Mortgage RatesApril 12, 2013Mortgage Rate Patterns : What You’ll See Through April And MayMortgage rates are following seasonal patterns. Here's what you might see from the 30-year fixed rate mortgage through April and May.

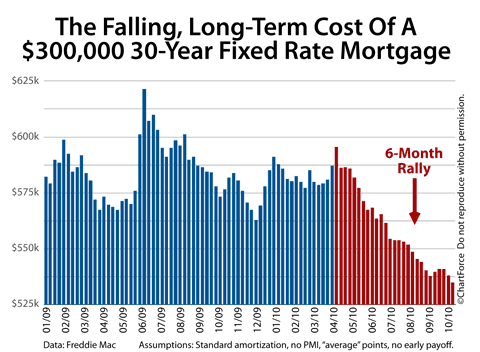

Mortgage StrategyOctober 12, 2010In Charts : The Falling, Long-Term Cost Of A 30-Year Fixed Rate MortgageAs compared to the day *after* the expiration of the $8,000 home buyer tax credit, today's cost of carrying a 30-year fixed rate mortgage to term is lower by $51,000. Mortgage rates are on a 6-month rally.