Key Takeaways

- First-time home buyers often qualify for down payments as low as 3% to 3.5%, depending on the loan program.

- Buyers who put down 20% avoid private mortgage insurance and generally enjoy lower interest rates.

- Down payment assistance programs help buyers with grants, forgivable loans, or deferred second mortgages.

Concerned about your first-time home buyer down payment? Rest assured, the minimum down payment for a house is usually less than the traditional 20%. In fact, most buyers only need about 3-3.5% for conventional or FHA loans, which amounts to $13,500-$15,750 on a $450,000 home. Down payment assistance may help lower this amount further. So, if saving for the down payment is challenging, ask your mortgage lender what assistance options are available.

In this article (Skip to…)

- Average down payment

- Required down payment

- Deciding on your down payment

- Down payment assistance

- First time buyer loans

- FAQ

Understanding first-time home buyer down payment requirements

Homeownership can be a complex process for first-time home buyers, especially when it comes to understanding down payments. Let’s break down the key concepts to help you make informed decisions about your home loan.

Check your home buying eligibility. Start hereWhat is a down payment?

A down payment is the initial amount of money you pay upfront when purchasing a new home. It is usually calculated as a percentage of the home’s total purchase price, with the remaining cost financed through a mortgage loan.

Example: When purchasing a $450,000 home, a 10% down payment would amount to $45,000 paid upfront. The remaining $405,000 would be financed through a home loan.

A down payment not only affects the amount you need to borrow but can also influence your interest rate, monthly payments, and whether you’ll need to pay mortgage insurance.

Sometimes, a bank will lend you the entire amount you need to buy a home. This is known as 100% financing. But most mortgage loans require some contribution from you, the borrower.

What’s the average down payment on a house for first-time home buyers?

Many first-time home buyers believe they need 20% down. But that’s far from true. In fact, according to data from the National Association of Realtors, the average down payment for first-time home buyers is just 8% (versus 19% for repeat buyers). On a $450,000 home, that comes out to a $27,000 down payment.

Check your mortgage eligibility. Start hereYou’re allowed to put down even less. If you have a credit score of 620, you might qualify for a mortgage with just 3% down — or $13,500 out of pocket for a $450,000 home.

Thanks to the low-down-payment mortgages available today, many first-time home buyers find the process a lot more affordable than they initially thought. Yet, keep in mind that if you don’t put 20% down, you’ll have the additional cost of private mortgage insurance (PMI). We discuss this in more detail below.

How much do first-time home buyers have to put down?

The minimum down payment for a house as a first-time buyer will depend on the type of mortgage loan, but most buyers will need at least 3% to 3.5% down. Some home buyers can put zero percent down using a VA loan or USDA loan. But only certain borrowers will qualify for these mortgage programs.

Imagine you want to buy a new home for $450,000. Here’s how much you might have to put down as a first-time home buyer, depending on your qualifications:

Check your home buying eligibility. Start here| Credit Score | Debt-to-Income Ratio | Loan Type | Down Payment | Down Payment $ Amount |

| 500-580 | 40-50% | FHA loan | 3.5% | $15,750 |

| 620+ | Up to 45% | Conventional loan | 3% | $13,500 |

| 620+ | Up to 41% | VA loan | 0% | $0 |

| 640+ | Up to 41% | USDA loan | 0% | $0 |

To qualify for one of those zero-down first-time home buyer loans, you have to meet special requirements.

- For a VA loan, you need to be an eligible U.S. Armed Forces veteran or active-duty service member

- For a USDA loan, you must meet local income limits and also purchase a house in a qualified “rural area” — which usually means a population of 20,000 or less

But the other two loan types, conventional and FHA, are a lot easier to come by. You’ll still need to meet minimum credit score requirements as well as employment and income guidelines, just like any other home loan. But there are no “special” requirements to get a low-down-payment FHA or conventional loan as a first-time home buyer.

How much should you put down on a house as a first-time buyer?

Determining how much you should put down on a house as a first-time buyer involves involves weighing various factors, including your financial situation, loan options, and long-term goals.

While the traditional 20% down payment is often cited, it’s not the only option, nor is it always the best choice for everyone.

Check your home buying options. Start hereThe amount you should put down depends on:

- Your savings and income

- The home’s purchase price

- Your credit score

- Available loan programs

- Local real estate market conditions

- Your debt-to-income ratio

Take a look at one example:

| First-Time Home Buyer Loan | Minimum Down Payment | Down Payment for a $400,000 house | Monthly Payment (Principal & Interest / Mortgage Insurance)* |

| Conventional loan WITH mortgage insurance | 3% | $7,500 | $2,649 ($2,326 / $323) |

| FHA loan | 3.5% | $8,750 | $2,636 ($2,314 / $322) |

| VA loan | 0% | $0 | $2,398 ($2,398 / $0) |

| USDA loan | 0% | $0 | $2,515 ($2,398 / $117) |

| Conventional loan WITHOUT mortgage insurance | 20% | $80,000 | $1,919 ($1,074 / $0) |

*The example above assumes a 30-year fixed-rate mortgage with a 6% interest rate.

As shown in the table, a bigger down payment means a smaller loan, lower monthly payments, and no PMI with 20% down—potentially saving $100+ per month. However, a smaller down payment has its own less obvious benefits too.

Pros of a smaller down payment

If you want to get into a house sooner, making a smaller down payment with your current savings can be a smart choice. Here’s why it can be a good idea:

- Keeps your emergency fund intact

- Leaves cash for home improvements

- Lets you start building equity sooner

- Opens access to down payment assistance programs

- Avoids potential price increases

Pros of a larger down payment

While a larger down payment requires more money upfront, it can offer significant benefits:

- Lower loan amount and monthly payments

- Potentially lower interest ratesLess interest paid overall

- No private mortgage insurance with 20% down

- More appealing to sellers in competitive markets

Remember, your mortgage isn’t fixed forever. Even if you put down less as a first-time buyer, you can often refinance later to remove mortgage insurance and lower your monthly payments.

How to lower your down payment as a first-time buyer

The minimum down payment for a house as a first-time buyer can feel like a major hurdle. However, there are several methods to help lower your first-time homebuyer down payment, making homeownership more accessible.

First-time homebuyer down payment assistance programs

If you’re a first-time home buyer, you might not have to cover the first time home buyer down payment yourself. First-time buyers can apply for grants or low-interest second mortgages — called down payment assistance programs (DPAs) — to help with their upfront contribution.

Check your home buying eligibility. Start hereSome down payment assistance loans may also help cover closing costs, further reducing your out-of-pocket expenses.

Types of down payment assistance include:

- Grants: Funds that don’t require repayment

- Forgivable loans: Second mortgage loans that may be forgiven over time

- Low-interest loans: Affordable second mortgage options to complement your first mortgage loan

- Deferred-payment loans: Loans with payments postponed until you sell or refinance

Each down payment assistance program has slightly different guidelines. But it’s common for these programs to prefer first-time home buyers, borrowers with low- to moderate-income, and buyers in targeted “development areas.”

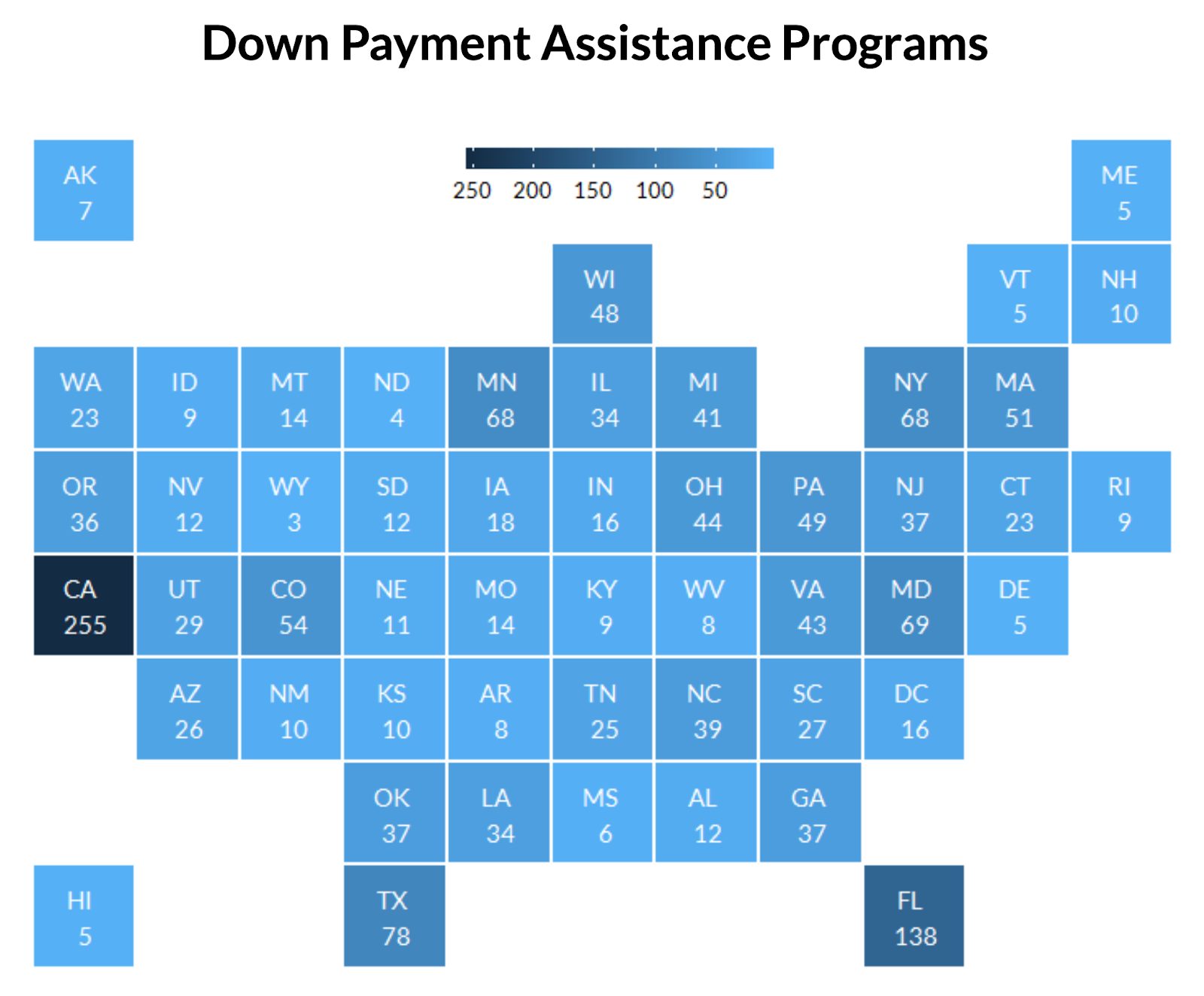

Number of down payment assistance programs by state

There are more than 1,600 of these DPAs nationwide. Many of these programs are run by nonprofits or local governments. Qualified buyers can receive anywhere from $5,000 to close to $35,000 toward their first time home buyer down payment and/or closing cost assistance.

Source: Down Payment Resource and The Urban Institute

First-time home buyer low or no-down-payment mortgages

As a first-time home buyer, you can choose how much money you want to put down towards the home’s purchase price. The down payment can be as large as you wish, or as small — so long as you make the minimum investment required by your mortgage lender and loan program.

Check your home buying eligibility. Start here1. FHA loans (3.5% down)

2. VA loans (0% down)

3. USDA loans (0% down)

4. Conventional 97 loans (3% down)

5. HomeReady (3% down)

6. Home Possible (3% down)

First-time home buyer down payment calculator

Our first-time homebuyer down payment calculator shows how different down payment amounts affect your loan size, monthly payment, and total borrowing costs. You can use it to explore scenarios before applying for a mortgage, so you understand the tradeoffs between putting less money down and paying mortgage insurance versus putting more down to lower long-term expenses.

Use our down payment calculator to:

- Estimate monthly mortgage payments based on various down payment amounts

- See how mortgage insurance impacts your costs

- Compare different loan programs and their down payment requirements

Other home buying costs to consider

First-time home buyers pay more than just a down payment when purchasing a home. Closing costs cover the fees required to finalize your loan and typically add 2%–5% of the loan amount, so most buyers should plan for an extra 3%–4% in cash on top of their down payment.

Typical closing costs include:

- Lender fees, including underwriting and processing.

- Home appraisal and credit report fees.

- Title search, title insurance, and settlement services.

- Recording fees and prepaid items such as interest or escrow deposits.

First-time home buyer down payment FAQ

Check your home buying eligibility. Start hereFind a low first time home buyer down payment

First-time home buyers have lots of options when it comes to making a down payment.

Research your home loan options thoroughly to minimize your out-of-pocket costs, as many require just 0% to 3% down. Then make sure you find a participating mortgage lender who offers the home loan program you need.

Don’t forget to look into down payment assistance options near you. Help is available for first-time home buyers who know where to look for it.

Time to make a move? Let us find the right mortgage for you