Mortgage StrategyFebruary 16, 2023How much is mortgage insurance? PMI cost vs. benefitPrivate mortgage insurance (PMI) is usually required if you put less than 20% down. Learn how much mortgage insurance costs and when you need it.

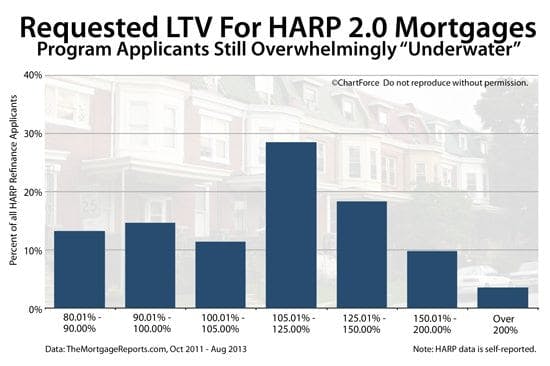

HARP RefinanceAugust 13, 2013HARP 2.0 : Finding Lenders To Refinance Your Underwater Mortgage With Existing PMI Or LPMIThe HARP 2.0 refinance program makes refinancing loans with private mortgage insurance (PMI) easy. How to get your refinance complete.

Tax Law For MortgagesApril 2, 2013Mortgage Insurance Tax-Deductible For 2012 And 2013New laws have made mortgage insurance is tax-deductible for 2013. The change is retro-active for 2012 tax returns, too.

UncategorizedAugust 24, 2012Mortgages On Maternity Leave : MGIC Settlement Streamlines Loan ApprovalsMGIC settles housing discrimination claim with the Department of Justice and agrees to revise approval guidelines related to family leave.

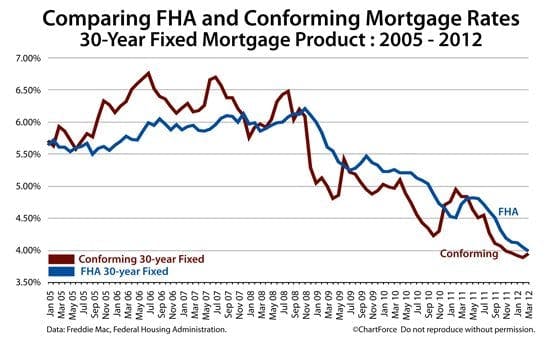

Mortgage StrategyAugust 17, 2012FHA Mortgage Rates Lower Than “Freddie Mac” Mortgage RatesThere is a big advantage to "going FHA" these days -- especially if you're making a low downpayment purchase. FHA mortgage rates are low as compared to conventional ones.

Mortgage StrategyMay 8, 2012FHA Mortgage Rates Vs Conforming Mortgage Rates : Which Is Better For You?Is an FHA mortgage better for you than a conventional one? A quick rundown of each product and a comparison chart.

FHA Home BuyingSeptember 17, 2010FHA Mortgage Insurance Premiums To Rise In October : Should You Act Now, Or Should You Wait?For the second time in 4 months, the FHA is changing the way it charges mortgage insurance.