About MortgagesApril 26, 2023Loan-Level Pricing Adjustments (LLPA): A Complete Guide For Mortgage BorrowersThe loan-level pricing adjustment (LLPA) system raises mortgage rates for conventional mortgage borrowers. See how LLPAs work here.

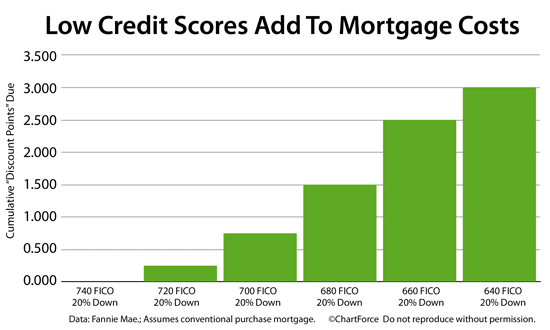

Mortgage StrategyNovember 1, 2011Credit Score Under 740? Prepare To Overpay On Your Mortgage.Most people know that low FICO scores influence the mortgage rates for which they're eligible. For the past 3 years, though, they've raised closing costs, too.

Mortgage RatesJuly 26, 2011FHA Mortgage Rates Vs. Conforming Mortgage Rates : Which Are Cheaper?The FHA insures 25% of the mortgage purchase market these days, up from 5 percent in 2006. Is it because FHA mortgages are cheaper than conforming ones?

Conforming MortgagesSeptember 29, 2009Fannie Mae To Get Tougher On Mortgage Insurance, Income Levels and Credit ScoresFor the second time in 10 weeks, Fannie Mae is toughening its mortgage guidelines again. Again. According to an internal Fannie Mae document, a review of the group's current "risk appetite, eligibility requirements, mortgage insurance options, and pricing" spawned changes spanning credit scoring, income requirements, loan-level pricing adjustments.

FHA Home BuyingMarch 25, 2009FHA Ends Its 95 Percent Cash-Out Refinances March 31, 2009. 85 Percent Is New Maximum.The FHA is discontinuing its 95% cash-out refinance program effective April 1, 2009. For all case assigmements made on or after April 1, 2009, cash-out refinances are limited to 85%. "Case assignment" is FHA-speak for "registered loans".