Today's mortgage rates

Average mortgage rates rose moderately yesterday. Indeed, they didn't fall at all this week. Still, the previous week had been good, and those rates yesterday evening were very close to where they stood at the start of March. Up and down but going nowhere.

Oh, dear. Next week is yet another during which mortgage rates could move in either direction. Unfortunately, there's currently no clear momentum in markets nor any predictable economic events to help me make predictions. And Federal Reserve events next Wednesday, on which much could turn, are wholly unpredictable.

Find and lock a low rateCurrent mortgage and refinance rates

| Program | Mortgage Rate | APR* | Change |

|---|---|---|---|

| Conventional 30-year fixed | |||

| Conventional 30-year fixed | 6.848% | 6.914% | -0.04 |

| Conventional 20-year fixed | |||

| Conventional 20-year fixed | 6.589% | 6.663% | -0.02 |

| Conventional 15-year fixed | |||

| Conventional 15-year fixed | 6.055% | 6.153% | -0.05 |

| Conventional 10-year fixed | |||

| Conventional 10-year fixed | 6.001% | 6.062% | Unchanged |

| 30-year fixed FHA | |||

| 30-year fixed FHA | 6.617% | 6.672% | -0.24 |

| 30-year fixed VA | |||

| 30-year fixed VA | 6.583% | 6.621% | -0.3 |

| 5/1 ARM Conventional | |||

| 5/1 ARM Conventional | 6.078% | 6.471% | -0.05 |

| Rates are provided by our partner network, and may not reflect the market. Your rate might be different. Click here for a personalized rate quote. See our rate assumptions See our rate assumptions here. | |||

Should you lock a mortgage rate today?

Economic data have not been kind to mortgage rates recently. And I doubt we'll see a sustained downward trend in those rates before May or June — and possibly later.

So, my personal rate lock recommendations remain:

- LOCK if closing in 7 days

- LOCK if closing in 15 days

- LOCK if closing in 30 days

- LOCK if closing in 45 days

- LOCK if closing in 60 days

However, with so much uncertainty at the moment, your instincts could easily turn out to be as good as mine — or better. So let your gut and your own tolerance for risk help guide you.

What's moving current mortgage rates

Next week's Fed event

The Federal Reserve's rate-setting body (the Federal Open Market Committee or FOMC) begins a two-day meeting next Tuesday. And it will announce on Wednesday whether it will cut general interest rates that day. (Spoiler alert: It won't.)

At least, CME's FedWatch tool, suggests that the smart money says it will hold those rates steady next week by 98% to 2%. So, if the rate announcement is almost bound to be a yawnfest, why will markets around the world be focused on the Fed that afternoon?

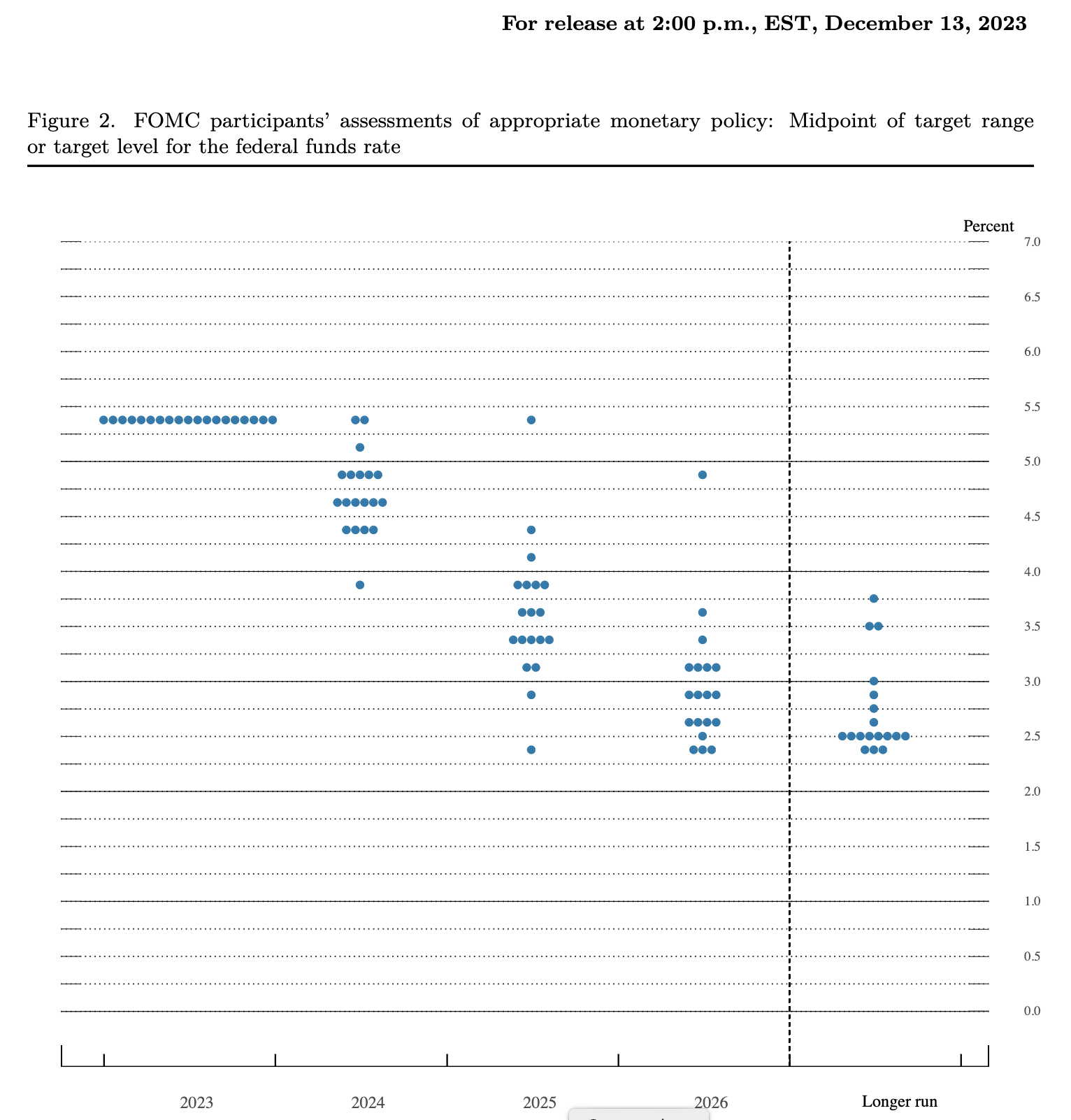

That's because the Fed will be sharing a huge amount of information about how its thinking about future rate cuts is evolving. Not only will it publish its usual report at 2 p.m. Eastern, but it will also release a quarterly Summary of Economic Projections, which crucially includes a "dot plot."

Markets and the Fed

A dot plot is a graphic representation of where individual FOMC members expect interest rates to travel over the next three years. Here's the last one, from December 2023:

[caption id="attachment_111743" align="aligncenter" width="1532"] Downloaded from the Federal Reserve website[/caption]

Markets will be fixated on two things, including changes in the dot plot. If more FOMC members are optimistic about the speed at which general interest rates might fall in the future, that's likely to be good for mortgage rates.

The other thing markets will be watching out for is most likely to be revealed at a news conference scheduled for 2:30 p.m. Eastern. And it's the likelihood of the Fed making three rate cuts in 2024. Fed Chair Jerome Powell hosts these events and the entire financial world will hang on his every word.

Three cuts were the plan at the last FOMC meeting. But the economy (and especially the inflation rate) has changed since then. And some fear there may be only two cuts this year, with the first in the third quarter. And that would almost certainly be bad for mortgage rates.

Other events next week

You'll find a list of the scheduled publications of the main economic reports below. However, none of them is likely to be remotely as consequential for mortgage rates as Wednesday's Fed events.

Indeed, most of them seldom affect those rates at all. But the two that are most likely to are a pair of March purchasing managers' indexes (PMIs) from S&P due on Thursday.

There's one for the services sector and one for the manufacturing one. And markets are expecting both these to edge downward. But we'd like to see even lower numbers than markets are expecting for mortgage rates to fall. Higher figures could push those rates higher.

As always, I'll brief you on each potentially influential report on the morning before it's published.

Economic reports next week

See above for details about the more important economic reports next week.

In the following list of next week's reports, only those in bold typically have the potential to affect mortgage rates appreciably. The others probably won't have much impact unless they contain shockingly good or bad data.

- Monday — February home builder confidence index

- Tuesday — February housing starts and building permits

- Wednesday — FOMC publications and news conference

- Thursday — March PMIs from S&P for the services and manufacturing sectors. And initial jobless claims for the week ending Mar. 16

- Friday — Nothing

Wednesday could be huge for mortgage rates.

Time to make a move? Let us find the right mortgage for you

Mortgage rates forecast for next week

Everything next week pivots on the Fed's announcements, reports and news conference. And I have no idea what those will contain. So, yet again, I must chicken out of predicting how mortgage rates will move next week.

How your mortgage interest rate is determined

A bond market generally determines mortgage and refinance rates. It's the one where trading in mortgage-backed securities takes place.

And that's highly dependent on the economy. So mortgage rates tend to be high when things are going well and low when the economy's in trouble. But inflation rates can undermine those tendencies.

Your part

But you play a big part in determining your own mortgage rate in five ways. And you can affect it significantly by:

- Shopping around for your best mortgage rate — They vary widely from lender to lender

- Boosting your credit score — Even a small bump can make a big difference to your rate and payments

- Saving the biggest down payment you can — Lenders like you to have real skin in this game

- Keeping your other borrowing modest — The lower your other monthly commitments, the bigger the mortgage you can afford

- Choosing your mortgage carefully — Are you better off with a conventional, conforming, FHA, VA, USDA, jumbo or another loan?

Time spent getting these ducks in a row can see you winning lower rates.

Remember, they're not just a mortgage rate

Be sure to count all your forthcoming homeownership costs when you're working out how big a mortgage you can afford. So, focus on something called you “PITI.” That stands for:

- Principal — Pays down the amount you borrowed

- Interest — The price of borrowing

- Taxes — Specifically property taxes

- Insurance — Specifically homeowners insurance

Our mortgage calculator can help with these.

Depending on your type of mortgage and the size of your down payment, you may have to pay mortgage insurance, too. And that can easily run into three figures every month.

But there are other potential costs. So, you'll have to pay homeowners association dues if you choose to live somewhere with an HOA. And, wherever you live, you should expect repairs and maintenance costs. There's no landlord to call when things go wrong!

Finally, you'll find it hard to forget closing costs. You can see those reflected in the annual percentage rate (APR) that lenders will quote you. Because that effectively spreads them out over your loan's term, making that rate higher than your straight mortgage rate.

But you may be able to get help with those closing costs and your down payment, especially if you're a first-time buyer. Read:

Down payment assistance programs in every state for 2023

Mortgage rate methodology

The Mortgage Reports receives rates based on selected criteria from multiple lending partners each day. We arrive at an average rate and APR for each loan type to display in our chart. Because we average an array of rates, it gives you a better idea of what you might find in the marketplace. Furthermore, we average rates for the same loan types. For example, FHA fixed with FHA fixed. The result is a good snapshot of daily rates and how they change over time.