Why use an FHA loan?

FHA loans have been making homeownership more accessible for decades. Tailored to borrowers with lower credit, the FHA makes it possible to buy a house with a credit score of just 580 and only 3.5% down.

But home buyers aren’t the only ones who can benefit. For current homeowners, an FHA refinance may let you access low rates and home equity, even without great credit.

Not sure whether you’ll qualify for a mortgage? Check out the FHA program. You might be surprised.

Verify your FHA loan eligibility. Start hereIn this article (Skip to...)

- What is an FHA loan?

- Types of FHA loans

- FHA loan requirements

- FHA loan rates

- FHA loan benefits

- FHA loan alternatives

- FAQ

>Related: How to buy a house with $0 down: First-time home buyer

What is an FHA loan?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA).

FHA insurance protects mortgage lenders, allowing them to offer loans with low interest rates, easier credit requirements, and low down payments (starting at just 3.5%).

Thanks to their flexibility and low rates, FHA loans are especially popular with first-time home buyers, home shoppers with low or moderate incomes, and/or lower-credit home buyers.

But FHA financing isn’t limited to a certain type of buyer — anyone can apply.

Verify your FHA loan eligibility. Start hereHow does an FHA loan work?

The first thing to know about FHA mortgages is that the Federal Housing Administration doesn’t actually lend you the money. You get an FHA mortgage loan from an FHA-approved bank or lender, just like you would any other type of home mortgage loan.

The FHA’s role is to insure these mortgages, offering lenders protection in case borrowers can’t pay their loans back. In turn, this lets mortgage lenders offer FHA loans with lower interest rates and looser standards for qualifying.

The one catch — if you want to call it that — is that you pay for the FHA insurance that protects your mortgage lender. This is called “mortgage insurance premium” or MIP for the life of the loan or until the FHA home loan is refinanced into another type of mortgage. We go over this in detail below.

Types of FHA loans

FHA loans offer various options to meet different home buying needs. These government-backed loans are designed to make homeownership more accessible, especially for those with less-than-perfect credit scores or limited savings.

Each type of FHA loan is tailored to different financial situations and home buying needs. Here’s what you can expect.

Compare FHA loan quotes from multiple lenders. Start hereFHA mortgage loan

An FHA mortgage is ideal for first-time home buyers, requiring a minimum credit score of 580 for a 3.5% down payment. Those with credit scores between 500 and 579 can still qualify for a 10% down payment. These loans are popular due to their lenient credit score requirements and low-down payment options.

FHA rate-and-term refinance

An FHA refinance loan is suited for borrowers looking to improve their loan terms or lower interest rates, especially if their credit scores have improved since obtaining their original mortgage. It offers a way to adjust loan terms to better fit current financial situations.

FHA Streamline Refinance

For current FHA loan holders, the FHA Streamline Refinance provides an efficient way to refinance with minimal documentation and underwriting. It often results in lower interest rates and can potentially reduce mortgage insurance premiums. This option is advantageous for those who want to refinance without a complicated process.

FHA cash-out refinance

An FHA cash-out refinance allows homeowners to tap into their home equity, converting it into cash. It requires a minimum credit score of 620, and borrowers must leave at least 15% equity in their home after the refinance. It’s suitable for those needing extra funds for expenses or investments.

FHA Home Equity Conversion Mortgage (HECM)

HECM is a reverse mortgage for homeowners aged 62 and older, allowing the conversion of home equity into cash. It provides financial flexibility for seniors by enabling access to their home equity without selling the home.

FHA 203(k) loan

The FHA 203(k) loan is designed for home purchases requiring renovations. It combines the cost of the home and renovation expenses into one loan. Borrowers must meet specific credit score requirements and ensure that renovations are completed within six months.

FHA Energy Efficient Mortgage

This loan type allows borrowers to include energy-efficient upgrades in their FHA loan. It’s aimed at reducing utility costs and increasing the home’s environmental friendliness, thereby potentially increasing its value.

Section 245(a) loan

The Section 245(a) program is for borrowers expecting an increase in their income. It offers a graduated payment schedule that starts low and increases over time, aligning with anticipated income growth. This loan is particularly beneficial for young professionals expecting career advancement.

Check your FHA loan eligibility. Start here

FHA loan requirements

Homeownership can be a liberating experience, especially for first-time buyers. With their flexible guidelines and government backing, FHA home loans provide a welcoming path.

Understanding FHA loan requirements can make the process much easier, opening the door to a future in your ideal home.

Check your FHA loan eligibility. Start hereTo be eligible for an FHA loan, applicants must adhere to specific guidelines:

- The property must undergo a home appraisal by an FHA-approved appraiser.

- The property must serve as the applicant’s primary residence; investment properties and second homes are not eligible.

- Occupancy of the property is required within two months following the closing.

- A mandatory inspection is conducted to ensure the property meets FHA’s basic standards.

There are a few more specific conditions to qualify, such as a down payment amount, mortgage insurance, credit score, loan limits, and income requirements.

FHA loan down payment requirements

FHA loans require a minimum down payment, which varies based on credit score. For credit scores of 580 and above, a minimum down payment of 3.5% is required. Borrowers with credit scores between 500 and 579 must make a 10% down payment.

FHA mortgage insurance premiums

FHA mortgage insurance premium (MIP) is what makes the FHA program possible. Without the MIP, FHA-approved lenders would have little reason to make FHA-insured loans.

There are two kinds of MIP required for an FHA loan. One is paid as a lump sum when you close the loan, and the other is an annual premium, which becomes less expensive each year as you pay off the loan balance:

- Upfront Mortgage Insurance Premium (UFMIP) = 1.75% of the loan amount for current FHA loans and refinances

- Annual Mortgage Insurance Premium (MIP) = 0.55% of the loan amount for most FHA loans and refinances

MIP is split into monthly payments that are included in your mortgage payment. You’ll have to pay FHA insurance for the life of the loan or if you refinance into another type of mortgage loan.

The good news is that, as a homeowner or home buyer, your FHA loan’s MIP rates have dropped. Today’s FHA MIP costs are now as much as 50 basis points (0.50%) lower per year than they were in previous years.

Also, you have ways to reduce what you’ll owe in FHA MIP.

Depending on your down payment and loan term, you can reduce the length of your mortgage insurance to 11 years instead of the entire loan.

| Loan term | Original down payment | MIP duration |

| 20, 25, 30 years | Less than 10% | Life of loan |

| 20, 25, 30 years | More than 10% | 11 years |

| 15 years or less | Less than 10% | Life of loan |

| 15 years or less | More than 10% | 11 years |

Or, you could refinance out of FHA MIP at a later date.

With FHA interest rates as competitive as they are today, refinancing could reduce your monthly mortgage payments and cancel your mortgage insurance premium if you have enough equity in the home.

Check your FHA loan rates. Start hereFHA loan credit score minimums

The minimum credit score requirement for an FHA loan is 500. However, a score of 580 or higher allows for a lower down payment. Credit scores directly impact loan terms and down payment amounts.

Debt-to-income ratio

FHA loans consider the borrower’s debt-to-income (DTI) ratio, a measure of monthly debt payments against monthly income. The FHA prefers a DTI ratio of no more than 43%, though exceptions can be made for higher ratios with compensating factors.

Income and employment requirements

There is no specific income threshold for FHA loans, but borrowers must demonstrate steady employment history. Verification includes pay stubs, W-2s, tax returns, and bank statements.

FHA loan limits

Loan limits for FHA loans vary by county. However, starting January 1, 2024, the new FHA loan limit will be $498,257 for a single-family home in most parts of the country. Limits increase for 2-, 3-, and 4-unit properties.

FHA loan rates

Interest rates for FHA loans are competitive and can vary based on factors such as prevailing market rates, borrower’s credit score, income, loan amount, down payment, and DTI ratio. Government backing often enables lenders to offer lower rates compared to conventional mortgages.

Compare your FHA loan rates from multiple lenders. Start hereToday’s rates for a 30-year, fixed-rate FHA loan start at % (% APR), according to The Mortgage Reports’ daily rate survey.

Thanks to their government backing, FHA loan rates are competitive even for lower-credit borrowers. But interest rates can vary a lot from one lender to the next, so be sure to shop around for your best offer.

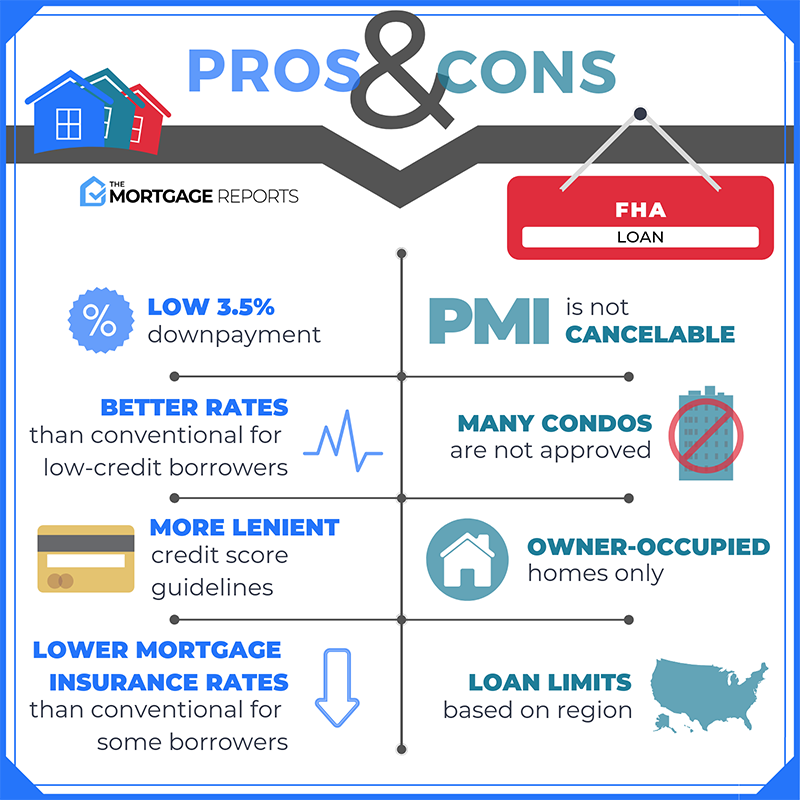

FHA loan benefits

Check your FHA loan eligibility. Start here1. Lower down payment: Just 3.5 %

For today’s home buyers, there are only a few mortgage options that allow for down payments of 5% or less. The FHA loan is one of them.

With an FHA mortgage, you can make a down payment as small as 3.5% of the home’s purchase price. This helps home buyers who don’t have a lot of money saved up for a down payment along with home buyers who would rather save money for moving costs, emergency funds, or other needs.

2. FHA allows 100% gift funds for the down payment and closing costs

The FHA is generous with respect to using gifts for a down payment. Very few loan programs will allow your entire down payment for a home to come from a gift. The FHA will.

Via the FHA, your entire 3.5% down payment can be a gift from parents or another family member, an employer, an approved charitable group, or a government homebuyer program.

If you’re using a down payment gift, though, you’ll need to follow the process for gifting and receiving funds.

3. FHA loans allow higher debt-to-income ratios

FHA loans also allow higher debt-to-income ratios.

Your debt-to-income ratio, or DTI, is calculated by comparing two things: your debt payments and your before-tax income.

For instance, if you earn $5,000 a month and your debt payment total is $2,000, your DTI is 40%.

Officially, FHA maximum DTIs are as follows.

- 31% of gross income for housing costs

- 43% of gross income for housing costs plus other monthly obligations like credit cards, student loans, auto loans, etc.

However, a 43% DTI is actually on the low end for most FHA borrowers. And FHA will allow DTI ratios as high as 50%. Although to get approved at such a high ratio, you’ll likely need one or more compensating factors — for instance, a great credit score, significant cash savings, or a down payment exceeding the minimum.

In any case, FHA is more lenient in this area than other mortgage loan options.

Most conventional mortgage programs — those offered by Fannie Mae and Freddie Mac — only allow debt-to-income ratios between 36% and 43%.

With down payments of less than 25%, for example, Fannie Mae lets you go to 43% DTI for FICOs of 700 or higher. But most people don’t get conventional loans with debt ratios that high.

4. FHA loans accept lower credit scores

Officially, the minimum credit scores required for FHA mortgage loans are:

- 580 or higher with a 3.5% down payment

- 500-579 with a 10% down payment

High credit scores are great if you have them. But past credit history mistakes take a while to repair.

FHA loans can help you get into a home without waiting a year or more for your good credit to reach the “excellent” level. Other loan programs are not so forgiving when it comes to your credit rating.

Fannie Mae and Freddie Mac (the agencies that set rules for conventional loans) say they accept FICOs as low as 620. But in reality, some lenders impose higher minimum credit scores.

5. FHA even permits applicants with no credit scores

What if an applicant has never had a credit account? Their credit report is, essentially, blank.

FHA borrowers with no credit scores may also qualify for a mortgage. In fact, the U.S. Department of Housing and Urban Development (HUD) prohibits FHA lenders from denying an application based solely on a borrower’s lack of credit history.

The FHA allows borrowers to build non-traditional credit as an alternative to a standard credit history. This can be a huge advantage to someone who’s never had credit scores due to a lack of borrowing or credit card usage in the past.

Borrowers can use payment histories on items such as utility bills, cell phone bills, car insurance bills, and apartment rent to build non-traditional credit.

“Not all lenders who are FHA approved offer these types of loans, so check with your loan officer individually,” cautions Meyer.

6. FHA loans can be up to $ in most of the U.S.

Most mortgage programs limit their loan sizes, and many of these limits are tied to local housing prices.

FHA mortgage limits are set by county or MSA (Metropolitan Statistical Area), and range from $ to $ for single-family homes in most parts of the country.

Limits are higher in Alaska, Hawaii, the U.S. Virgin Islands, and Guam, and also for duplexes, triplexes, and four-plexes.

7. FHA also allows extended loan sizes

As another FHA benefit, FHA loan limits can be extended where home prices are more expensive. This lets buyers finance their home using FHA even though home prices have skyrocketed in certain high-cost areas.

In Orange County, California, for example, or New York City, the FHA will insure up to $ for a mortgage on a single-family home.

For 2-unit, 3-unit and 4-unit homes, FHA loan limits are even higher — ranging up to $.

If your area’s FHA’s loan limits are too low for the property you’re buying, you’ll likely need a conventional or jumbo loan.

8. If you have an FHA loan, you can lower your rate with an FHA Streamline Refinance

Another advantage for FHA-backed homeowners is access to the FHA Streamline Refinance.

The FHA Streamline Refinance is an exclusive FHA program that offers homeowners one of the simplest, quickest, and most affordable paths to refinancing.

An FHA Streamline Refinance requires no credit score checks, no income verifications, and home appraisals are waived completely.

In addition, via the FHA Streamline Refinance, homeowners with a mortgage pre-dating June 2009 get access to reduced FHA mortgage insurance rates.

Verify your FHA loan eligibility. Start hereFHA loan disadvantages

What is the downside to an FHA loan? Among the numerous benefits of FHA loans, there are certain disadvantages that potential borrowers should be aware of. These drawbacks can impact the overall cost and flexibility of the loan.

Here are the downsides that you should know about FHA home loans.

FHA loan mortgage insurance premiums

One of the primary drawbacks of FHA loans is the mandatory mortgage insurance premiums. These include an upfront premium at closing, generally 1.75% of the loan amount, and ongoing monthly payments. This additional cost can make FHA loans more expensive over the long term

Loan limits

One notable limitation of FHA loans is the lower loan limits compared to conventional loans, which can be restrictive for higher-income buyers. The FHA mortgage limit for a one-unit property ranges from $ to $ for single-family homes in most parts of the country, which may not be sufficient in areas with higher property values.

Strict property requirements

FHA loans come with stringent property requirements. The purchased home must be the borrower’s primary residence and must meet specific safety and condition standards. This requirement can limit the types of properties that qualify for an FHA loan.

FHA loan alternatives

Alternative loans, like USDA and VA loans, offer distinct advantages, such as no down payment requirements, but come with specific eligibility criteria. Understanding these alternatives ensures you make a well-informed decision about the type of mortgage that’s right for you.

Conventional 97

The Conventional 97 program comes with a down payment requirement of just 3%. It stands out due to the absence of income limits and mandatory home buyer education, making it accessible to a broader range of homebuyers.

Check your conventional loan eligibility. Start hereHomeReady Mortgage by Fannie Mae

The HomeReady mortgage program is designed for low- to moderate-income families, allowing a home purchase with only a 3% down payment. Furthermore, this program permits the entire downpayment and closing costs to be covered by gifts or grants, offering significant financial flexibility.

Freddie Mac Home Possible

The Home Possible loan is notable for its reduced mortgage insurance costs compared to other similar programs. With a 3% down payment requirement and lower ongoing costs, Home Possible is an attractive alternative for those looking to save on mortgage insurance.

USDA loans

USDA loans, backed by the U.S. Department of Agriculture, are an attractive alternative, especially for moderate-income buyers in rural areas. They don’t require a down payment, which is a significant advantage. However, eligibility for USDA loans is restricted based on income and geographical limits, and not every property qualifies for this type of financing.

VA loans

VA loans are another viable alternative, particularly for U.S. military service members, veterans, and certain surviving spouses. Like USDA loans, VA loans also require no down payment. However, eligibility for VA loans is exclusive to the military community, limiting their accessibility to the general public.

FAQ: FHA loans

Yes, FHA loans offer both fixed-rate and adjustable-rate (ARM) options. A fixed-rate FHA loan provides a consistent interest rate and monthly payment for the life of the loan, ideal for those who prefer stability. An adjustable-rate FHA loan, on the other hand, has an interest rate that can change over time, typically offering lower initial rates.

FHA loans often have lower interest rates compared to many conventional loan options. This is largely due to the government backing of FHA loans, which reduces the risk for lenders. As a result, lenders are generally able to offer more competitive mortgage rates to borrowers. However, the actual interest rate you’ll receive on an FHA loan can vary based on several factors, including your credit score, loan amount, and the current market conditions. It’s always a good idea to compare rates from multiple lenders to ensure you’re getting the best deal possible for your situation.

Yes. A little-known FHA benefit is that the agency will allow a home buyer to assume the existing FHA mortgage on a home being purchased. The buyer must still qualify for the mortgage with its existing terms but, in a rising mortgage rate environment, it can be attractive to assume a home seller’s loan. Five years from now, for example, a buyer of an FHA-insured home could inherit a seller’s sub-3 percent mortgage rate. This can make it easier to sell the home in the future.

While you can’t buy a true rental property with an FHA loan, you can buy a multi-unit property — a duplex, triplex, or fourplex — live in one of the units, and rent out the others. The rent from the other units can partially, or even fully, offset your mortgage payment.

Closing costs are about the same for FHA and conventional loans with a couple of exceptions. First, the appraiser’s fee for an FHA loan tends to be about $50 higher. Also, if you choose to pay your upfront MIP in cash (instead of including this 1.75% fee in your loan amount), this one-time fee will be added to your closing costs. Additionally, the fee can be rolled into your loan amount.

Most borrowers will need a minimum credit score of 580 to get an FHA loan. However, home buyers who can put at least 10% down are eligible to qualify with a 500 score. Yet, each lender may have their own credit score minimums, separate to those established by the Federal Housing Administration.

The loan-to-value (LTV) ratio for FHA loans typically cannot exceed 96.5%, meaning you can borrow up to 96.5% of your home’s value. This high LTV ratio is part of what makes FHA loans accessible, especially for first-time homebuyers who might not have substantial savings for a down payment.

For FHA loans, the equivalent of private mortgage insurance (PMI) is the mortgage insurance premium (MIP). MIP is required for all FHA loans, regardless of the down payment or loan-to-value ratio. This insurance protects lenders from losses in case of borrower defaults and is included in both upfront and ongoing mortgage costs.

If you default on an FHA loan, the lender can initiate foreclosure proceedings. The FHA loan program, backed by the Federal Housing Administration, is designed to minimize the risk of defaults by offering more lenient qualification criteria. However, consistent failure to make mortgage payments may lead to foreclosure, impacting your credit score and homeownership status.

Today’s FHA loan rates

Now is an opportune time to consider an FHA loan, with current mortgage rates being historically competitive.

FHA loan interest rates are typically among the most competitive. To capitalize on these favorable rates, start by comparing offers from FHA-approved lenders.

Finding the most affordable loan could be just a few clicks away. Begin your journey towards homeownership today by exploring your options and discovering the best rates available for your financial situation.

Time to make a move? Let us find the right mortgage for you