Definition Of “Fair” Credit

There is no standard or legal definition of “fair” credit. The three major credit bureaus have not established any categories of credit score. However, many lenders consider scores between 620 and 679 to be in the “fair” range.

The median FICO score in the US is higher than “fair.” At 720, it’s considered “good.” So you’re in the lower half (but not by much) if you have fair credit.

Verify your new rateHow Much Can You Save By Improving Fair Credit?

Unless you pay in cash, your credit score affects the cost of everything you buy. Having fair credit can cost you significantly more than having good credit. Even though a good credit score (a FICO between 680 and 739) might be just a few points higher than yours.

Luckily for you, it’s not hard to add those points and move up a level.

The discount you get for having good credit depends on the type of financing you seek — mortgage, auto, credit cards or personal loans. Here are some of the differences in interest rates as of this writing.

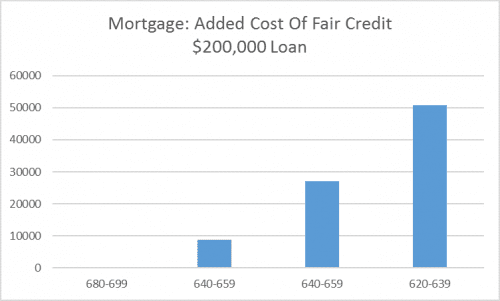

Mortgages

Currently, MyFICO says that those with fair credit can expect 30-year fixed-rate mortgage offers ranging from 5.06 percent to 4.09 percent, depending on their credit scores and the strength of their application.

Getting to 680, the low end of the “good” range, drops that rate to 3.87 percent. With a $200,000 loan amount, having good credit can save you between $8,800 and $51,000 over the life of the mortgage.

That’s quite an incentive to increase your credit score.

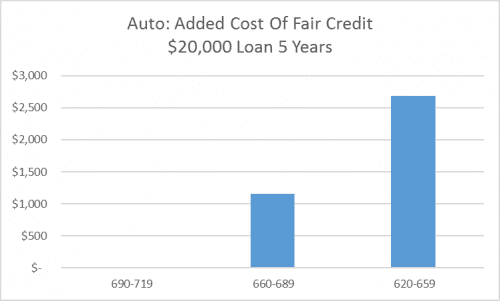

Verify your new rateAuto Loans

Car buyers with fair credit pay about twice as much interest as those with good credit. Thinking about financing a new car for 60 months?

MyFICO says that on average, auto borrowers with credit scores between 620 and 659 (the low end of “fair”) pay 9.4 percent. At the higher end (660 - 689), buyers pay 6.75 percent, and once they make the leap into “good” territory, they get 4.66 percent.

Credit Cards

When you finance a car or house, lenders can take back the car or house if you fail to repay them. But with credit cards, there is nothing securing the loan — except your promise to pay.

The better your credit score, the more likely it is that you’ll keep that promise. Because credit cards are unsecured, your credit score has an even greater effect on your interest rate.

Several online lists of credit card offers, as of this writing, showed rates between 20 and 29 percent for consumers with fair credit — about twice those offered to applicants with good credit.

Personal Loans

Like credit cards, personal loans are unsecured accounts. Your promise to repay is the only security the lender has.

Personal loans for people with good credit, according to one national peer-to-peer site, range between 12.74 and 15.99 percent. That’s a lot more favorable than the 16.99 to 21.49 percent offered to the next lowest tier.

Verify your new rateHow To Improve A Fair Credit Score

Your strategy for improving depends on the cause of your fair credit. Not all fair credit scores are the result of mismanaging debt.

Your score may be lower than average because you don’t use credit much, or because you’re young and have not had your accounts very long.

That’s a lot easier to fix than a low score resulting from missed payments, late payments, or too much debt.

Start With Your Free Report

So your first step is to get a copy of your credit report and FICO score, and check out the “reason codes,” which explain the biggest factors affecting your score.

You do this by ordering your report at the government’s site, annualcreditreport.com, and you can purchase your FICO scores for a small fee.

Don’t bother with other sites —there’s a reason their scores are called “FAKE-O” scores. Lenders use FICO scores almost exclusively, so that’s what you need to check.

Problem: Short History

If you’re fairly young and just beginning to use credit, you might see these reasons for your fair credit score:

- Account payment history is too new to rate

- Too few active accounts

- Date of last inquiry too recent

None of these is a serious problem. They can be fixed by using the accounts you have (so you have activity). Don’t carry balances, though, so you keep your utilization ratio low. Pay on time, every time, and your FICO will improve.

You need at least three accounts (“trade lines”) for many mortgage programs to use your credit score, and a mix — revolving accounts like credit cards and installment accounts like auto loans — increases your score faster.

If you want to speed up the process, and you’ve got nice friends or family with excellent credit, see if they’ll add you as an “authorized user” on an account or two.

Note: you don’t actually use the account. Their good payment history on that account will magically be added to your credit report and can help your score.

Too Much Credit

You may have the opposite problem — too much credit use. You’ll see reasons like these:

- Amount owed on accounts is too high

- Too many accounts with balances

- Number of revolving accounts

There’s a reason too much credit use is a red flag for lenders, and a reason for fair credit scores. Increasing account balances indicate that you spend more than you make, which can eventually lead to bankruptcy.

The good news is that if your payment history is good, your FICO can be raised quickly by paying down your balances.

Stop opening new accounts and pay your balances down as quickly as possible. People with good credit don’t use more than 25 to 30 percent of their available credit, while those in the fair range use 40 to 60 percent.

If you have accounts with small balances, try zeroing those out first, then work on paying down the others.

Derogatory Items

If your reason codes are some of these, you’ve got serious work to do.

- Delinquency on accounts

- Time since delinquency is too recent or unknown

- Frequency of delinquency

Late payments are a big deal to creditors and FICO systems because habitual late payers are statistically much more likely to default on loans.

According to FICO, a “good credit” consumer with a 680 score can drop 60 to 80 points with just one late payment (31 days past due).

FICO studied this in 2011 and found that it took about nine months to completely recover from a late mortgage payment (the most damaging type of late payment).

If you normally pay on time and have a good history with a creditor, you may be able to persuade them to erase a single late payment. It’s always worth a try.

If you’re habitually late, though, the black mark will likely stick.

Your score will come up eventually if you change your habits, but you need to stick with your plan. If you’re disorganized about bills, try setting up automatic payments.

Create and stick to a budget, so you have what you need when bills are due. And monitor your credit score. Seeing your score improve should give you all the incentive you need to take control.

What Are Today’s Good Credit Mortgage Rates?

While mortgage rates for fair credit are still highly affordable, moving up to “good” can shave more than half a percent from your interest rate.

Check with lenders and see what’s available to you now, and what you might save with just a few more FICO points.

Time to make a move? Let us find the right mortgage for you