Mortgage RatesMay 18, 2021Mortgage rates and inflation: Why are rates going up?What's the relationship between mortgage rates and inflation? Learn why high inflation might cause mortgage rates to go up this year.

Economic NewsJuly 17, 2012A Helpful Chart : How Inflation Changes Mortgage RatesInflation is a self-reinforcing cycle. The longer it lasts, the more insidious its effects, and rising mortgage rates are an unfortunate consequence.

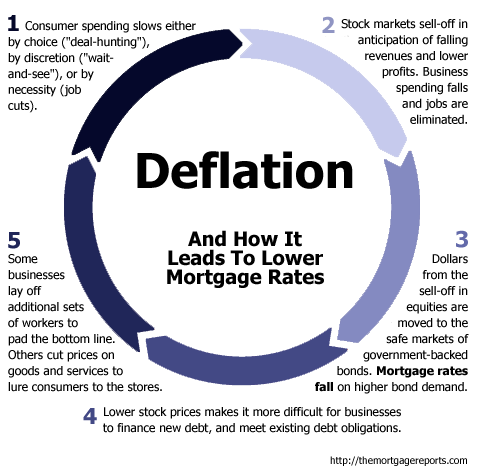

Economic NewsSeptember 27, 2010How Deflation Changes Mortgage RatesAccording to Google, "deflation" chatter is growing. It's extending the Refi Boom for another few weeks.