About MortgagesMay 27, 2026Current Mortgage Rates by Credit Score | 2026Mortgage rates by credit score vary widely. So what does your score get you? And what can you do to qualify for a lower rate?

FICO & Credit ScoresNovember 29, 2023What’s the Minimum Credit Score to Buy a House?What's the minimum credit score to buy a house? You should qualify with a score of 580-620. Learn how your credit impacts your mortgage.

FICO & Credit ScoresMay 6, 2022How to shop for a mortgage without hurting your credit scoreLearn how to shop for a mortgage and find the lowest interest rate without hurting your credit score. Start here.

FICO & Credit ScoresNovember 11, 2021Tips for getting a mortgage with a 680 credit scoreIf you're looking for rates that "good credit" can get you, click through to see loan options and mortgage rates for a 680 credit score.

FICO & Credit ScoresAugust 13, 2018What is a “good” credit score, and how do you make it even better?What is a good credit score, and how can you go from good to excellent? Find out here.

FICO & Credit ScoresMay 19, 2017Mortgage Credit Report: Lenders Accept Non-Traditional CreditIf your mortgage credit report has limited data, don't despair. Mortgage lenders are much more accepting of non-traditional credit today.

FICO & Credit ScoresJune 9, 2016How To Boost Your FICO Score Before Buying Your Next HomeTake steps to boost your FICO score before applying for your next mortgage. Better scores mean lower mortgage rates and better terms. Today's rates, too.

FICO & Credit ScoresApril 15, 2016Improving Your Credit Score Using “Authorized User” AccountsAuthorized User accounts can affect your credit score -- good or bad. Know how they work, and how to work them to your advantage. Improve your FICO today.

FICO & Credit ScoresApril 11, 2016You Don’t Need A 740 FICO Score To Get A MortgageYou can get mortgage-approved with credit scores as low as 500. However, with some simple steps, you can improve your FICO by a lot. Easy-to-follow tips.

FICO & Credit ScoresApril 18, 2015What Makes Your FICO Credit Score Change Each Month?Keeping a decent credit score can help you get access to better, lower mortgage rates. Free advice to help you boost your credit scores quickly.

FICO & Credit ScoresSeptember 10, 2014FICO Changes Expected To Boost Credit Scores, Lower Consumer Mortgage RatesA new FICO scoring method is expected to raise credit scores by 25 points, at minimum; and 100 points at maximum. Read more and get a live rate quote now.

FICO & Credit ScoresAugust 29, 2014Current Mortgage Rates Dropping For FICO Scores Of 580+Lenders are lowering credit score requirements. Read more on today's minimum required FICO scores, and get a live mortgage rate quote.

FICO & Credit ScoresAugust 24, 2014New FICO Scoring Model Raises Your Credit ScoresA new FICO credit scoring model will raise borrower credit scores. Analysis of the changes, plus today's live mortgage rates.

Mortgage StrategyMay 25, 2014As Mortgage Rates Drop, Mortgage Standards Expand To Include Lower Credit ScoresEffective immediately, mortgage lenders have lowered minimum FICO requirements on home loans. Read more about the shift, and get today's live mortgage rates.

FICO & Credit ScoresAugust 25, 2012Your Credit Report Will Be Re-Pulled Just Prior To Closing (And It Could Change Your Loan Terms)When does "cleared to close" not mean "cleared to close"? When Fannie Mae's involved! Keep your loan approval intact all the way through funding. Here's how.

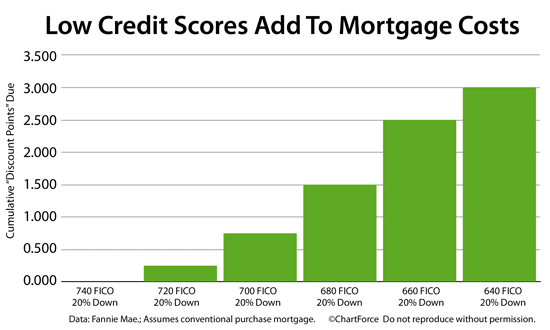

Mortgage StrategyNovember 1, 2011Credit Score Under 740? Prepare To Overpay On Your Mortgage.Most people know that low FICO scores influence the mortgage rates for which they're eligible. For the past 3 years, though, they've raised closing costs, too.

FICO & Credit ScoresOctober 10, 2011Chart : How Does A Foreclosure, Missed Payment, And Maxed-Out Credit Card Change Your FICO ScoreThe company behind the FICO scoring model published a "What If?" series for common, specific credit missteps. See how your scores can change with a foreclosure, missed payment, maxed credit card, and more.