Mortgage StrategyFebruary 16, 2023How much is mortgage insurance? PMI cost vs. benefitPrivate mortgage insurance (PMI) is usually required if you put less than 20% down. Learn how much mortgage insurance costs and when you need it.

About MortgagesSeptember 22, 2022What is PMI? Home buyer’s guide to private mortgage insurancePrivate mortgage insurance (PMI) is an extra monthly cost that protects your lender. But it lets you buy a house without 20% down.

Mortgage StrategyOctober 5, 20174 types of PMI: which one is right for you?There is more than one type of PMI; in fact, there are four. Choosing the right one puts you in a better home buying position.

About MortgagesAugust 6, 2017Behind On Mortgage Payments? Try A Claim AdvanceIf you're behind on your mortgage payments, and you have private or government-backed mortgage insurance, you may be able to get back in control with a claim advance. A claim advance is money from your mortgage insurer used to bring your account current.

About MortgagesJune 13, 2017PMI Mortgage Insurance: You Can Pay LessPMI mortgage insurance is a necessary evil if you buy or refinance more than 80 percent of your property value. But there are are things you can do to reduce what you pay.

Mortgage StrategyJune 7, 2016Is PMI Bad? No. Here Are The “Silent” Benefits Of Mortgage InsurancePMI offers protections for the homeowner, not just the lender. Most buyers have never heard of these two benefits that are directed at the consumer.

About MortgagesMay 31, 2016Private Mortgage Insurance (PMI) Is Neither “Good” Nor “Bad”Not sure whether you want to put 20% down on a home? It's okay if you don't. Frank talk about private mortgage insurance (PMI) and how it can help you buy.

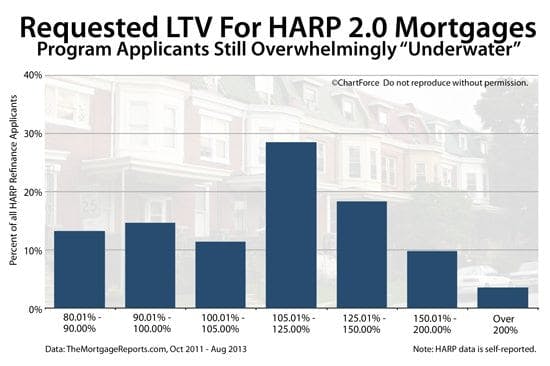

HARP RefinanceAugust 13, 2013HARP 2.0 : Finding Lenders To Refinance Your Underwater Mortgage With Existing PMI Or LPMIThe HARP 2.0 refinance program makes refinancing loans with private mortgage insurance (PMI) easy. How to get your refinance complete.

Tax Law For MortgagesApril 2, 2013Mortgage Insurance Tax-Deductible For 2012 And 2013New laws have made mortgage insurance is tax-deductible for 2013. The change is retro-active for 2012 tax returns, too.