The zero-down payment mortgage

Anyone looking to step onto the property ladder with a hefty upfront payment needs to understand how first-time home buyer loans with zero down payment work.

These loans eliminate the need for a traditional down payment, leaving just the standard closing costs to consider. Yet, other alternatives, such as the FHA loan and Conventional 97, allow as little as 3% down.

Additionally, government grants and loans are available to offset these initial costs. That makes it possible to buy a home with no money down, or very little money down.

Click to see your ZERO down eligibilityIn this article (Skip to…)

- Buying with zero down

- No-down-payment loans

- Low-down-payment loans

- Zero-down mortgage lenders

- How to get a down payment

- Zero-down loans FAQ

Can I buy a house with no money down?

Yes, you can buy a house with no money down, especially as a first-time home buyer. There are specific first-time home buyer loans with zero down and various assistance programs made to make homeownership more attainable and budget-friendly.

Typically, conventional and FHA loans require a minimum 3% to 3.5% down payment. However, there are exceptional options available for certain groups, like veterans and rural home buyers with moderate to low incomes, that allow for zero down payments. These first-time home buyer programs open the door to owning a home without the need for a substantial upfront payment.

Discover your zero-down loan options. Start hereMoreover, every state offers forms of home buyer assistance. These programs, often in the form of government grants, might cover your entire down payment, sparing you from significant out-of-pocket expenses. This makes the dream of homeownership much more accessible, even if you aren’t eligible for a zero-down loan.

What is a zero-down mortgage?

Zero-down mortgages are a viable option for many first-time home buyers, providing a path to homeownership without the burden of a large upfront down payment. These loans are usually government-backed, such as VA or USDA loans, reducing the risk to lenders and making it possible for buyers with less financial flexibility to purchase a home.

For example, VA loans cater to military veterans and offer benefits like no down payment and no mortgage insurance. USDA loans, on the other hand, are designed to promote homeownership in rural and certain suburban areas, also with no down payment required. Both of these first-time home buyer loans with zero down make homeownership more accessible, especially for those who might struggle to save for a conventional down payment.

How to buy a house with no money down

Buying your dream home without an upfront down payment is possible, thanks to first-time home buyer loans with zero down. Follow this process for making a zero-down home purchase.

Check your zero-down eligibility. Start here

Step 1: Apply for a zero-down VA loan or USDA loan

The easiest way to buy a house with no money down is to use a government-backed mortgage. VA loans are designed for veterans and active military members, and they offer the advantage of no down payment and no requirement for mortgage insurance. This makes them an attractive option for eligible first-time buyers.

Similar to this, USDA loans are intended for borrowers in rural and some suburban areas and also offer the benefit of no down payment.

To qualify for these government-backed loans, applicants must meet specific service- or location-based criteria.

Step 2: Use a first-time home buyer program to cover the down payment

For those who find saving for a down payment challenging, various first-time home programs are available at both the state and federal levels. These programs offer grants or low-interest loans to cover down payments and closing costs.

By reducing the initial financial barrier, these homeownership programs make buying a home more attainable for individuals and families with limited funds.

Step 3: Ask for a down payment gift from a family member

Receiving a down payment gift from a family member can significantly ease the financial burden of buying a home. For your lender to accept this down payment source, a gift letter is required from the donor stating that the money is a gift and not a loan.

This letter should include details such as the relationship between the donor and recipient, the amount of the gift, and the address of the property being purchased.

Step 4: Get the lender to pay your closing costs (lender credits)

One way to reduce upfront expenses is to negotiate for lender credits, where the lender agrees to cover your closing costs in exchange for a slightly higher interest rate on your mortgage.

This trade-off can be beneficial for buyers who prefer to minimize initial expenses, although it’s important to consider the long-term cost implications of a higher interest rate on the overall loan.

Step 5: Get the seller to pay your closing costs (seller concessions)

Another strategy to manage upfront costs is through seller concessions, where the seller agrees to pay a portion or all of the buyer’s closing costs.

This negotiation is part of the home buying process and can include various fees such as loan processing, appraisal, and title insurance. Seller concessions can significantly lower the immediate financial burden for the buyer, making the process of purchasing a home more accessible.

First-time home buyer loans with zero down payment

The USDA loan program and the VA loan program allow eligible buyers to buy a house with no money. Both are available to first-time home buyers and repeat buyers alike. But they have special requirements to qualify.

Check your zero-down eligibility. Start hereUSDA loans (0% down)

When exploring first-time home buyer loans with zero down, the USDA loan stands out as an exceptional option. Offered by the U.S. Department of Agriculture, this program is commonly known as the “Rural Housing Loan” or the “USDA loan,” and it provides 100% financing.

A notable aspect of the USDA loan is its broad definition of “rural,” which surprisingly includes many suburban neighborhoods in addition to traditional rural areas.

The primary aim of the USDA is to assist “low-to-moderate-income home buyers” in the vast majority of the U.S., with the exception of major cities. Remarkably, about 97% of the U.S. land area falls under the USDA’s eligibility criteria. This makes the USDA loan not just a rural home buying option but a widespread opportunity for first-time home buyers looking to purchase in non-metro locations.

Key requirements of a USDA loan include:

- Zero down payment.

- A minimum credit score of 640.

- Debt-to-income ratio below 41%.

- Stable two-year employment history.

- Income not exceeding 115% of the area’s median income.

- Purchasing a single-family primary residence in an eligible area.

Besides requiring no down payment, another significant advantage of the USDA loan is that it often has lower mortgage rates compared to similar low- or no-down-payment options.

With its combination of zero down payment, broader location eligibility, and potentially lower mortgage rates, the USDA loan is a valuable tool for many first-time homebuyers seeking an accessible and cost-effective way to enter the housing market.

VA loans (0% down)

The VA loan is a zero-down mortgage available to members of the U.S. military, veterans, and surviving spouses.

The U.S. Department of Veterans Affairs guarantees VA loans and helps lenders offer favorable rates and more lenient qualification criteria to borrowers who meet VA mortgage guidelines.

Check your VA loan eligibility. Start hereMost veterans, active-duty service members, and honorably discharged service personnel are eligible for the VA program. Home buyers who have spent at least six years in the Reserves or National Guard are also eligible, as are spouses of service members killed in the line of duty.

VA loan requirements:

- Certificate of Eligibility from the VA

- 0% down payment

- Credit score of 580-620

- Debt-to-income ratio below 41%

- Two-year employment history

- Buy a 1- to 4-unit primary residence

VA loans have no maximum loan amount. It’s often possible to get a VA loan above the current conforming loan limits, as long as you have enough credit and can afford the payments.

In addition, VA loans charge no ongoing private mortgage insurance (PMI). There’s only a one-time funding fee that can be rolled into your loan. That’s a serious benefit. It could lower your monthly payments by a few hundred dollars in some cases.

Finally, VA mortgage rates tend to be the lowest of any home loan program. This is usually the cheapest mortgage option for eligible veterans and service members.

“Doctor loans” for physicians

Doctor loans, sometimes referred to as physician loans, are specialized home buyer programs designed to meet the unique needs of medical professionals.

Recognizing the financial burdens of medical school debt and the eventual high earning potential of doctors, these loans offer more flexible terms and requirements.

Doctor loans aim to ease the transition from training to practice, making homeownership more accessible even while you’re still in the early stages of your career.

Doctor loan requirements:

- Must be a medical resident, practicing physician, or fellow

- Credit score is usually 700 or higher, but it is more lenient than conventional loans

- High educational debt is okay if you enroll in a repayment plan

- Employment contracts are often required, especially for new or resident doctors

- A small down payment is generally around 5%, though some offer zero down

- Loans are mainly for primary residences, but some programs allow second homes or investments.

Nurses and other healthcare professionals also have options when it comes to securing a home loan. While they may not qualify for special no-down-payment mortgage loans, they can take advantage of programs offering low down payments.

Additionally, some lenders and nonprofits provide grant money and deferred loans aimed at covering the costs of both the down payment and closing fees.

Nurse home loans offer tailored solutions to make the dream of homeownership more attainable for those in the healthcare field.

First-time home buyer loans with a low down payment

While there are options for first-time home buyer loans with zero down, not everyone will qualify for one. But it may still be possible to buy a house without paying money down if you choose a low-down-payment mortgage and use a government grant or loan to cover your upfront costs.

If you want to go this route, here are a few of the best low-money-down mortgages to consider.

Conventional 97 loans (3% down)

A conventional loan is what many home buyers consider the “standard” mortgage. These loans are not government-backed, unlike FHA, VA, or USDA loans. However, they offer flexible guidelines that make it easier for first-time home buyers to qualify.

Contrary to popular belief, you don’t necessarily need a 20% down payment for a conventional loan. In fact, one of the most accessible programs for first-time home buyers is the Conventional 97 loan program, which requires as little as 3% down.

Check your 3% down eligibility. Start hereThe Conventional 97 loan program is particularly friendly to first-time home buyers. While requirements may vary slightly from lender to lender, these loans generally follow the guidelines set by Fannie Mae and Freddie Mac.

Conventional 97 loan requirements:

- 3% down payment

- Minimum 620 credit score

- Debt-to-income ratio below 43% (in most cases)

- Two-year employment history

- Loan amount within conforming loan limits

- Purchase a 1- to 4-unit property

If you have a low down payment but a solid FICO score, a Conventional 97 loan can often be the best choice.

Strong credit can net you a lower interest rate, and unlike some other programs, you can usually cancel private mortgage insurance (PMI) after a few years. This could potentially save you hundreds of dollars on your monthly mortgage payment.

Fannie Mae HomeReady loans (3% down)

Fannie Mae’s HomeReady program is designed to help home buyers with moderate incomes. This loan program stands out for its flexibility and its commitment to helping more Americans get their foot in the door of homeownership.

One distinguishing feature of the HomeReady program is its consideration for extended household income. This means you can pool resources with family members or even renters to meet income qualifications, expanding your home buying potential.

HomeReady requirements:

- Just 3% down is required

- A minimum credit score of 620 is necessary for qualification

- The program allows for a higher debt-to-income ratio compared to conventional loans

- Borrower’s income should generally be at or below the area median income, although this may vary depending on location

- Completion of an approved home buyer education course is often required

Freddie Mac Home Possible loans (3% down)

Much like Fannie Mae’s HomeReady, the Home Possible loan program from Freddie Mac aims to facilitate homeownership for those who might find it a little more challenging to qualify for a conventional loan. The program is particularly useful for first-time home buyers.

Home Possible offers multiple benefits, including reduced mortgage insurance costs and greater flexibility in the source of your down payment. The program will accept not just personal savings but also employer assistance programs and even gift funds, providing broader opportunities for qualifying applicants.

Home Possible requirements:

- A minimal 3% down payment is needed

- The program typically requires a minimum credit score of 620

- Flexible debt-to-income ratio guidelines, making it easier for borrowers with higher debt levels to qualify

- Borrowers must meet specific income requirements, which are usually based on the area’s median income

- The loan can be used for 1- to 4-unit properties, including condos and planned unit developments

FHA loans (3.5% down)

The Federal Housing Administration guarantees its FHA loan, which is a popular first-time home buyer program that is well known for offering flexibility with lower credit scores and down payments.

With an FHA loan, you can put just 3.5% down as long as your credit score is 580 or higher. By contrast, a conventional mortgage requires only 3% down, but you need a FICO score of at least 620 to qualify.

Check your FHA loan eligibility. Start hereSome buyers who qualify for conventional financing can get a more favorable rate with an FHA loan because FHA doesn’t adjust rates for buyers with lower credit scores.

According to the FHA’s guidelines, you could even get a mortgage with a credit score of 500 to 579, as long as you can put at least 10% down. But in practice, it’s harder to find lenders who will allow FICO scores below 580.

FHA loan requirements:

- 3.5% down payment

- Minimum 580 credit score

- Debt-to-income ratio below 45% (in most cases)

- Two-year employment history

- Buy a 1- to 4-unit primary residence

- Loan amount within local FHA loan limits

The major downside to an FHA loan is that you have to pay upfront and monthly mortgage insurance premiums (MIP). FHA mortgage insurance payments are required until you sell the home or refinance it into a conventional loan.

But if an FHA loan will put you in a home when other forms of financing won’t, the MIP cost is often worth it. This is due to the fact that as you build home equity over time, your investment’s rising value can offset the initial cost of MIP on an FHA loan.

Good Neighbor Next Door loan program

The U.S. Department of Housing and Urban Development (HUD) offers a unique first-time home buyer program called the Good Neighbor Next Door. It’s specifically designed to benefit first-time home buyers who are also public servants, such as teachers, firefighters, law enforcement officers, and emergency medical technicians. The program enables qualified applicants to purchase homes in designated “revitalization areas” at a significant discount—often as much as 50% off the list price.

What makes this program a standout option for first-time home buyers is the substantially reduced home price, which in turn lowers the amount needed for a down payment. In some cases, the down payment could be as low as $100, making it one of the most affordable paths to homeownership.

Another plus is that buyers can finance the home using various types of loans, such as FHA, VA, or conventional mortgages. This means you’re not locked into a specific type of loan, giving you the flexibility to choose what works best for your financial situation.

However, it’s important to note that this program comes with commitments. You must agree to live on the property as your primary residence for at least 36 months, and, depending on your profession, you may also be required to work within the area where the home is located.

Piggyback loans

Piggyback loans are a financial strategy for first-time home buyers looking to purchase a home with a low down payment.

Essentially, a piggyback loan involves taking out two separate mortgages simultaneously: One for the majority of the home’s price and a second “piggyback” loan to cover the portion that would typically be your down payment.

The most common structure is the 80-10-10, where the first mortgage covers 80% of the home’s cost, the piggyback loan covers 10%, and the remaining 10% is your down payment.

While piggyback loans have their advantages, they also come with their own set of complexities. Managing two different loans means two sets of terms and two interest rates. It’s essential to have a firm understanding of both loans and ensure that the sum of both payments fits within your budget.

Pros and cons of first-time home buyer loans with zero down

Stepping into the world of homeownership as a first-time home buyer can be both exhilarating and nerve-wracking. One of the biggest dilemmas you may face is whether or not to make a down payment.

With options like first-time home buyer loans with zero down, you don’t have to wait years to save up.

Here’s what you should know about the advantages and pitfalls of opting for a first-time home buyer program with no down payment.

Pros:

- Become a homeowner faster: Say goodbye to the long waiting game of saving for a down payment. You can dive right into the housing market and begin building equity, something that might take years otherwise.

- Financial flexibility: Keeping a down payment in your bank account gives you the leeway to allocate funds for other immediate needs, like furniture, home improvements, or emergency expenses.

- Nonprofit help: Some nonprofit organizations offer grants to first-time home buyers, which can be a significant boon if you’re aiming for zero-down payment.

- Tax incentives: Larger loan amounts can offer more significant mortgage interest deductions if you itemize your taxes, leading to potential tax savings.

Cons:

- Higher monthly payments: With no initial down payment, your monthly mortgage commitment could be steeper than you’d like.

- Higher interest rates: Loans with zero down payments often come with higher interest rates, meaning more money is paid out over the loan’s life.

- Income and household limits: Programs, particularly those affiliated with HUD, often come with income limits, which might restrict your eligibility based on your household income.

- Home buyer education: Some first-time home buyer loans with zero down require you to complete a home buyer education course, adding an extra step to your journey to homeownership.

- Limited initial equity: Jumping into a loan with no down payment means you start with zero equity in your home, making you more vulnerable to market fluctuations.

In a nutshell, while first-time home buyer loans with zero down can offer a fast track to becoming a homeowner, they come with their own set of challenges. Understanding these pros and cons can help you make a decision that aligns well with your financial circumstances and long-term goals.

Best no-down-payment mortgage lenders

Finding the best lenders for first-time home buyer loans with zero down payment comes down to two important tasks:

- Exploring state and local first-time home buyer programs

- Gathering quotes from lenders who specialize in government-backed loans, like VA loans and USDA loans

When you’re a first-time home buyer eager to secure a zero-down loan, choosing the right lender becomes paramount. The lender you select will determine not only the mortgage rates you’ll pay but also the overall experience you’ll have during the home-buying process.

What to look for in a lender

While large national lenders often advertise competitive rates, smaller local credit unions and community banks should not be dismissed. These institutions frequently offer personalized service and might have more flexible criteria when it comes to credit score requirements and income limits.

- Transparency: A good lender will clearly outline the terms, rates, and fees associated with your loan. This helps you understand the full scope of your financial commitment.

- Credibility: Check for lender certifications and read reviews. A lender’s reputation is a good indicator of the quality of service you can expect.

- Flexibility: Lenders vary in their flexibility regarding credit score requirements, income limits, and loan customization. Find one that aligns with your specific situation.

- Customer service: Excellent customer service can go a long way, especially for a first-time home buyer who may have numerous questions and concerns.

How to compare lenders

When it comes to the nitty-gritty of comparing loan quotes, consider more than just the interest rate. Consider the loan’s term length, which will have a significant impact on both your monthly payments and the total repayment amount.

- Mortgage interest rates: The lower the mortgage rate, the less you’ll pay over the loan term. However, remember that zero-down loans may inherently have higher rates due to the lender’s perceived risk.

- Loan terms: 15-year, 20-year, or 30-year? The term of the loan impacts both your monthly payment and the overall cost of the loan.

- Fees and charges: Look beyond the interest rate to other costs such as origination fees, application fees, and any penalties.

- Monthly payments: Make sure you understand what your monthly commitments will be, as this will significantly affect your budget.

Types of lenders known for zero-down home loans for first-time buyers

Lastly, consider specialized lenders who cater to specific needs.

For example, if you’re an American veteran, some lenders specialize in VA loans and can walk you through the specific advantages and stipulations of these no-down-payment loans.

Similarly, lenders well-versed in USDA loans can be invaluable if you’re considering buying a rural property.

- VA loan experts: Lenders like Veterans United and Navy Federal are known for specializing in VA loans, offering favorable terms to active-duty service members, veterans, and select family members.

- USDA loan providers: If you’re looking at rural properties, consider lenders like PNC Bank and Fairway Independent Mortgage, who are experienced in USDA loans.

- Online lenders: Platforms like Rocket Mortgage and Lending Tree offer the convenience of online applications and often have lower overhead, which could translate into better terms for you.

- Credit unions and community banks: These institutions often have a vested interest in building local communities and may offer favorable terms to first-time home buyers.

By doing thorough research and comparing multiple loan quotes, you’ll be well-equipped to select a lender with the best first-time home buyer loans with zero down for your particular needs.

How to get a down payment for a house

Buying a home is a significant milestone. But for borrowers who do not qualify for a first-time home buyer loan with zero down, coming up with a down payment can be a major hurdle.

If you’re having trouble saving up for a house, one of these strategies could help you make the minimum down payment needed for a home loan.

Check your home loan options. Start here.Apply for down payment assistance

In addition to first-time home buyer loans with zero down, many prospective homeowners are also eligible for cash assistance offered by state and local governments. If you can not pay the down payment on your own, these down payment assistance (DPA) programs can help you buy a house.

Some home buyer assistance programs offer up to 5% or more of the home’s sale price as a grant or loan. Many loans are silent second mortgage loans. As long as you retain ownership without selling or refinancing the property over a set period of time, these loans are exempt from repayment.

If you’re using a low-down-payment FHA or conventional mortgage, DPA could potentially cover your entire down payment, leaving you with $0 out of pocket. Keep in mind that you may still have to pay upfront closing costs (more info on this below).

DPA programs nationwide

There are more than 2,000 DPA programs nationwide, with assistance available in every state. Each program has its own guidelines, typically requiring you to be a first-time home buyer with a low-to-moderate income.

The amount of money you could get varies by program, too. For instance, one down payment assistance loan in New York City can offer up to $100,000 for eligible buyers, while another in Arkansas may cap assistance at $15,000.

If you’re hoping to qualify for a home-buying grant, the best first step is to contact either your local housing finance authority or a mortgage lender. Either one can tell you about local DPA options and help you find out whether you qualify.

Don’t forget closing cost assistance

As we mentioned above, your down payment isn’t the only upfront cost when buying a home. Buyers are also responsible for closing costs.

These include loan origination fees charged by the lender along with third-party fees required to set up your home loan (items such as credit report, home appraisal, title search, and underwriting fees).

Check your zero-down eligibility. Start hereUsually, closing costs range from 3% to 5% of the loan amount. That’s $15,000 to $25,000 for a $500,000 loan.

Even if you qualify for a no-down-payment mortgage, you still need to get your closing costs covered if you want to buy a house with no money.

Fortunately, there are a variety of ways to get help with your closing costs:

Closing cost assistance

Most down payment assistance programs can be used for closing cost assistance, too. However, the grant or loan you receive likely won’t be enough to fully cover both the down payment and loan fees. Consequently, you may have to pay the remainder out of pocket.

Seller-paid closing costs

It’s possible for a motivated seller to pay your closing costs. The way this often works is that you pay a little more for the home, and the seller kicks back that “extra” cash to cover your fees. You’re essentially rolling the cost into your mortgage loan when you go this route.

You can learn more about how seller concessions work here.

Lender-paid closing costs

Some mortgage lenders offer incentives to home buyers; they might be willing to cover part or all of your closing costs. This can be helpful if you’re short on cash, but be aware that no-closing-cost mortgages usually come with higher interest rates. So you could pay significantly more over the life of the loan.

You can learn more about how lender-paid closing costs work here.

Get a cash gift from a family member

Many homebuyers receive help in the form of a cash gift from family. It’s important to understand the tax rules regarding such gifts. Additionally, lenders typically require a letter from the family member confirming that the money is a gift and not a loan.

This gift letter should clearly state the relationship between the donor and the recipient, confirm that no repayment is expected, and specify the amount of the gift. The letter helps the lender document the source of your down payment funds, ensuring it’s not an additional loan.

Borrow from your 401(k)

Some 401(k) plans allow you to borrow against your retirement savings for a down payment. This can be a viable option, but it’s crucial to understand the terms of repayment and any potential impact on your retirement funds.

Typically, you can borrow up to 50% of your vested account balance, up to a maximum of $50,000. The loan usually needs to be repaid within five years, and payments are often required at least quarterly. Be aware that if you leave your job, the full loan amount may become due immediately. Additionally, while the interest you pay goes back into your account, it’s in after-tax dollars, and you’ll miss out on potential investment growth during the repayment period.

Read our guide on the pros and cons of borrowing from a 401(k) to buy a house.

Buy with a partner or co-borrower

Purchasing a home with a partner or friend can effectively halve the burden of the down payment. This approach requires careful planning and clear agreements about ownership, payments, and what happens if one party wants to sell their share.

Discuss and agree upon how mortgage payments, property maintenance, and other expenses will be shared. It’s advisable to involve a lawyer to draft a co-ownership agreement that protects both parties in case of disputes or changes in circumstances.

Learn more about buying a house with a co-borrower.

Use your savings

The most straightforward way to fund a down payment is through your savings. Start by setting a budget and a timeline to reach your savings goal. Cutting back on non-essential expenses and setting up automatic transfers to a savings account can help you build up the necessary funds.

Cash out investments

If you have investments in stocks, bonds, or mutual funds, consider liquidating some of these assets. This can be a quick way to access a substantial amount of money. However, be mindful of any tax implications or penalties that might apply.

Assess the market conditions and timing of cashing out investments, as this can significantly affect the return you receive. Consulting with a financial advisor can provide insights into the best strategy for liquidating assets without adversely impacting your long-term financial goals.

FAQ: First-time home buyer loans with zero down

Check your zero-down eligibility. Start hereThere are two ways to buy a house with no money down. One option is through a zero-down USDA or VA mortgage. The alternative entails a low-down-payment mortgage with additional down payment assistance to cover your upfront costs. FHA and conventional loans are available with just 3% or 3.5% down, and that entire amount is allowed to come from down payment assistance or a cash gift.

You can buy a house with no money down and no closing costs by using a zero-down loan and convincing a highly motivated seller to pay your closing costs. In some cases, you may be able to opt for the lender to cover the closing costs, but be aware that this usually means higher interest rates. Another option is to qualify for down payment assistance, which can help with some closing costs, but you’ll likely still need to pay a portion out of pocket, as these funds rarely cover both the down payment and all loan fees completely.

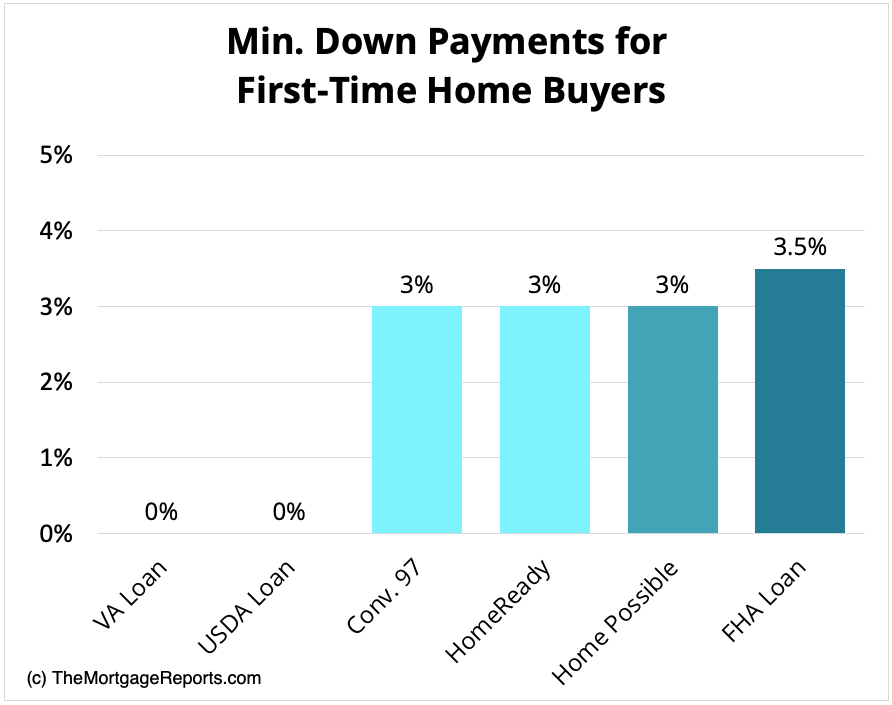

Down payment requirements vary by mortgage program. VA and USDA loans both allow zero down payments. Conventional loans start at just 3% down, while FHA loans require at least 3.5% down. You are free to contribute more than the minimum down payment amount if you want.

On average, closing costs are about 3% to 5% of the mortgage loan amount. That means closing costs on a $500,000 mortgage loan could range from $15,000 to $25,000. The amount you’ll pay in closing fees depends on your home purchase price, down payment amount, mortgage lender, and location.

Every home buyer is responsible for covering closing costs. However, there are various ways to reduce your out-of-pocket expenses. Buyers can ask the seller to cover their closing costs or have the lender pay them in exchange for a higher mortgage rate. You can also use funds from a down payment assistance program toward your upfront loan fees.

There are just two first-time home buyer loans with zero down. These are the USDA loan and the VA loan, which are both government-backed loans. Eligible borrowers can buy a house with no money down but will still have to pay for closing costs.

The FHA loan always requires a down payment of at least 3.5%. However, the money doesn’t have to come from your own savings. FHA accepts multiple down payment sources, including gift money and grants or loans from first-time home buyer programs. If you’re short on cash, talk to an FHA lender about your down payment funding options.

You’ll usually need a credit score of at least 640 for the zero-down USDA loan program. VA loans with no money down usually require a minimum credit score of 580 to 620. Low-down-payment mortgages, including conforming loans and FHA loans, also require FICO scores of 580 to 620.

If you lack sufficient savings for a down payment, lenders will allow you to use funds from other sources. Home buyer assistance programs offered by state and local governments can help eligible first-time buyers. You can also fund your down payment using gift money from relatives, a loan from your 401(k), cashed-out investments, or equity from another property you own. Talk to your mortgage lender about options if you’re short on cash.

Down payment assistance programs are available to home buyers nationwide, and many first-time home buyers are eligible. DPA can come in the form of a home buyer grant or a loan that covers your down payment and/or closing costs. Offerings vary by state, so be sure to ask your mortgage lender which programs you may be eligible for.

You may already qualify for a first-time home buyer loan with no down payment

Today’s home buyers have access to a wide range of mortgage programs. With all the low- and no-down-payment loans available, many first-time buyers can get into a house with little or even zero money down.

If you’re ready to buy a house but don’t have a lot of cash saved up, ask your mortgage lender about options. Odds are, there’s a home loan that could work for your financial situation.

Time to make a move? Let us find the right mortgage for you