Hope springs eternal for summer home buying

Making sense of the housing market is imperative when you’re trying to buy or sell a home.

History says seasonality plays a big role. The summer is typically a boom period, with borrower activity tending to rise alongside temperatures.

This is The Mortgage Reports’ State of the Housing Market. This quarterly feature will run through the latest trends of real estate’s major facets; including prices, sentiment, and inventory data.

Verify your home buying eligibility. Start hereAt a glance...

- U.S. home price growth slows, per CoreLogic

- For-sale listings make huge gains, per Realtor.com

- New construction mostly pointed up, per the Census Bureau and HUD

- Existing property sales stall, per NAR

- New home sales fall off, per the Census Bureau and HUD

- Home buyers getting rosy, per Fannie Mae

- Mortgage lenders are gaining confidence, per the MBA

- Home builders in holding pattern, per NAHB

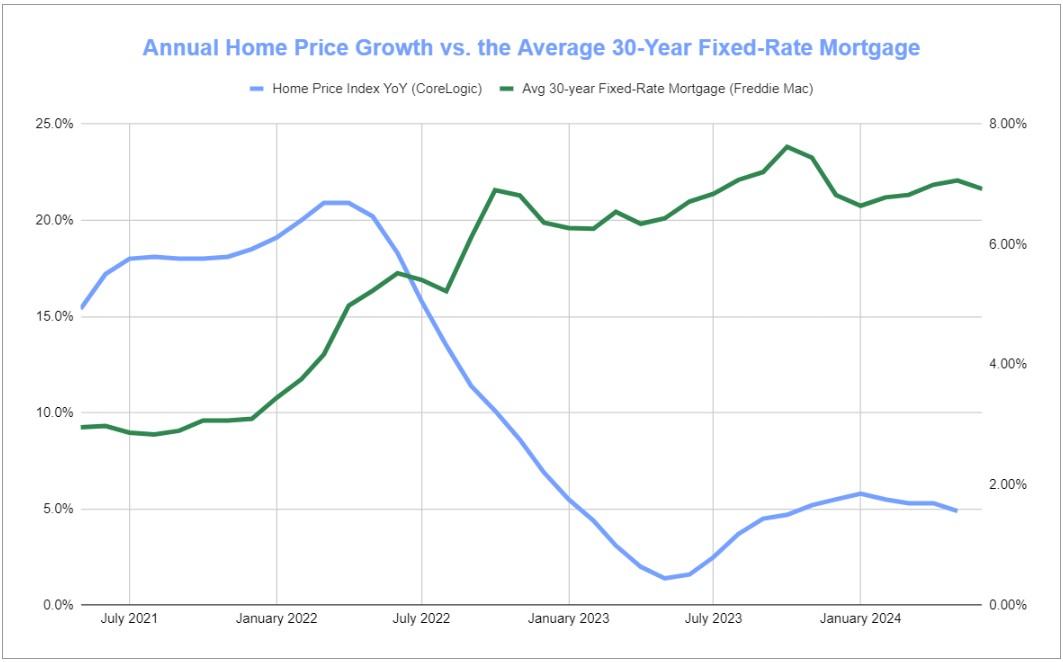

Home prices

Pandemic conditions drove property value growth to previously unseen levels. However, the rate of appreciation has normalized in recent times.

Single-family home prices rose 4.9% annually in May, according to CoreLogic’s Home Price Index. While it marked the 148th consecutive month of positive year-over-year growth, it was the lowest pace since October 2023. Additionally, prices inched up 0.6% month-over-month.

Check your home loan options. Start here“While national annual home price growth continues to slow as anticipated, cooling appreciation over the past months is now observed in more markets, as the surge in mortgage rates this spring caused both slowing home buyer demand and prices,” said Selma Hepp, chief economist at CoreLogic.

“However, persistently stronger home price gains this spring continue in markets where inventory is well below pre-pandemic levels, such as those in the Northeast. Also, markets that are relatively more affordable, such as those in the Midwest, have seen healthy price growth this spring. On the other hand, markets with notable inventory increases, including those in Florida and Texas, continue to see annual deceleration that is pulling prices below numbers recorded last year.”

At the state level, New Hampshire led the nation with a 12% annual gain. Rhode Island and New Jersey followed with increases of 9.8%. While no state experienced a year-over-year loss, Texas and Louisiana both had gains below 1%.

CoreLogic forecast a 0.7% increase in prices from May to June and a 3% bump by May 2024.

Housing inventory

The amount of available properties at a given time greatly impacts real estate dynamics.

A bountiful for-sale market benefits buyers, while tight supply swings the pendulum of advantage toward sellers. The ongoing inventory shortage is perhaps the biggest detriment to the overall market, as demand overshadows supply.

The latest listing data

June had 839,992 active listings, according to Realtor.com’s Housing Market Trends report. That number jumped 36.7% from June 2023 and 6.6% from May.

“While the quantity of homes on the market still trails pre-pandemic levels, home buyers are seeing more options to choose from as inventory increases,” said Danielle Hale, chief economist at Realtor.com. “The combination of more for-sale homes and longer time on the market is beneficial for home shoppers as they have more selection and don’t need to feel as rushed in picking a place to call home. Whether this translates into more home sales will likely hinge on how mortgage rates impact affordability in the second half of the year.”

Among the 50 largest metropolitan areas, Tampa, Fla., led the way with a 93.1% year-over-year increase in active listings. Orlando, Fla., Denver, San Diego, and Jacksonville, Fla., rounded out the top five, growing by 81.5%, 77.9%, 72.5% and 69.6%, respectively.

Conversely, Las Vegas had the only annual decline, falling 29.5%. Above it, New York and Rochester, N.Y., each gained 3.1%, then came 5.6% in Cleveland and 5.8% in Chicago.

The pipeline

For a look ahead, the Census Bureau and Department of Housing and Urban Development put together a joint Monthly New Residential Construction Report with three leading indicators of housing supply.

First, building permits hit a seasonally adjusted annual rate (SAAR) of 1.446 million in June. That grew 3.4% from May but fell 3.1% from June 2023.

Secondly, May housing starts reached a SAAR of 1.353 million. That rose 3% monthly while declining 4.4% yearly. Lastly, housing completions grew to a SAAR of 1.710 million, marking increases of 10.1% month-over-month and 15.5% year-over-year.

“With better inflation data, the Federal Reserve is expected to begin rate reductions later this year, and an improving interest rate environment will help buyers as well as builders and developers who are contending with tight lending conditions and high interest rates,” said Robert Dietz, chief economist at the National Association of Home Builders. “And with home inventory at a relatively low 4.4 months’ supply, builders are prepared to increase production in the months ahead. NAHB survey data of forward-looking builder sales expectations saw a gain in July.”

Home Sales

The frequency and summation of sold homes provide a picture for how the sector is performing. It can also tell a story of where demand stands compared to supply and affordability.

In June, a SAAR 3.89 million existing homes sold, according to the National Association of Realtors (NAR). This fell 5.4% both monthly and annually.

Check your home loan options. Start hereBroken down by price tier, $250,000-$500,000 existing homes accounted for 44% of sales. Among the country’s four major regions, the South led with a 45% share of sales, followed by 24% in the Midwest, 19% in the West and 12% in the Northeast.

“We’re seeing a slow shift from a seller’s market to a buyer’s market,” said Lawrence Yun, chief economist at NAR. “Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals, and inventory is definitively rising on a national basis.”

Sales of new homes also faded in June, according to the Census Bureau and HUD. These sales ran at a SAAR of 617,000, good for dips of 0.6% over May and 7.4% over June 2023.

On a year-over-year basis, new home sales rose 32.8% in the Midwest and 2.8% in the West. Meanwhile, the South and Northeast dropped 12.2% and 63.6%, respectively.

“Many potential buyers are remaining in a holding pattern due to elevated mortgage rates that averaged near 7% in June,” said Carl Harris, NAHB chairman. “However, moderating inflation suggests lower interest rates in the months ahead and that should bring more buyers off the sidelines.”

How are home buyers feeling?

The general consensus among house hunters can shape market competition.

More demand — especially when for-sale inventory is low — can create frenzied bidding wars and accelerate home price growth. When home buyer conditions aren’t opportune, borrowers may be able to get a relatively good deal on a property.

Verify your home buying eligibility. Start hereThrough a consumer survey, Fannie Mae’s Home Purchase Sentiment Index (HPSI) evaluates the overall view and outlook of the housing market through six components: Good time to buy, good time to sell, home price expectations, mortgage rate expectations, job loss concern, and household income. The index launched in 2011 and runs on a scale of zero to 100. It reached a high of 93.8 in August 2019 and a low of 56.7 in October 2022.

In June, the HPSI rose to 72.6, up from 69.4 month-over-month and 66 year-over-year. The share of respondents who said it was a ‘good time to buy’ had the largest gain, up a net five percentage points month-over-month.

“Affordability concerns remain the primary driver of consumer housing sentiment, even as the topline findings from our monthly survey showed a modest uptick in optimism on both homebuying and home-selling conditions,” said Mark Palim, deputy chief economist at Fannie Mae. “If mortgage rates decline through the end of the year, as we currently forecast, we do think home sales activity will pick up, but progress on that front is likely to be slow due to the ongoing imbalance between supply and demand.

How are lenders feeling?

Mortgage lenders constantly adjust their underwriting standards. Their willingness to approve and take on a home loan depends on both the borrower’s financial profile and the overall economic conditions at that point in time.

Find your lowest interest rate. Start hereWhen the economy runs hot, lender leniency tends to go up because those mortgages come with less risk. The opposite holds true during leaner times or recessions due to heightened uncertainty.

The Mortgage Bankers Association (MBA) measures this phenomenon with its Mortgage Credit Availability Index (MCAI). The MCAI has a baseline score of 100. Any score above that means lenders are more likely to extend credit while anything below indicates tighter standards.

The MCAI inched up from 94.1 in May to 95 in June and hovers around near-decade lows. In June 2023, the index sat at 96.6.

“Mortgage credit availability increased in June for the sixth consecutive month, as lenders expanded their offerings of cash-out refinance loan programs,” said Joel Kan, MBA’s deputy chief economist. “The recent growth in credit availability is encouraging, but the index is still hovering near 2012 lows. The jumbo index increased to its highest level since August 2022, but the conforming and government indices continue to indicate tight credit conditions, driven mainly by reduced industry capacity.”

How are home builders feeling?

Home builder sentiment ebbs and flows based on consumer demand, market conditions, shifting costs and supply chain status.

The National Association of Home Builders (NAHB) and Wells Fargo measure this sentiment on a 0-100 scale in their monthly Housing Market Index (HMI) survey. The survey is broken into three components: current home sales, home sales over the next six months and traffic of prospective buyers.

In July, builder confidence hit a score of 42, down from 43 in June and 56 in July 2023. It also reached the lowest point since December 2023.

“Though inflation is still above the Federal Reserve’s target of 2%, it appears to be back on a cooling trend. NAHB is forecasting Fed rate reductions to begin at the end of this year, and this action will lower interest rates for home buyers, builders and developers,” said Dietz. “And while home inventory is increasing, total market inventory remains lean at a 4.4 months’ supply, indicating a long-run need for more home construction.”

The bottom line

Whether you’re a buyer or seller, navigating the housing market can be a huge challenge.

While many real estate experts will tell you it’s never a bad time to buy a house as long as you can comfortably afford it, doing your homework can give you a leg up on the competition.

If you’re ready to start your journey of homeownership or sell your current property, reach out to a local mortgage professional today.

Time to make a move? Let us find the right mortgage for you