Why Do Some Mortgage Lenders Require Flood Insurance?

Flooding is the most common natural disaster in the United States. In the most flood-prone parts of the country, most mortgage lenders won’t finance property unless the owners purchase flood insurance.

Even if your mortgage lender doesn’t force you to buy this coverage, however, you might want to consider it.

Flood insurance often covers you when your homeowners coverage doesn’t apply. But it comes with a cost.

In many cases, the cost is well worth protection for your largest investment.

Verify your new rateFlood Damage Is Not Covered By Homeowners Insurance

Homeowners insurance does not cover flood damage.

If a storm blows your roof off and rain ruins your rugs and furniture, homeowners insurance kicks in. But this only applies to damage from water originating from within your home or directly from the sky.

If water touches the ground before wrecking your house — from rivers, overflowing ditches, flash flooding, etc. — your regular home insurer is off the hook.

You can only get flood protection from a flood insurance policy.

Flood Insurance: Who Needs It?

You do, if your property is financed, and it’s in designated flood plain.

You might need it even if you don’t live in a flood plain. If a large part of your net worth is tied up in your house or its furnishings, you should definitely consider adding this protection.

An Insurance Information Institute study found that more than one-fifth of claims for flood damage came from people living in low-to-moderate risk areas – folks not required by lenders to buy flood insurance.

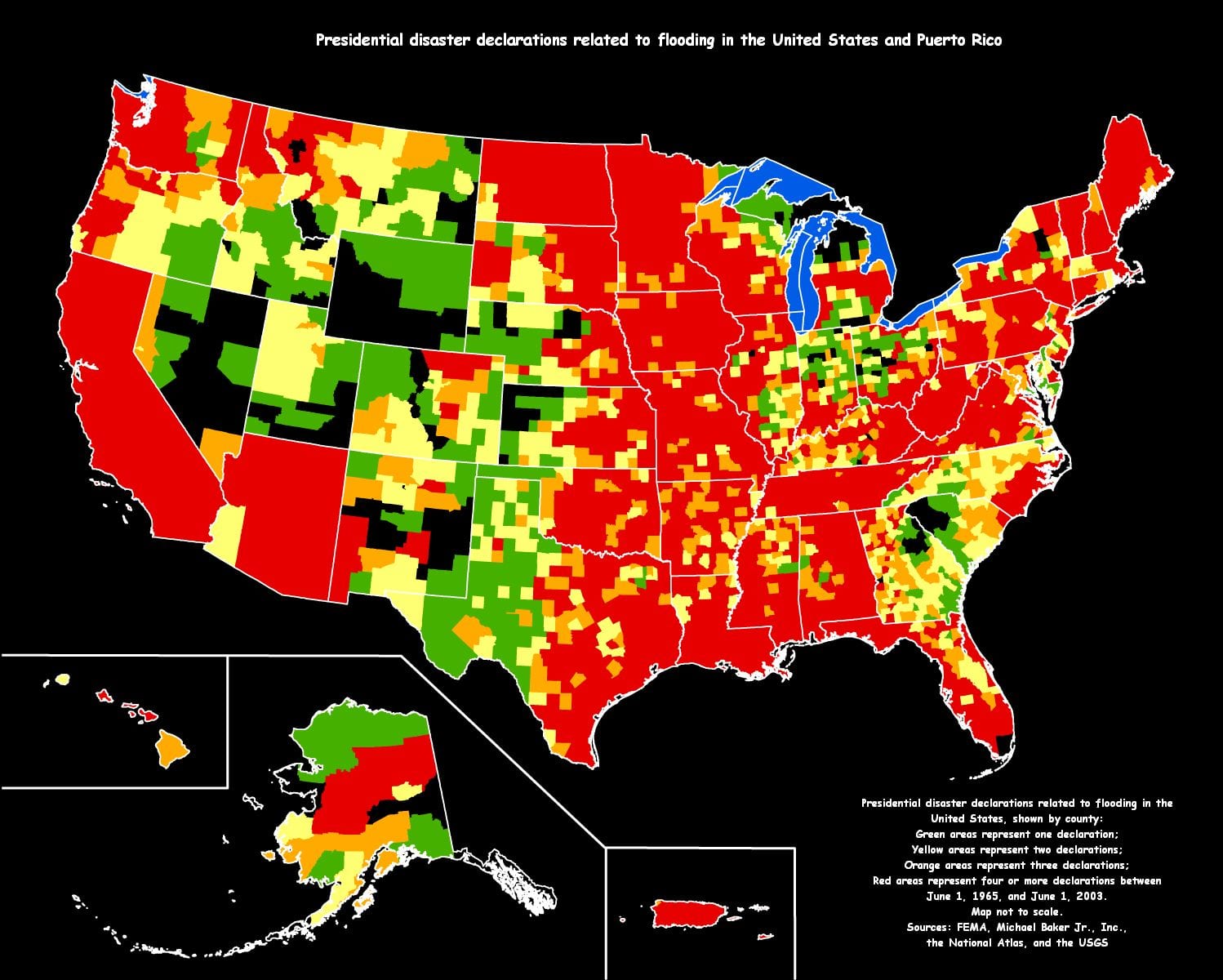

The National Flood Insurance Program’s web site says that for all practical purposes, “Everyone lives in a flood zone.”

The map below makes this very clear.

What about disaster relief from the government? That’s usually a low-interest loan, which must be paid back.

How Does Flood Insurance Work?

National flood insurance is a government program, and policies are sold only through licensed insurance agents. Flood insurance rates do not vary between insurers.

You can insure your dwelling for up to $250,000, and its contents for up to $100,000. That’s the limit for government policies, but private insurers can sell you extended coverage.

Flood insurance has a deductible. You can choose a higher one to get a lower premium. However, if coverage is required by your mortgage lender, it may set a maximum allowable deductible for its own protection.

It’s important to know that there is a 30-day waiting period for flood insurance; you can’t just buy it once a storm is heading your way.

Verify your new rateHow Much Does Flood Insurance Cost?

The cost of flood insurance depends on the property location — how high it is (or isn’t) above the 100-year flood level in your area.

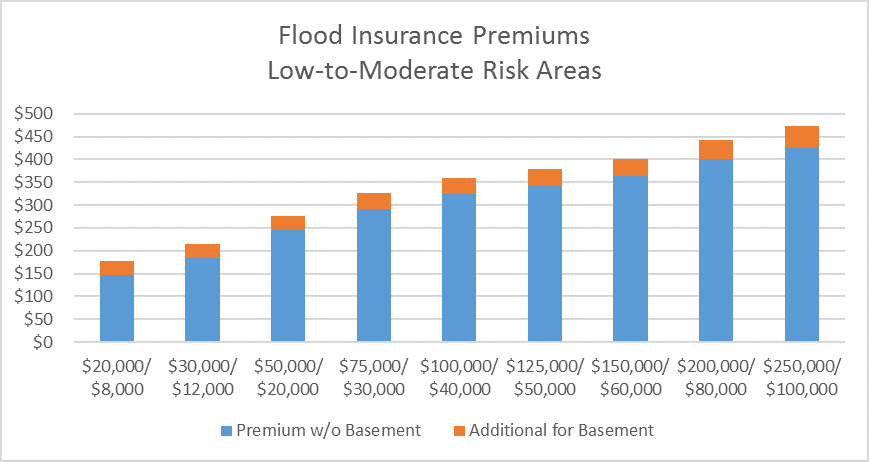

If you live in a low-to-moderate risk area, you’re eligible for a Preferred Risk Policy (PRP). The chart below shows these policy costs.

You can find your risk (and potential flood insurance cost) by entering your address into the flood risk tool provided by FEMA to see your local risk profile.

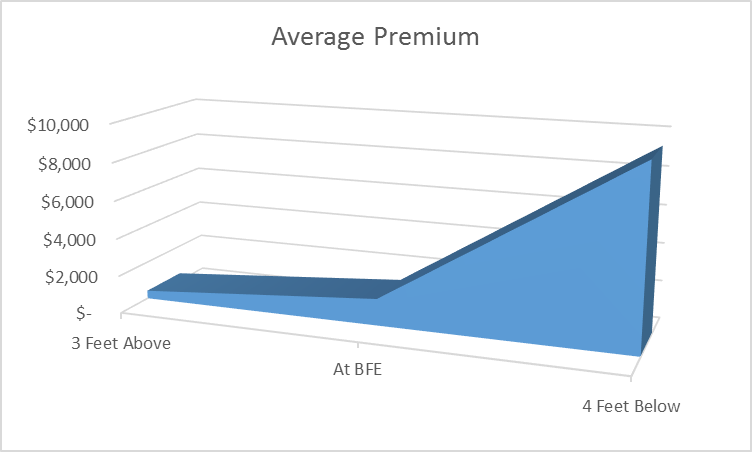

For those in high-risk areas, flood insurance is required by mortgage lenders, and the cost is not negotiable. You should consider this when you shop for real estate. The table below shows average costs in high-risk locations.

Areas at or above Base Flood Elevation (BFE) come with the highest premium. BFE is the “100-year flood” level to which flood waters have a one percent chance of rising in any given year.

Cost Of Not Having Flood Insurance

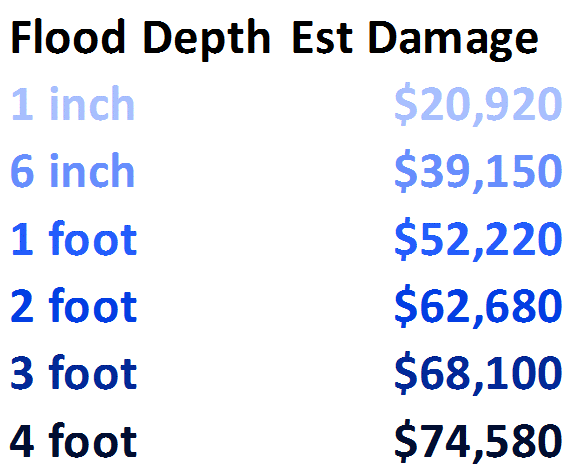

FloodSmart.gov has a really cool flood damage estimator tool that shows how much damage your home might incur at different levels of flooding.

This chart shows the estimated damage to a 2,000 square foot house for flooding between one inch and four feet:

According to the Insurance Information Institute, less than 13 percent of homeowners carry flood coverage, while one-third of all flood-related disaster assistance, which is provided to uninsured residents, went to those not in designated flood plains.

That’s a lot of people gambling with the biggest asset they own.

What Are Today’s Mortgage Rates?

Mortgage rates today are changing fairly often — moving up and down as lenders deal with market conditions.

To find your best rate today, be prepared to provide lenders with some basic information about the property and your credit rating, and they’ll tell you what’s available now.

Time to make a move? Let us find the right mortgage for you