How Much Do Mortgage Lenders Make From Your Loan?

One thing most consumers can agree on is that mortgages are not cheap.

The typical origination fee, one percent of the balance, can come to thousands of dollars.

There may be risk-based surcharges for those with low credit scores, small down payments, or riskier properties like high-rise condos or manufactured homes.

In addition, there are usually expenses for third party services like home appraisals, title insurance, escrow officers and home inspection.

If you feel as though everyone is making a ton of money from your home purchase or refinance, it’s understandable.

But not necessarily true.

Verify your new rateMortgage Lender Costs

The slew of new mortgage regulations and consumer protections, while generally regarded as a positive thing for the industry, did increase lender costs. Banks, brokerages and non-bank originators implemented new procedures and hired more personnel to comply with new rules.

Debra Still, President of Pulte Mortgage, claimed in a recent presentation that in 2006, the average loan file had 302 pages. Now, the average mortgage file (book?) is 806 pages.

This caused the cost of originating a new home loan to increase by an average of $210, upping the total cost to over $7,700 per mortgage.

Mortgage Lender Profits

By the end of 2015, dealing with increased regulation, personnel costs, and loan buy-backs (foreclosures, etc.) had dropped lenders’ per-loan profit, according to the Mortgage Bankers Association (MBA), to $493 per loan.

However, as lenders got better at dealing with the new rules, and brought in new technology, costs came down again and profits rose — to an average of $1,686 per loan in the second quarter of 2016.

There is definitely money on the table when you shop for a home loan. But that money is under the lender’s control, not the loan agent’s.

Loan Officer Income

According to the US Bureau of Labor Statistics (BLS), the median pay in 2015 for loan officers of all kinds — commercial, consumer, and mortgage — was $63,430 per year. The lowest ten percent earned less than $32,870, and the highest ten percent earned more than $130,630.

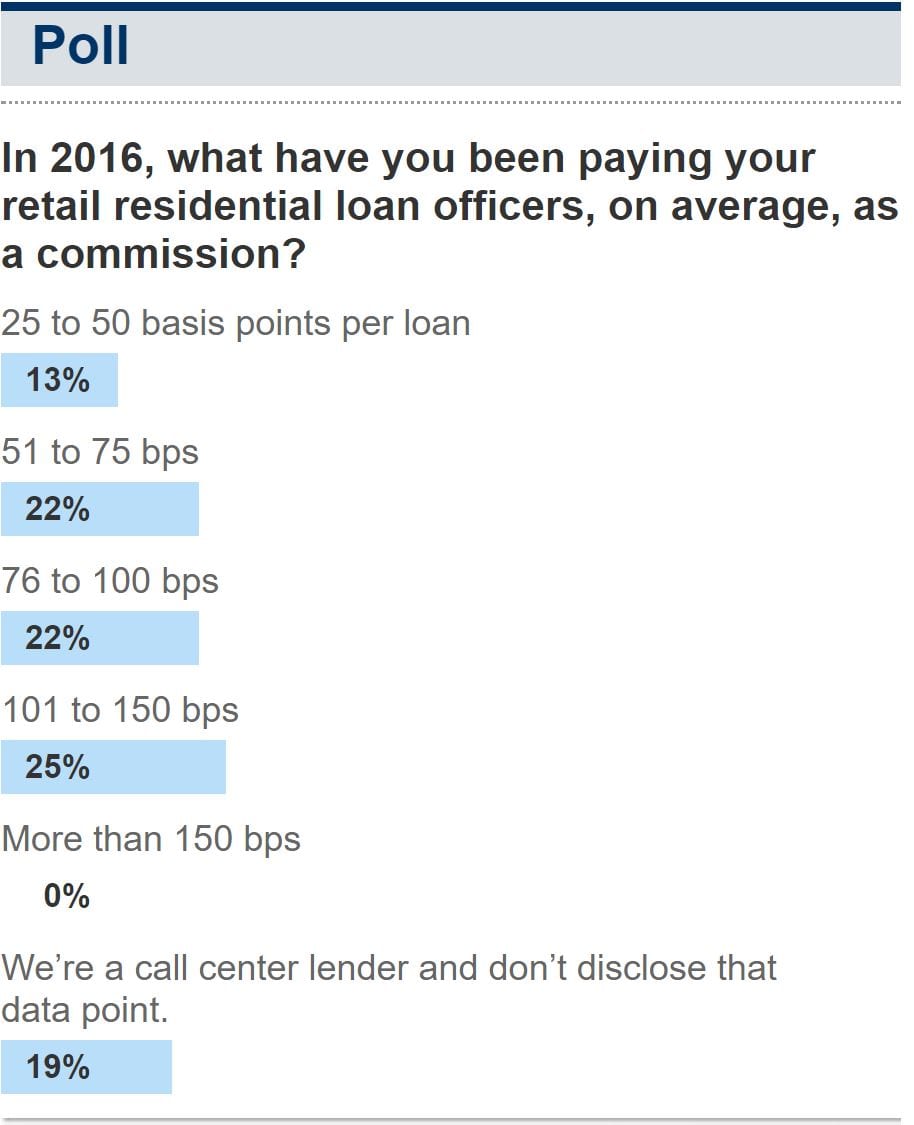

Loan agent compensation varies widely. Some receive a flat salary, but most are paid on commission. The poll results below from Inside Mortgage Finance show the range of commissions paid. Each basis point is 1/100th of one percent, so 25 basis points, or bps, equals 1/4 of one percent. That’s $250 for a $100,000 mortgage.

Working For Free

Most mortgage loan professionals work on commission. That means they may spend hours to work through loan scenarios for you, help you improve your credit score, pull your needed documentation together, complete your application, order title reports and verify your employment, assets and other pertinent details.

They don’t usually get paid if you decide not to buy or refinance, or the application is denied, or you change lenders. Working for free is a big part of this business.

Mortgage Commissions

Commissions vary between banks, brokerages and originators. What’s not allowed, however, is that the commission for your loan depend on the terms of the mortgage — no bonuses for giving you a higher rate, or bigger fee, and no penalties for cutting you a discount.

If loan agents want your business, they will offer you the best deal allowed by their employer – the mortgage bank or brokerage.

How To Negotiate The Best Mortgage Rate

When you shop for a home loan, compare offers from different competing lenders. There isn’t usually much to be gained by working over an individual loan officer and trying to beat a better deal out of him or her.

However, lenders are rarely allowed to reduce your fees slightly (“deviate,” as they say in the industry) under certain conditions. They may be allowed to do so in order to compete with another lender’s pricing, if they have a policy in place that meets guidelines established by the Consumer Financial Protection Bureau.

Second, any discount can’t be taken from the loan officer commission, except “to defray certain unexpected increases in estimated settlement costs.”

Fortunately, these days it’s easy to get a fistful of quotes online without putting on your boxing gloves.

What Are Today’s Mortgage Rates?

Today’s rates depend on lender efficiency, policy, desired profit margins and other factors. It really doesn’t matter what a lender’s policies are or how much it pays its loan agents. What matters is the bottom line deal it offers you.

Time to make a move? Let us find the right mortgage for you

![30-Year Mortgage Rates Chart [image]](/_next/image?url=https%3A%2F%2Fassets.themortgagereports.com%2Fwp-content%2Fuploads%2F2020%2F02%2F30-Year-Mortgage-Rates-Chart-image.jpg&w=3840&q=75)