Conforming MortgagesSeptember 12, 2012Improve Your Mortgage Approval : The Income-Equity-Credit TriangleMortgage underwriting may be strict, but there's no magic formula for getting approved. Satisfy the Mortgage Income-Equity-Credit Triangle.

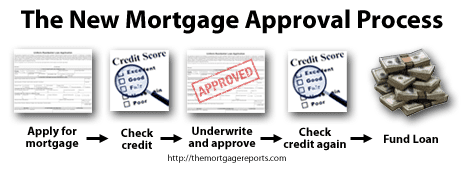

FICO & Credit ScoresAugust 25, 2012Your Credit Report Will Be Re-Pulled Just Prior To Closing (And It Could Change Your Loan Terms)When does "cleared to close" not mean "cleared to close"? When Fannie Mae's involved! Keep your loan approval intact all the way through funding. Here's how.

Conforming MortgagesDecember 10, 2010Winter 2011 : “Cheat Sheet” For The New Fannie Mae GuidelinesIn Winter 2011, Fannie Mae changed its mortgage guidelines to favor personal income over personal assets. Check the "Cheat Sheet" to see how you'll be affected.

Conforming MortgagesSeptember 29, 2009Fannie Mae To Get Tougher On Mortgage Insurance, Income Levels and Credit ScoresFor the second time in 10 weeks, Fannie Mae is toughening its mortgage guidelines again. Again. According to an internal Fannie Mae document, a review of the group's current "risk appetite, eligibility requirements, mortgage insurance options, and pricing" spawned changes spanning credit scoring, income requirements, loan-level pricing adjustments.

Conforming MortgagesJuly 20, 2009Fannie Mae Toughens Guidelines On 2-Unit Homes, Trailing Spouses And Retirement PortfoliosMortgage approvals are getting more difficult. Again. After reviewing recent unemployment data and market fluctuations, plus patterns of mortgage fraud, Fannie Mae is making major mortgage guideline changes for the first time in more than 6 months. The changes are broad, impacting 15 separate areas of the mortgage approval process. The most impactful change may be Fannie Mae's new restrictions on mortgages for 2-unit properties.