Federal ReserveMarch 15, 2021

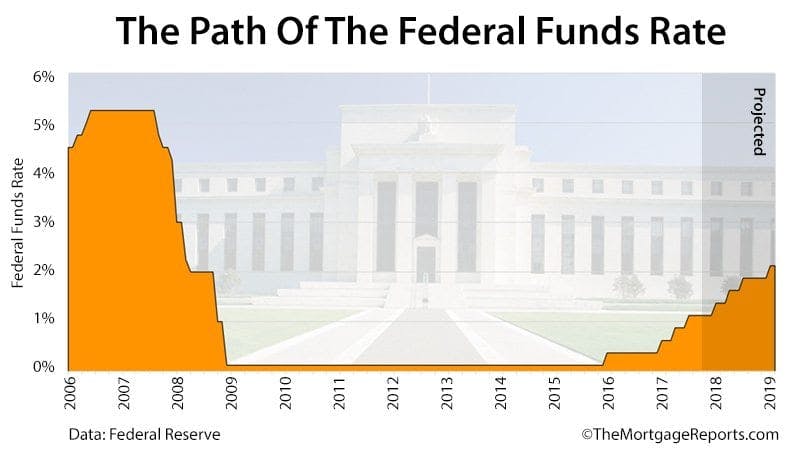

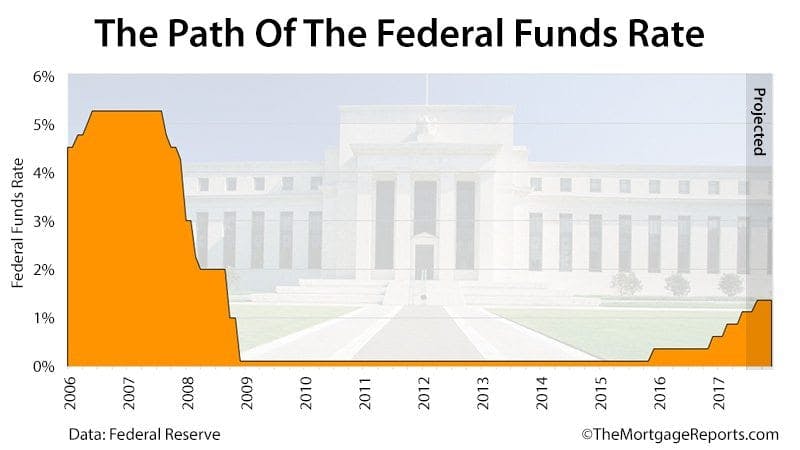

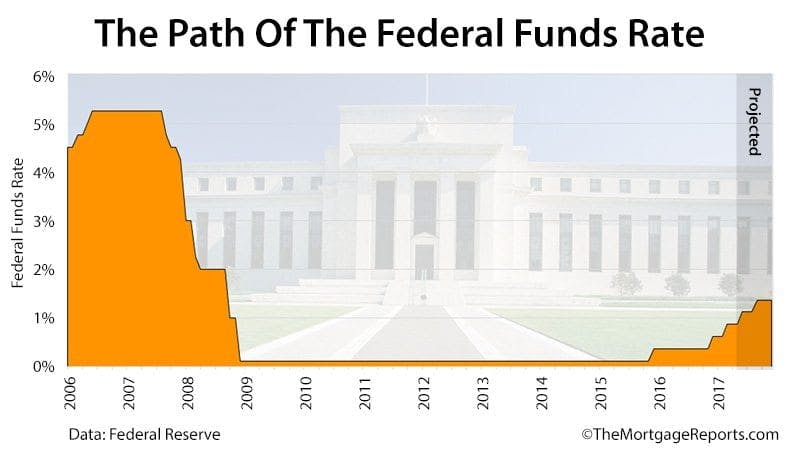

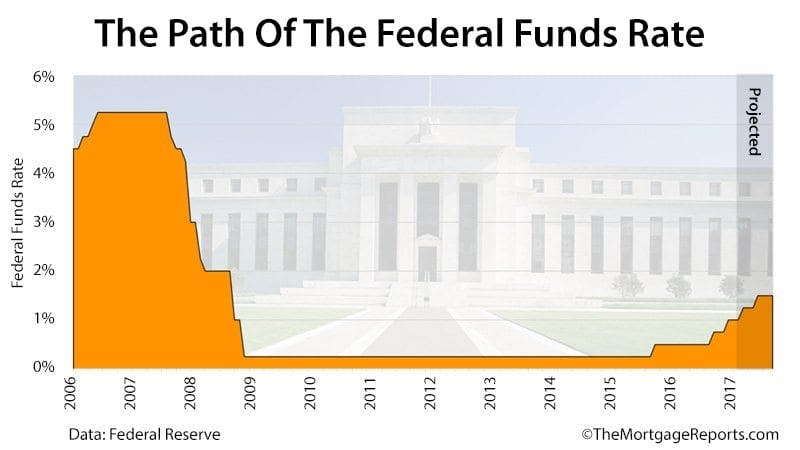

How mortgage rates move when the Federal Reserve meets

The Fed adjourns from a 2-day meeting Wednesday. The group doesn't set mortgage rates but it can influence them. How this week's meeting could affect your refinance and purchase mortgage rate.