10-year mortgage rates can save you thousands

10-year mortgage rates are generally lower than 30-year, 20-year, or even 15-year mortgage rates.

And with a much shorter loan term, a 10-year mortgage can save you tens of thousands in interest over the course of your loan.

The catch? 10-year mortgage payments are a lot higher than other types. And these loans can be harder to find.

But for those who afford the payments, a 10-year mortgage is a great tool to pay off your house faster and save on interest.

Verify your mortgage eligibilityIn this article (Skip to...)

- How low are 10-year mortgage rates?

- What is a 10-year fixed mortgage?

- Should I use a 10-year mortgage loan?

- A 10-year refinance lets you pay off your loan early

- 10-year fixed mortgage rates vs. 10-year adjustable rates (ARMs)

- 10-year mortgage rates: What to consider

- Where can I find a 10-year fixed-rate loan?

- Alternatives to a 10-year fixed-rate mortgage

How low are 10-year mortgage rates?

10-year fixed mortgage rates tend to be significantly lower than 30-year fixed rates (which is the most popular loan type).

A survey of multiple lenders1 at the time of writing showed 10-year rates ranging from 0.3% to 0.7% lower than 30-year rates. On average, 10-year mortgage rates were about 0.50% lower than 30-year mortgage rates.

For example, say 30-year rates are averaging around 3.25%. Average interest rates for a 10-year loan might be 2.75%. But they’d likely range from 2.5% to 3.0% — and could vary more depending on the borrower.

On average, 10-year mortgage rates were about 0.50% lower than 30-year mortgage rates.

Of course, interest rates vary a lot from one borrower to the next.

Your own rate could be higher or lower depending on your credit score, loan amount, down payment, and more.

That’s why it’s always important to shop for the lowest rate. With a 10-year mortgage, shopping around is doubly important because not all mortgage lenders offer these loans.

You’ll have to search out a few that do in order to compare interest rates and find the best 10-year mortgage rate for you.

Compare mortgage lenders. Start here

What is a 10-year fixed mortgage?

A 10-year mortgage is simply a home loan with a 10-year term. A ‘term’ is the amount of time it takes to pay down your loan in full.

Most people choose a fixed-rate mortgage with a 30-year term.

But a shorter term, like a 10-year loan, costs way less in interest for two reasons:

- You’re paying interest for much less time. If you’re paying x% for 30 years, it costs a lot more than paying x% for 10 years

- 10-year mortgage rates are generally lower than 30- or 15-year mortgage rates. Typically, the shorter your loan term is, the lower your interest rate is

A 10-year mortgage probably sounds great so far. But there’s one big drawback.

Higher monthly mortgage payments

The biggest drawback to a 10-year mortgage — and the thing that keeps most people from getting one — is that it has much higher mortgage payments than a longer-term loan.

If you borrow a big sum over 30 years, you get 360 monthly payments over which to pay off the loan.

If you borrow the same sum over 10 years, you get only 120 months to pay down the same balance.

Take a look at one example of how 10-year mortgage payments might compare to a 30-year loan:

| 10-Year Fixed-Rate Mortgage | 30-Year Fixed-Rate Mortgage | |

| Loan Amount | $300,000 | $300,000 |

| Interest Rate* | 2.5% | 3.0% |

| Monthly Payment | $2,800 | $1,300 |

| Total Interest Paid | $39,400 | $155,300 |

*Interest rates shown are for sample purposes only. Your own rate will be different

Payments for a 10-year mortgage are not three times as much as a 30-year mortgage.

But they’re significantly more — enough to put this loan type outside most people’s monthly budgets.

If you can afford 10-year mortgage payments, though, you’ll save tens of thousands in interest.

Just look at the savings in the example above. For the same loan amount, a 10-year mortgage saves you over $115,000 compared to a 30-year loan.

For those who can swing it, buying or refinancing real estate with a 10-year loan means huge savings in mortgage interest over the years.

Verify your home loan eligibility

Should I use a 10-year mortgage loan?

For most people, the additional monthly cost of spreading mortgage payments over 120 months instead of 360 is just too high.

But if you have plenty of spare money at the end of each month, 10-year mortgage rates are well worth exploring.

Who benefits most from a 10-year fixed mortgage?

There are a few scenarios in which a 10-year loan term makes particular sense

- You’re buying a different home 10 or so years before you retire and want to have it paid off when you do

- You have a new job or raise that lets you afford the higher monthly payments

- You’re refinancing 5-15 years into paying down your mortgage and you don’t want to restart the clock with a new 30-year loan

- You want to pay off your mortgage loan ASAP, and can afford the higher payments by prioritizing your mortgage over other potential expenses (like a new car, a remodel, or a bigger house)

If you’re a younger, first-time home buyer, a 10-year mortgage might not be the best choice.

A longer loan term will free up your monthly budget for other homeownership costs that usually pop up (like furnishing and repairs).

And you still have the option to refinance to a shorter loan term later on, maybe when you’re making more money or have lower monthly debts (e.g. when things like student loans or a car loan are paid off).

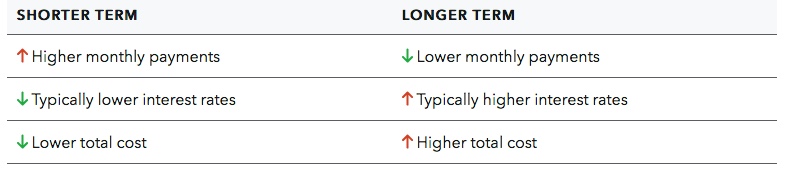

Pros and cons of a 10-year fixed mortgage

Federal regulator the Consumer Financial Protection Bureau has a graphic that neatly sums up the pros and cons of 10-year mortgage rates:

Image: CFPB

If you think a 10-year mortgage term is right for you, be sure your income and monthly budget are reasonably secure.

If your circumstances change, you may have to refinance to a longer term to make your monthly payments affordable again.

This involves paying a second round of closing costs and going through the whole mortgage process again.

How a 10-year refinance could help you pay off your loan faster

Many people refinance their existing 30-year mortgage to a new 30-year loan without a second thought.

But many homeowners should consider refinancing to a shorter term.

Suppose you’ve already been paying your home loan for 10, 15, or 20 years. Resetting the clock on your mortgage means you’ll be repaying your loan for 30 more years.

Remember, your interest payments reset with the new term, too.

If your new mortgage rate isn’t substantially lower than the original one, you could end up paying more in interest overall even though your monthly payments are lower.

Many lenders offer 10-, 15- or 20-year refinance loans that could help you secure a lower rate and pay off your mortgage when you originally planned.

10-year refinance rates are low, just like 10-year home purchase rates. And they let you pay off the loan sooner than you would have otherwise.

Especially if you’re older — and retirement is a much closer prospect than it used to be — paying off your mortgage as soon as you can might make your golden years much more comfortable.

10-year adjustable-rate loans vs. 10-year fixed-rate loans

When you’re looking at 10-year mortgage rates, note the difference between a 10-year fixed-rate mortgage (FRM) and a 10/1 adjustable-rate mortgage (ARM).

You may see 10/1 ARM rates advertised. But don’t be confused. These are almost always 30-year mortgages.

The ‘10/1’ means that the initial ARM interest rate is fixed for the first 10 years of the loan. After that, it may rise or fall each year depending on which way the broader interest market is trending.

A 10-year FRM, on the other hand, has a fixed mortgage rate that stays the same throughout the life of the loan — until you pay off the loan, sell the home, or refinance. This means payments are fixed and reliable, too.

10/1 ARM rates vs. 10-year fixed mortgage rates

Traditionally, adjustable-rate mortgages have lower interest rates than comparable fixed-rate mortgages.

Lower rates reflect lower risk on the lender’s part. Since you agree to a potentially higher rate after the initial fixed period, ARMs are inherently less risky for lenders.

But some of that reward has been eroded over the last decade or so, as interest rates have generally only moved downward. Rates that are likely to be lower rather than higher de-incentivize lenders from offering far lower rates on ARMs.

Compared with FRMs generally, you can still find lower rates on some types of ARMs, especially those with shorter fixed-rate periods.

But, by the time you get up to 10/1 ARMs, you’re likely to find little advantage — and sometimes even a disadvantage.

You’re almost certain to get a significantly lower rate on a 10-year FRM than on a 10/1 ARM.

Verify your new rate

10-year mortgage rates: What to consider

Just like any other mortgage, choosing a 10-year home loan isn’t just about the interest rate.

You still have to look at your loan options carefully and consider:

- APR — The annual percentage rate (APR) is an estimate of the total cost of the loan each year, including interest and fees

- Mortgage insurance — A 10-year conventional loan with less than 20% down will require private mortgage insurance (PMI)

- Discount points — Some low-rate offers assume you’ll pay for ‘discount points’ at closing to lower your rate. One discount point typically costs 1% of the loan amount

- Origination fees — These are the fees a lender charges to set up your mortgage. They vary a lot from one lender to the next and are an important metric for comparing mortgage offers

- Home equity — If you want to refinance into a 10-year mortgage loan, you likely want to have at least 20% equity in your home. Otherwise, you’ll have to pay mortgage insurance and your monthly costs will be higher

- Loan program — A 10-year mortgage will likely be a conventional or ‘conforming’ loan. The popular FHA loan program does not offer a 10-year term

Where can I find a 10-year fixed-rate mortgage?

Most lenders don’t offer 10-year fixed mortgages. A whole lot of them only give you a choice between 15-year and 30-year loans.

But that doesn’t mean these are hard to find.

To give just a few examples, the following major lenders offer 10-year mortgages:

- Quicken Loans offers a ‘YOURgage’ product that lets you choose any term between eight years and 29 years (including a 10-year mortgage)

- New American Funding has mortgage terms ranging from 10-30 years

- US Bank offers 10-year fixed mortgages if you prefer a large mainstream bank

- Crestline Funding has a ‘MyFi’ product that offers terms from five to 40 years. However, it’s licensed to lend in only 11 states: Alaska, Arizona, California, Colorado, Florida, Idaho, Montana, Oregon, Utah, Washington, and Wyoming

This is just a shortlist. There are plenty of other lenders offering 10-year mortgages — you just might have to do a little extra research to find them.

If you don’t want to tackle the job on your own, consider enlisting the help of a mortgage broker who can find 10-year loans and compare lenders on your behalf.

Alternatives to a 10-year fixed-rate loan

Let’s say you’re sold on the idea of being mortgage-free within 10 years.

New home buyers have little choice but to go for a 10-year term on a new mortgage.

Or, if you’re already a homeowner, you have the option to refinance your current mortgage to a new 10-year loan with a lower rate.

But there are other ways to pay off your mortgage quickly that don’t involve the hassle and costs of a new mortgage or refinance.

Pay extra on your mortgage to pay it off early

This is easy. All you do is pay extra on your mortgage — above the required payment — each month.

To make this strategy worthwhile, you’ll need to pay substantially more — as much as you can afford each month, probably.

This strategy is less risky than committing to the 10-year mortgage.

The extra payments are optional. If circumstances change, you simply stop paying extra. With a 10-year loan, you’re obligated to make the full payment, or suffer damaged credit and the potential loss of your home.

Plus, paying extra is easy. Most lenders understand that any extra funds received should be applied to principal. But it’s worth checking how they will apply extra funds just in case.

While you’re chatting with your lender, make sure your mortgage doesn’t have prepayment penalties.

These are “fines” for paying down your mortgage early. True, most lenders no longer charge them. But it’s worth making sure your lender won’t ding you before you start making extra payments.

Make one extra mortgage payment per year

Making one extra payment per year won’t zero out your loan balance as fast as an extra payment each month. But it certainly helps.

Instead of making one payment each month (12 per year) make 13 payments.

Or you could switch to bi-weekly payments (one every two weeks) which adds up to one extra monthly payment per year.

The arithmetic might seem odd, but it works out. You usually make 12 full payments, which is 24 half ones. But if you pay every two weeks, you make 26 half-payments a year — or 13 full payments.

Recast your mortgage

A mortgage recast lets you pay a one-time, lump-sum to reduce your mortgage balance and shorten your loan term.

Your lump sum is used to reduce your principal. Then the lender recalculates your whole remaining mortgage, changing the term and adjusting your amortization table accordingly.

This is one way to shorten your loan term without refinancing (and without paying closing costs again).

Not every lender allows you to recast your mortgage. And even those that do often charge a fee for it: perhaps a few hundred dollars.

Still, that’s a lot cheaper than typical refinancing.

If your lender won’t recast your loan, you can almost always still pay down the principal using a lump sum. Though this method is a bit messier because all the math hasn’t been adjusted to formalize the change.

Whichever of these routes you choose, talk everything through with your lender before you make additional payments.

And put your instructions for the extra payments in writing so there’s no room for misunderstanding.

Save money with or without 10-year mortgage rates

There are plenty of ways to turn your dream of being mortgage-free in 10 years into a reality.

If you can afford the higher payments of a 10-year fixed loan, you can shorten your loan term, lower your interest rate, and greatly reduce your total interest payments.

But even without a 10-year mortgage or refinance, it’s possible to save on your home loan.

15- and 20-year mortgages offer similar low rates but slightly lower monthly payments.

Or, you can use one of the above strategies to pay extra on your mortgage and pay it off early.

The only question is, what will you choose to do?

Time to make a move? Let us find the right mortgage for you110-year and 30-year fixed mortgage rates sourced on 10/23/2020 from US Bank, Realtor.com, Bankrate, Zillow, and mortgagecalculator.com. Advertised rates based on a borrower with excellent credit and a sizeable down payment. Your own rate will vary.

![30-Year Mortgage Rates Chart [image]](/_next/image?url=https%3A%2F%2Fassets.themortgagereports.com%2Fwp-content%2Fuploads%2F2020%2F02%2F30-Year-Mortgage-Rates-Chart-image.jpg&w=3840&q=75)