Mortgage RatesSeptember 9, 2020How mortgage rates are determined and why you should careLearn how mortgage rates are determined, what causes lenders to offer you a higher or lower rate, and why mortgage rates rise and fall daily.

Federal ReserveJune 17, 2020For once, the Fed DOES affect mortgage rates. Here’s whySince March, the Fed has controlled mortgage rates more than usual. Find out how the Federal Reserve helped push mortgage rates to record lows.

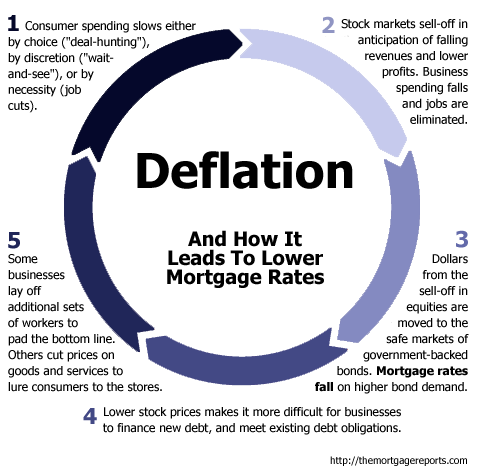

Economic NewsSeptember 27, 2010How Deflation Changes Mortgage RatesAccording to Google, "deflation" chatter is growing. It's extending the Refi Boom for another few weeks.