Conventional loan vs FHA: What’s better?

There’s no one-size-fits-all mortgage. When deciding between a conventional loan vs FHA loan, you’ll have to compare costs and benefits based on your personal finances.

Compare home loan options. Start hereA conventional loan is often better if you have good or excellent credit because your mortgage rate and PMI costs will go down. But an FHA loan can be perfect if your credit score is in the high-500s or low-600s. For lower-credit borrowers, FHA is often the cheaper option.

These are only general guidelines, though. And the choice between a conventional loan vs FHA loan might be different for you. So be sure to look closely at both loan types and choose the best one for your financial situation.

In this article (Skip to...)

- Conventional loan vs FHA

- Down payments

- Credit scores

- Debt-to-income ratio

- Mortgage insurance

- Loan limits

- Mortgage rates

- Mortgage payments

- Additional options

- FAQ

Conventional loan vs FHA comparison

There are plenty of low-down-payment options for today’s home buyers. But many will choose either a conventional loan with 3% down or an FHA loan with 3.5% down.

Compare home loan options. Start hereSo, which type of home loan program is better? That depends on your financial situation.

Here’s an overview of what you need to know about qualifying for a conventional loan vs FHA loan.

| Conventional 97 Loan | FHA Loan | |

| Minimum Down Payment | 3% | 3.5% |

| Minimum Credit Score | 620 | 580 |

| Maximum Debt-to-Income Ratio | 43% | 50% |

| Loan Limit for 2024 (in most areas) | $ | $ |

| Income Limit | No income limit | No income limit |

| Mortgage Insurance | Annual fee | Annual and upfront fee |

Down payment requirements

Both conventional and FHA mortgage programs have minimum down payment amount requirements which borrowers must meet in order to be eligible for a home loan and reach their goal of homeownership.

Compare home loan options. Start here- FHA: 3.5% down with a 580 credit score, or 10% down a score between 500-579

- Conventional 97: 3% down

Like other conventional loans, conventional 97 applicants will pay private mortgage insurance (PMI) with less than 20% down. And all FHA borrowers are required to pay mortgage insurance regardless of down payment.

Credit scores

In deciding between an FHA loan and the Conventional 97 loan, your individual credit score matters. This is because your credit score determines the type of mortgage loan you’re eligible for. Credit history affects your monthly mortgage payments, too.

Compare home loan options. Start hereMinimum credit score requirements for FHA and conventional loans are:

- FHA: 580 credit score with 3.5% down, or 500-579 credit score with 10% down

- Conventional: 620 credit score

If your credit score is between 500 and 620, the FHA loan is best suited for you because it’s your only available option.

But if your credit score is above 620, it’s worth looking into a conventional loan with 3% down. Especially because, as your credit score goes up, your mortgage rate and PMI costs go down.

Debt-to-income ratio

Another factor you need to consider when choosing between a conventional and FHA loan is your debt-to-income ratio or DTI ratio. This is the amount of debt you owe on a monthly basis, compared to your monthly gross income.

Compare home loan options. Start here- Conventional loans usually allow a maximum DTI of 43% — meaning your debts take up no more than 43% of your gross monthly income

- FHA loans allow for a higher DTI of up to 50% in some cases

However, even with FHA loans, you’ll have to shop around if your debt-to-income ratio is above 45%. Because the FHA allows mortgage lenders to set their own in-house loan requirements, some may set stricter DTI requirements that are below 50%.

Debt-to-income ratios tend to make a bigger difference in high-cost areas, like big cities, where home values are high.

If you’re buying somewhere like Los Angeles, New York, or Seattle, your monthly debt (including mortgage costs) will take up much more of your income simply because real estate is so much more expensive.

Mortgage insurance

FHA and conventional loans both charge mortgage insurance. But the cost varies depending on which type of loan program you have, and how long you keep the mortgage.

Compare home loan options. Start here- FHA mortgage insurance (MIP): The costs for MIP is the same for most borrowers: 0.55% of the loan amount per year, with a one-time upfront fee of 1.75%

- Conventional loans private mortgage insurance (PMI): The costs for PMI vary depending on your credit score and loan-to-value ratio. You’ll only pay PMI when you put less than 20% down, and you’ll only continue to pay monthly premiums until you reach 20% home equity

| Conventional Loans | FHA Loans | |

| Mortgage Insurance Type | Private Mortgage Insurance (PMI) | Mortgage Insurance Premium (MIP) |

| Upfront Mortgage Insurance Fee | n/a | 1.75% of loan amount |

| Annual Mortgage Insurance Rate | Up to 2.25% of loan amount | 0.55% of loan amount |

| Duration | Until the loan reaches 80% LTV | 11 years (down payment of 10% or more) OR life of the loan (down payment of 3.5% to 10%) |

The cheaper mortgage insurance option for you depends on your financial situation.

Conventional 97 mortgage insurance goes away at 80% loan-to-value. You’ll also hear loan officers refer to this as 20% home equity (both terms essentially refer to the same thing).

This means that, over time, your Conventional 97 can become a better value — especially for borrowers with high credit scores.

Also, consider upfront charges.

- In addition to MIP, the FHA charges an upfront mortgage insurance premium known as UFMIP. UFMIP costs 1.75% of your loan size, is added to your loan balance, and is non-recoverable except via the FHA Streamline Refinance

- The Conventional 97 charges no equivalent upfront fee for mortgage insurance. It only charges monthly mortgage insurance premiums

Conventional loan vs FHA loan limits

Both the FHA and conventional loans have limits on the amount of money you can borrow.

Compare home loan options. Start hereIn 2024, the FHA loan limits for a single-family home is $ in most of the U.S.

The conventional loan limit for a single-family home is $.

Any loan amount that exceeds these limits are considered non-conforming loans or jumbo loans.

Conventional loan vs FHA mortgage rates

Mortgage rates typically look lower for FHA loans than conventional loans on paper. For instance, today’s average FHA rates are as low as % (% APR)*, while conventional mortgage rates are as low as % (% APR)*.

Compare conventional and FHA mortgage rates. Start hereHowever, those rates can’t be taken at face value. First, because mortgage rates vary depending on your personal finances, your rate will likely be different from the average rate.

Second, PMI and credit score can also affect your interest rate and mortgage payment. For conventional loans, a lower credit score means a higher interest rate. So if your score is in the low- to mid-600s, an FHA loan might be cheaper.

Conventional loans also base mortgage insurance rates on your credit score, which contributes to a higher monthly payment as well.

*Current rates according to The Mortgage Reports' lender network. Rates are for sample purposes only; your own rate will be different.

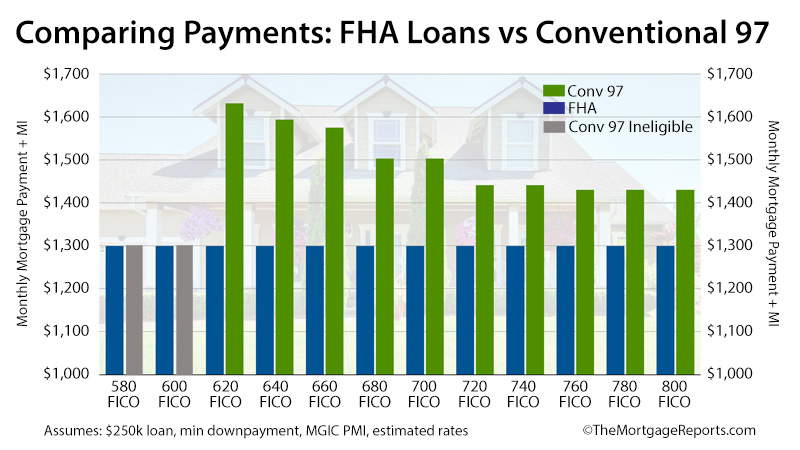

Conventional loan vs FHA mortgage payments

For home buyers with good credit scores, a conventional loan may be more attractive. That’s because conventional loan costs are more dependent on your credit score and down payment than FHA loan costs. And as a result, your monthly payments and PMI are lower when your credit score is higher. This is a key difference from how FHA loans work.

Compare conventional and FHA mortgage rates. Start here

With an FHA loan, your mortgage rate and MIP cost the same no matter what your FICO score.

That means in the short term, FHA loans may be more advantageous.

But over the long-term, borrowers with above-average credit scores will typically find Conventional 97 loans more economical relative to FHA ones.

Remember, mortgage insurance for conventional loans can be canceled at 20% loan-to-value ratio. But FHA mortgage insurance lasts the entire life of the loan. The only way to bypass this requirement is if you put down at least 10% down. This way you may be able to drop FHA mortgage insurance after 11 years (assuming 20% loan-to-value).

So if you’ll be staying in the home long enough to reach 20% equity — and especially if you have a good credit score — a conventional loan could be your cheaper option in the long run.

FHA vs Conventional infographic

Alternative low-down-payment loan programs

The conventional 97 loan and FHA loan aren’t the sole options for low-down-payment mortgages. Explore a variety of other mortgage loans with low or no upfront expenses to make homeownership more accessible:

Compare your home loan options. Start here- Fannie Mae HomeReady: This home loan offers below market interest rates, reduced private mortgage insurance costs, and it allows the income of everyone living in the household to qualify. However, there are income limits, loan maximums, and you’ll need a FICO score of 620 or more and a DTI of 50% or less

- Freddie Mac Home Possible: Similar to HomeReady, it has income and loan limits, and it requires a minimum credit score of 660, 3% down payment, and DTI below 43%. However, Freddie Mac Home Possible offers flexible loan approval requirements that help low-income families become homeowners

- VA loan: This mortgage loan requires no down payment and offers flexible credit score minimums and below-market rates. VA loans have no maximum loan amounts. Plus, bankruptcy and foreclosure are not immediate disqualifications. Yet, this program is only available to eligible service members and veterans

- USDA loan: This rural housing government-backed loan requires no down payment and has no maximum home purchase price. Although there are drawbacks. This government-agency loan does have property standards that require the home to be located in a rural area. There are also income limits for the buyer, and it does carry mortgage insurance for the entire loan term

Most of these mortgage loan products can only be used to purchase a primary residence — a home in which you live in for the majority of the year.

Vacation homes and investment properties are generally not allowed.

For many first-time homebuyers, though, the choice among low-down payment loans will be between the FHA loan and the Conventional 97. This is because VA loans are available to military borrowers only. USDA loans are restricted to suburban and rural areas, with maximum loan and income limits, and HomeReady has similar income restrictions.

Conventional loan vs FHA loan FAQ

Between FHA and conventional, the better loan for you depends on your financial circumstances. FHA might be better than conventional if you have a credit score below 680, or higher levels of debt (up to 50 percent DTI). Conventional loans become more attractive the higher your credit score is because you can get a lower interest rate and monthly payment.

You can switch from an FHA to a conventional loan by refinancing your mortgage. This means you get a new conventional loan to pay off your existing FHA loan. This might make sense to do if you have at least 20 percent equity in your home and a 620 or higher credit score. Then, you may be able to save by switching from an FHA to a conventional loan with no PMI.

If you get a conventional loan with 20 percent down or more, you won’t have to pay for mortgage insurance. That’s a big benefit over FHA loans, which require mortgage insurance regardless of your down payment size. The conventional 97 loan also lets you put just 3 percent down, while FHA requires 3.5 percent at minimum. And conventional loans offer lower mortgage rates the higher your credit score is. That’s good news if you have a good credit score of 720 or higher.

FHA loans are great for borrowers who need a home loan with a lower bar of entry. The big benefits are that they allow lower down payments (just 3.5 percent) and a lower credit score (580) than many other mortgage loans.

You have to pay for FHA mortgage insurance regardless of your down payment size. And you can’t get rid of it unless you refinance. So if you have a great credit score and/or you’re putting 20 percent or more down, an FHA loan likely isn’t the right choice for you. In that case, look into a conventional loan instead.

Conventional loans require a credit score of at least 620. But some mortgage lenders might set their own requirements, starting at 640, 660, or even higher. Plus, your conventional mortgage rate will be better the higher your credit score is. So especially if your credit is on the lower end, be sure to show around with different lenders for the best deal.

FHA loans require a credit score of 580 or higher in most cases. You might be able to get an FHA loan with a credit score of 500-580 if you make a 10 percent or bigger down payment. But you’ll have to search for the right lender because few mortgage companies allow scores in that range for FHA loans.

Conventional loan interest rates are typically a little higher than FHA mortgage rates. That’s because FHA loans are backed by the Federal Housing Administration, which makes them less “risky” for lenders and allows for lower rates. However, if you have a great credit score (above 680, in most cases) you might qualify for a lower conventional rate. But, you also have to consider the annual mortgage insurance rate with each loan. Depending on your credit score and down payment, conventional mortgage insurance rates could be higher or lower than FHA insurance rates. This will affect which loan is cheaper overall.

You might qualify for a conventional loan if you have a credit score of at least 620; a debt-to-income ratio of 43 percent or lower; a 3 percent down payment; and a steady, two-year employment history proven by tax returns and bank statements. To qualify for the low-down-payment conventional 97 loan, you must buy a single-family property (no 2-,3-, or 4-units allowed).

Generally, conventional loans have a higher credit score requirement than FHA loans. Conventional loans may require a credit score of 620 or higher, while FHA loans may allow for a credit score as low as 500 to 580, depending on the lender.

Mortgage insurance is a type of insurance that protects lenders in case the borrower defaults on the loan. With a conventional loan, private mortgage insurance (PMI) is generally required if the down payment is less than 20%. With an FHA loan, mortgage insurance premiums (MIP) are required for the life of the loan.

FHA loans generally have more flexible underwriting requirements compared to conventional loans. They may allow for higher debt-to-income ratios, lower credit scores, and non-traditional credit histories. Conventional loans may have stricter underwriting requirements.

Yes, you can refinance from an FHA loan to a conventional loan. Refinancing may help you get a lower interest rate, lower monthly payments, or eliminate mortgage insurance. However, it’s important to evaluate the potential costs, benefits, and qualification requirements before proceeding with the refinance.

Conventional loan vs FHA: The bottom line

For today’s low down payment home buyers, there are scenarios in which the FHA loan is what’s best for financing; and there are scenarios in which the Conventional 97 is the clear winner. Mortgage rates for both home loans should be reviewed and evaluated.

Ready to make a home purchase? Talk with a loan officer about your mortgage options. You should compare personalized quotes for both FHA and conventional loans to see which one is cheaper for your situation and suits your needs best.

Time to make a move? Let us find the right mortgage for you