in retirement

It’s one thing to take risks when you’re young or middle-aged. But, by definition, retirees are in a less strong position to recover from losses: They may have less time to do so. And they have fewer opportunities to earn enough to return to their previous levels of wealth.

Read this before tapping your 401(k) to buy a home

Of course, managing risk doesn’t mean avoiding it completely. If you spread your money across enough FDIC-insured certificates of deposit and savings and money market accounts, you can be pretty sure you won’t risk losing a cent. But you can be certain you’ll watch your wealth being whittled away by inflation year after year.

That’s why a diversified portfolio is so important in retirement. Mutual funds are one way to diversify your stocks and reduce your risk. Laddered CDs are another way to increase your earnings without risking your principal. You need enough salted away in safe investments to keep you afloat if your risky ones blow up.

Being mortgage-free is a safe investment

Paying down debt counts as an investment. True, you don’t get a positive return on your money. But the interest payments you save are just as real as any dividend or yield.

3 reasons to pay off your mortgage early (and 2 not to)

You have to decide whether paying off your mortgage before you retire fits within your diversified portfolio. Your return won’t be handsome if you do, especially if you’re going to itemize your tax deductions, but it would certainly count as one of your safe investments.

And, in the event of a depression, recession or economic meltdown, it could be one you’d value a great deal.

You still have options

Finally, paying down a mortgage doesn’t necessarily mean closing down your options. Providing you remain creditworthy, you could still likely borrow against your home with a new mortgage.

How to get a mortgage in retirement

Alternatively, you may prefer to borrow using a home equity loan or home equity line of credit (HELOC).

HELOC or fixed home equity loan? What’s best for you?

Reverse mortgages

And, of course, you could still borrow using a reverse mortgage or home equity conversion mortgage (HECM — a reverse mortgage backed by the Federal Housing Administration). You have to have cleared your original mortgage to be eligible for one of these. However, you can use some of the proceeds from the new loan to pay off any small balance on that original one.

HECM reverse mortgages: Who should consider them?

That opens the possibility of being free of mortgage payments, while still borrowing through a mortgage. And that’s something you may find attractive. Just be sure you understand all the potential disadvantages before you commit.

Take advice

Nothing’s certain in this world. That’s why there are no automatically correct answers to retirement planning. It all depends on your resources, your needs and your appetite for risk.

And that’s why it’s usually a good idea to seek advice for that planning from a reputable, independent professional. Just be sure you and she are on the same page when it comes to risk management.

What are today’s mortgage rates?

Today’s mortgage rates can impact your decision to carry a mortgage into retirement. With rates as low as they are, paying off the loan offers a smaller benefit. However, the decision to retire with or without a mortgage is very personal, and everyone feels differently about risk. In the end, it’s you who has to sleep at night.

Time to make a move? Let us find the right mortgage for you